Will Tariff Revenue Reduce US Fiscal Risk?

By James Picerno | The Milwaukee Company

US tariff revenue has increased sharply lately

In the short term, higher tariff revenue will help ease US fiscal risk, but…

The longer-term impact from tariffs is expected to bring mixed results for the economy

Debates about the effects of tariffs are wide ranging and, for the most part, speculative, at least so far. Although many economists expect that tariffs will lift inflation, if only temporarily, and slow growth, the evidence to date has been mixed in terms of the hard data, leaving room to argue in favor of a variety of scenarios for the months ahead. The main exception: government revenue collected from customs duties and some excise taxes have increased sharply, according to Treasury data.

Analysis by the Bipartisan Policy Center, a think tank, estimates that tariffs so far this year have jumped to $129 billion, as of August 5. That’s well more than double the amount at this point in 2024, and even further ahead vs. comparable periods in earlier years.

The possibility that higher tariff revenue will be the new normal for the US raises the potential for a positive upgrade in the US fiscal outlook, if only at the margins. The Tax Foundation, another think tank, projects that tariffs (if they remain intact) could generate up to $2 trillion in additional revenue for the government over the next ten years.

From a purely accounting-ledger perspective, tariffs will be a factor in slowing if not reversing the government’s growing fiscal deficit of late. Optimists also point to the Department of Government Efficiency (DOGE), which reports that its reforms and cutbacks have saved $199 billion so far this year. Although the estimate is widely disputed, by some accounts it’s another sign that efforts to address government profligacy are making headway.

But these are still early days, and so looking at tariffs in isolation is misleading, advises The Budget Lab at Yale:

All 2025 US tariffs plus foreign retaliation lower real GDP growth by -0.5pp each over calendar years 2025 and 2026 (Q4-Q4). The unemployment rate ends 2025 0.3 percentage point higher and 2026 0.7 percentage point higher, and payroll employment is 497,000 lower by the end of 2025. The level of real GDP remains persistently -0.4% smaller in the long run, the equivalent of $120 billion 2024$ annually, while exports are -16.0% lower.

On the other hand, some of the darker forecasts from analysts have, so far, been wide of the mark. Tariffs, argued some analysts several months ago, would quickly trigger a recession and raise inflation sharply – neither of which happened, at least so far. The pushback is that the tariff impact will take time, in part because businesses have been absorbing the higher prices from tariffs. The thinking now is that as various efforts to delay the tariff effect fade in the months ahead, the negative economic effects will become increasingly obvious.

