Iran War Risk Still Low for the US Economy — But the Safety Margin May Be Shrinking

By James Picerno | The Milwaukee Company

US recession risk was low at the start of military strikes on Iran

The market was calm on Monday, but the situation is fluid and the risk profile will remain sensitive to headlines

Oil is a key factor, with the possibility of sustained price spikes posing the main macro risk

The ongoing US-Israel military strike on Iran remains a highly fluid situation, with the potential for significant fallout for the global economy and financial markets. The conflict is still evolving and so it’s difficult at this stage to develop reasonable forecasts of the war’s effects, but US recession risk was still subdued ahead of the attack that began on Saturday.

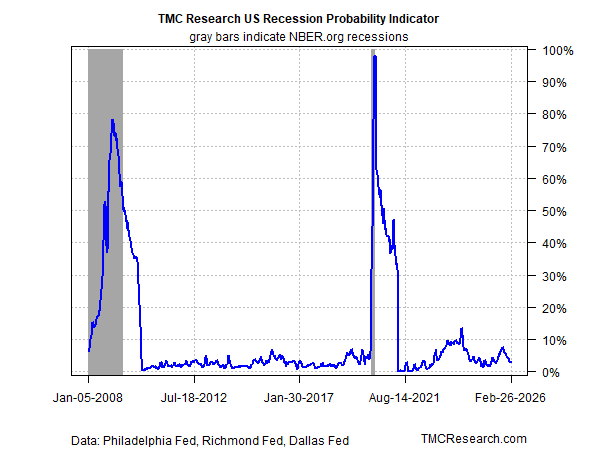

The TMC Recession Probability Indicator (RPI) continues to reflect a low probability that an NBER-defined downturn has started or is imminent. The current estimate indicates a roughly 3% probability of contraction, based on data through Feb. 26 – an estimate that’s fallen slightly since our previous update three months ago. (RPI aggregates and processes data from three business-cycle indicators published by regional Fed banks — see here for details.)

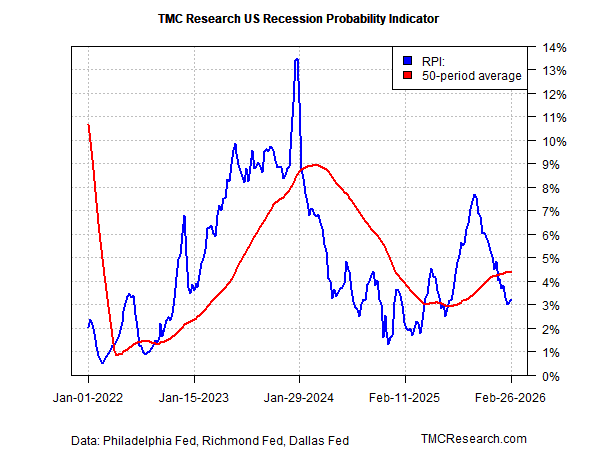

Focusing on recent history shows that the trend (50-period average) has edged higher recently, but it’s fair to say that the current level suggests a high probability that the economy’s current bias remains strongly skewed toward growth.

The caveat is that RPI, and similar metrics, are designed to capture “normal” business-cycle fluctuations rather than so-called exogenous events, such as the military strike on Iran. To the extent that war will create headwinds for economic activity the transmission would likely come via an oil-price shock.

