Resilient, Not Recessionary: The US Economy Refuses to Crack

By James Picerno | The Milwaukee Company

Recession odds stay low as growth outperforms crisis expectations

TMC’s recession indicator signals resilience, not contraction, despite inflation pressures

Stronger hiring and firming GDP keep the Fed in wait‑and‑see mode

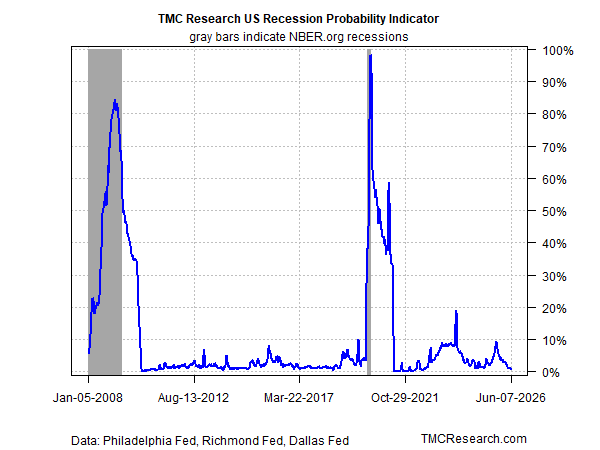

At the start of the Iran conflict, many analysts expected US economic growth would stumble and recession risk would spike. It was a reasonable view at the time, although TMC Research noted a few days after the war started that our “Recession Probability Indicator (RPI) continues to reflect a low probability that an NBER-defined downturn has started or is imminent.” An update of the numbers suggests more of the same.

More than three months into the Middle East crisis, the American economy still looks resilient. Inflation is an ongoing threat, thanks to the supply-side energy shock that’s lifted prices. But growth has held up better than expected, and the odds appear low that the economy is on the precipice of a material slowdown, much less an outright contraction.

The TMC Recession Probability Indicator (RPI) is currently estimating that it’s highly unlikely the economy is shrinking or will soon slip over the edge. That doesn’t mean macro risks are absent – quite the opposite. Rather, RPI reports that the quantitative signals that usually flag elevated recession risk are subdued at the moment. (RPI aggregates and processes data from three business‑cycle indicators published by regional Fed banks — see here for details.)

Last week’s release of payrolls data for May aligns with RPI’s growth bias. Hiring increased by 172,000 positions last month, beating expectations by a wide margin and marking the third straight month of relatively strong employment gains. Meanwhile, the jobless rate was unchanged at a low 4.3%.

While hiring has remained relatively resilient, the majority of recent job creation has been concentrated in the healthcare and hospitality sectors, and many other industries continue to struggle. At the same time, consumer sentiment remained near record lows in May, signaling a considerable degree of unease among households.

From a top-down perspective, however, the near-term outlook remains upbeat. For example, the Atlanta Fed’s GDP nowcast for the upcoming second‑quarter economic report is on track to accelerate to a 3.3% annualized pace, according to the bank’s model (June 9). If correct, the rate of output’s increase will more than double from Q1’s 1.6% advance.

None of this should dismiss the concern that the ongoing effects from the crisis pose a threat to the economy, primarily in the form of higher inflation. The key variable is how long the conflict lasts, which will likely determine when energy exports through the Strait of Hormuz rebound to something approximating normal — a shift that would, in turn, likely cool the recent inflation surge.

Forecasting such a turn of events is extremely challenging, although that won’t stop journalists from posing the question to Kevin Warsh, the new Federal Reserve chair, who will field these and related topics for the first time at the central bank’s press conference next week.

The economy’s resilience to date will give the Fed cover for leaving interest rates steady at next week’s June 16–17 policy meeting. But the resilience also suggests a strengthening case for raising rates. If economic activity is firming at a time when inflation is heating up, tightening monetary policy is a reasonable response at some point.

Fed funds futures currently estimate low odds for a rate hike next week and at the subsequent meeting in late July. But sentiment is starting to lean into a hawkish policy pivot later in the year – an outlook that will continue to resonate if recession‑risk odds stay low.