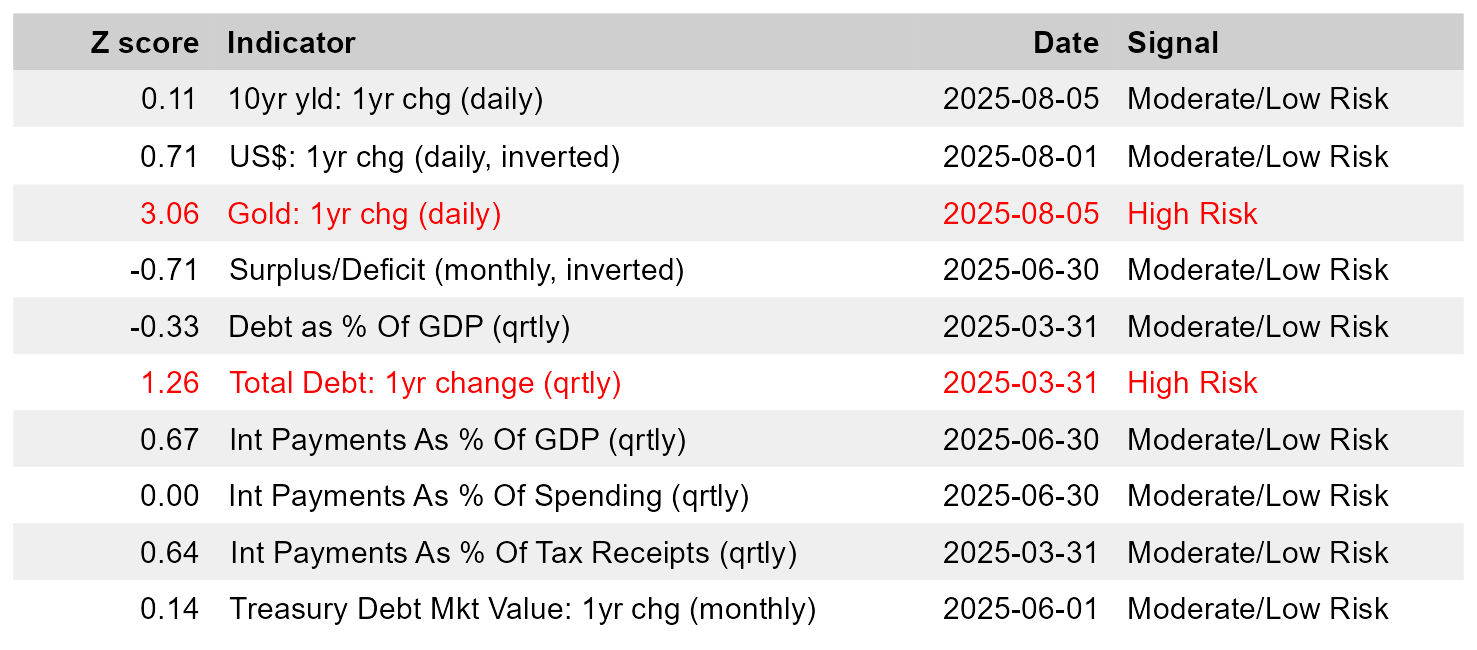

As for data published to date, the tariffs may have reduced fiscal risk a notch as the monthly deficit retreated in the second quarter to a relatively moderate/low risk state following Q1’s high risk profile for this data, based on TMC Research’s modeling.

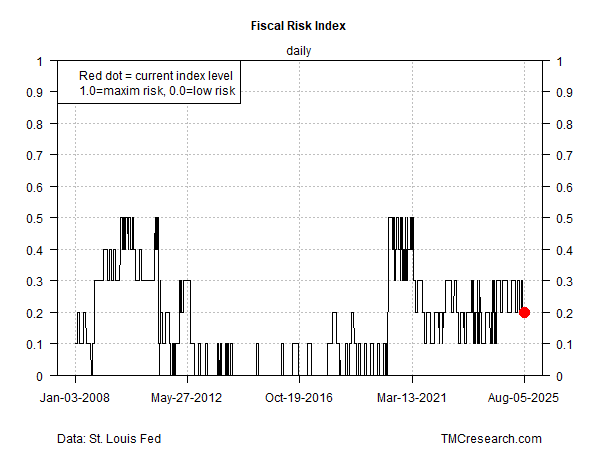

In turn, our 10-factor Fiscal Risk Index (based on the indicators in the table above) ticked down to a 0.2 reading from 0.3 previously. That’s a relatively low level that’s within the range of recent years.

The implication: the state of US fiscal risk remains more or less unchanged compared with the past several years of the post-pandemic period.

Keep in mind that this view is based on relative changes. The Fiscal Risk Index is an effort to monitor relative changes through time.

In absolute terms, by contrast, the state of US fiscal risk remains worrisome, at least by some indicators. For example, the Congressional Budget Office this month advised that the government’s new spending legislation enacted last month will increase the federal deficit by $4.1 trillion in the decade ahead.

The implication: the already hefty amount of federal debt as a percentage of GDP – 121% in Q1 – looks set to rise further. The current level (excluding the temporary spike during pandemic spending) is close to a record high in the modern era.

Even deeper shades of red may be likely unless: 1) economic growth ramps up, generating higher-than-expected tax and tariff revenue; or 2) Congress reduces spending. Short of one or both of those scenarios unfolding, borrowing costs could rise, which may reverberate through financial markets and the economy.

For now, it’s not obvious that a lot has changed for the fiscal-risk outlook. Will the status quo prevail in the second half of the year, as the effects from tariffs – good or ill – become more pronounced? A key clue may be waiting in our next update.