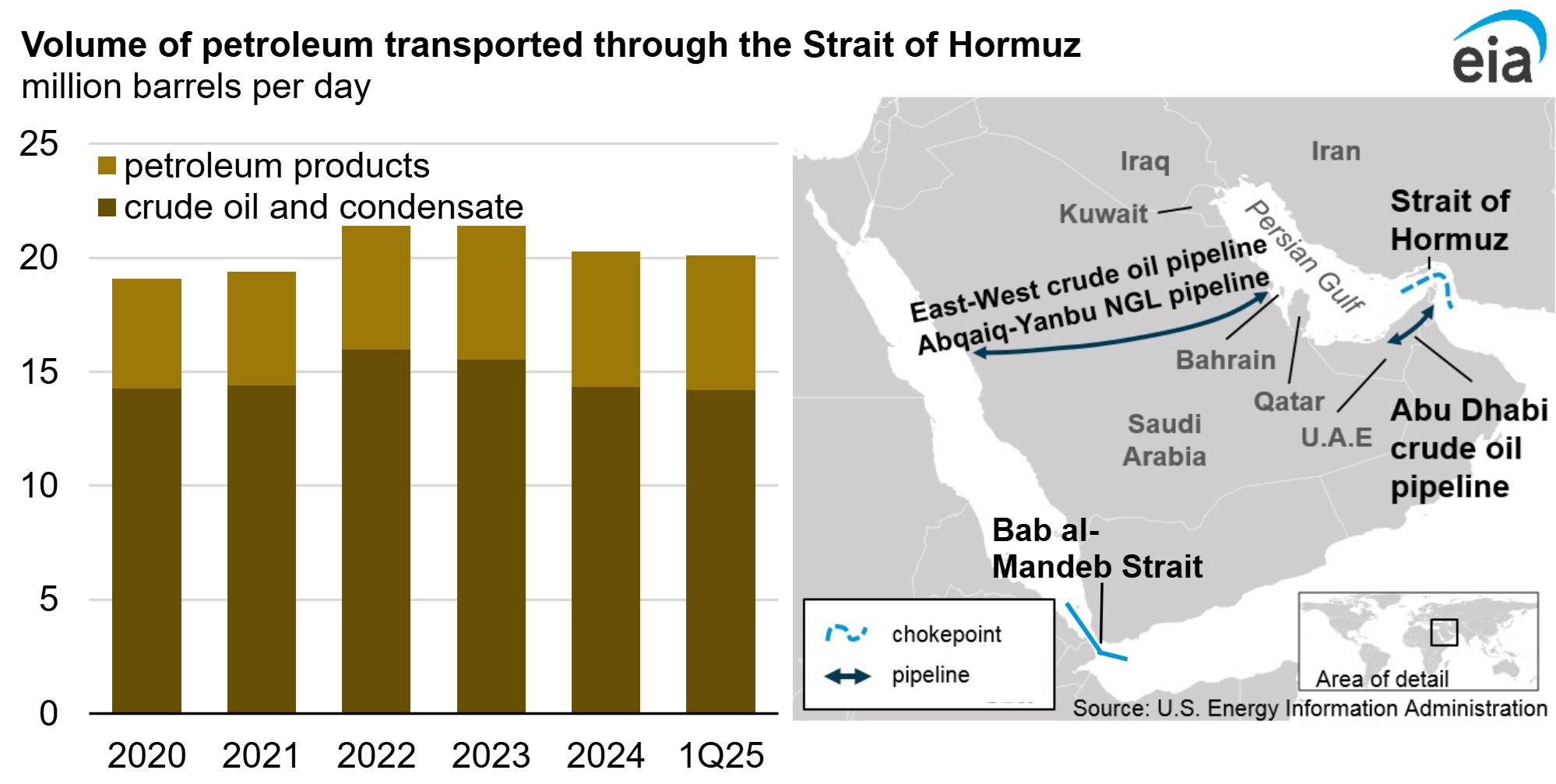

Roughly one-fifth to one-third of the world’s seaborne oil exports flow through the narrow Strait of Hormuz, the world’s most important (and potentially vulnerable) energy chokepoint. Iran has the ability to disrupt or close the strait, which could raise oil prices sharply as markets reprice the geopolitical oil premium.

The risk of a protracted war that materially lifts energy prices for an extended period could raise recession risk. That possibility still looks low at the moment, even after factoring in the Iran-related threat and Monday’s sharp increase in Brent, the international benchmark for crude oil. But much depends on how long the conflict lasts, how it evolves, how high energy prices rise, and how the war affects inflation and interest rates.

For the moment, the US economy remains relatively resilient to blowback from the war, in part because America has become a net exporter of oil in recent years due to the substantial rise in crude oil production related to advances in hydraulic fracking technology and the so-called shale revolution. As a result, the risk of another 1973 oil crisis is low, at least for now.

But low risk isn’t zero risk and the potential for economic fallout in the worst-case scenario could be significant. Exactly what that looks like and how it unfolds is speculative at this point, but the initial reaction in the stock market suggests that investors are assessing the fallout risk as low to moderate, based on the S&P 500 Index’s fractional rise in Monday’s trading, even though oil prices surged.

These are still early days, however, and it’s too early to confidently judge the depth and breadth of the macro risk that could be lurking. One reason for caution and reserving judgment: the odds currently appear low for a negotiated settlement. President Trump on Monday said the timeline for ongoing strikes could stretch out to four or five weeks, and he hasn’t ruled out putting US troops into Iran.

Meanwhile, Iran shows no sign capitulating. As we write, news reports highlight that Iran’s retaliatory strikes are widening, including hitting the American Embassy in Riyadh, Saudi Arabia.

It’s an open question how long Tehran can hold out against the combined military forces of the US and Israel, but early indications suggest that the regime is calculating that standing firm and lashing out is the less-dangerous path for survival.

From a US economic perspective, the war still appears to be a low-risk event in terms of triggering recession, but the calculus could change quickly, depending on how events unfold, particularly with respect to energy prices.

For now, the data suggest resilience, not recession. But with geopolitics suddenly sitting in the driver’s seat, the next several weeks will determine whether this remains a contained shock or the first chapter of a more consequential economic story.