Slowing Growth and Rising Federal Debt Complicate US Economic Outlook

By James Picerno | The Milwaukee Company

The US long-term economic growth trend is still showing signs of a slow, persistent downshift

The increasing federal budget deficit could become a significant headwind for growth in the years ahead

These two factors are complicating the government's policy agenda and will be harder to resolve the longer they are ignored

A year ago TMC Research advised that slowing economic growth and the government’s failure to stabilize if not reverse the deepening federal budget deficit would “complicate and constrain” Washington’s policy agenda. Twelve months on, the risk continues to resonate.

This week the Treasury Department reported that the US government’s gross national debt topped $37 trillion, a new record high. As a result, the government’s budget deficit rose 19% in July vs. the year-ago level.

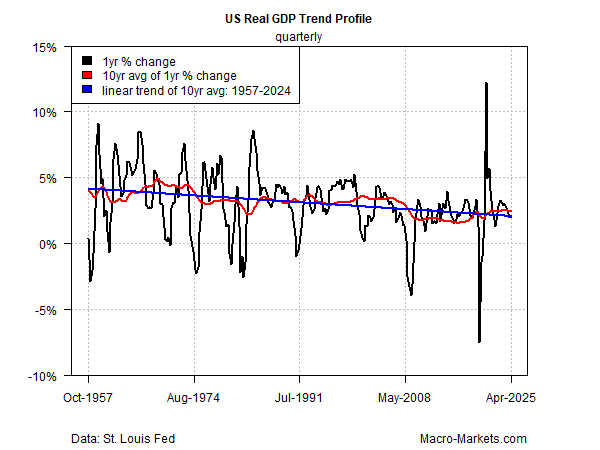

Meanwhile, a long-term downshift in US economic growth has been unfolding for decades. There are several reasons, but it’s fair to say that the government’s rising debt doesn’t help. Whatever the causes, the latest economic data still highlight a slow but persistent decline in the growth trend for US real (inflation-adjusted) gross domestic product (GDP), a broad measure of economic output.

The blue line in the chart above indicates the long-term bias, based on the linear trend for 10-year changes, a measure that’s been gradually but consistently slipping. In the shorter run, the economy ebbs and flows, as shown by the more-volatile 1-year change (black line) and its smoothed version (red line), defined as the 10-year average of 1-year changes. But the economic equivalent of gravity remains ongoing.

There are several factors behind the softer growth trajectory, some of which are beyond the government’s control. One is that as economies mature, growth inevitably downshifts in relative terms. Economic activity on a comparative basis can’t perpetually rise because of the law of diminishing marginal returns, technological limits and other constraints. Much as a company’s growth rate is destined to slow once it reaches a certain size, the US economy – the world’s largest – runs into limits for boosting growth rates compared with smaller economies.

The same constraint applies to every country in some degree, particularly in the developed world. To be fair, the US certainly retains a number of key advantages over its peers and competitors – a flexible workforce, a history of technological innovation, and robust capital markets, for instance.

Although economic activity is primarily driven by the private sector, government policy is a powerful force for tipping the scales in favor, or against, growth. The fiscal drag from a large and deepening budget deficit, however, is a headwind, and one that threatens to become a significant factor in the years ahead absent the political will to address the mounting fiscal challenge.

A short-term reprieve from red-ink risk may be plausible in some degree over the near term, as we discussed last week in our update on US fiscal risk. Tariffs collected by the US government so far this year have surged through early August, more than doubling the amount vs. the year-ago level, reports the Bipartisan Policy Center, a think tank.

But the potential for slower growth linked to higher tariffs may eventually offset any advantage. Meanwhile, projections that the US debt-to-GDP ratio will rise to new heights could more than cancel out any revenue boost from tariffs. The current ratio is roughly 121%, based on the total public debt as a percent of GDP in the first quarter. The expected trajectory is on track to rise to 156% by 2055, the Congressional Budget Office projects.

One facet of the threat from deepening fiscal risk relates to the upward influence on interest rates. A new estimate from the Dallas Federal Reserve notes:

Each percentage point increase in the debt-to-GDP ratio increases long-term interest rates by 3 basis points. (100 basis points equal 1 percentage point.) This suggests, holding all else equal, long-term interest rates could rise more than 1.5 percentage points over the next 30 years if debt increases as projected.

Higher interest rates are a headwind for growth. What’s the solution? The main challenge is addressing a basic problem: government revenues aren’t keeping pace with outlays. In the current political climate in Washington, the prospects for a concerted effort to rein in spending has been mixed, at best, to date.

Meanwhile, some of the solutions on the demand side for juicing economic growth have become politically unpopular. The CBO summarized this issue recently by noting: “Without immigration, the US population would begin to shrink in 2033,” which would be another factor weighing on growth.

Meanwhile, the downside bias for the economic trend looks set to strengthen if the budget deficit worsens. The calculus is based on an assumption that as federal borrowing rises, the trend is expected to: 1) slow capital accumulation, which in turn suppresses labor force productivity; and 2) create upside pressure on interest rates.

Similar growth headwinds also apply throughout much of the developed world, and so in a relative sense American exceptionalism will likely endure for the foreseeable future, if only in relative terms. That may suffice to keep US financial markets competitive in the near term.

Ultimately, the federal deficit will be resolved, one way or the other, although the details and timing are unclear. Along the way, an uncomfortable fact endures: The longer the government waits to resolve the fiscal challenge, the harder and more painful the solution will be.