Hiring Rebounds, But Fed Path Still Looks Foggy Ahead of Dec. 10 Rate Decision

By James Picerno | The Milwaukee Company

September payrolls rose more than expected, signaling growth momentum in Q3 despite earlier fears

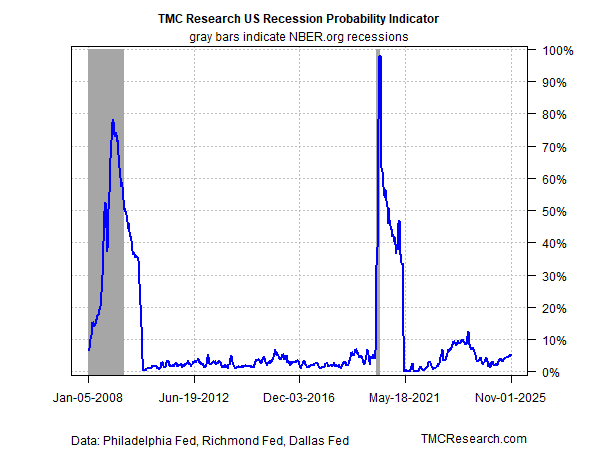

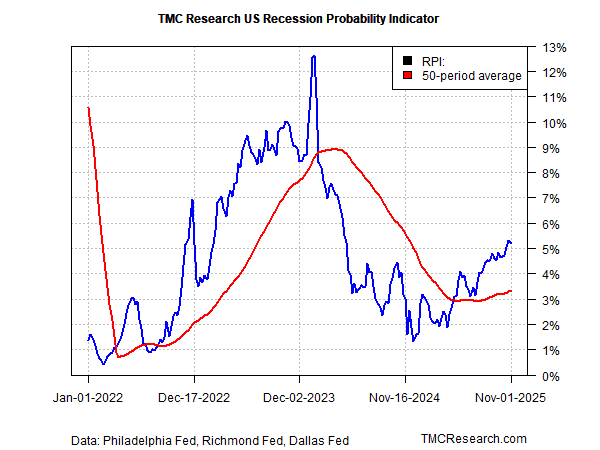

The TMC Recession Probability Indicator shows a low chance of economic contraction for now

With no October jobs data scheduled, and diverging economic views, policymakers are flying blind ahead of the December policy meeting

US jobs rose in September, increasing more than expected, according to the shutdown-delayed report from the Labor Department. The increase strengthens the view that the third-quarter GDP report, when it’s finally published, will reflect robust economic activity.

Looking deeper into the jobs report, however, continues to raise questions about what’s in store for the months ahead. Although hiring recovered to the strongest gain in five months, the year-over-year trend continues to weaken, slipping to a 0.9% advance in September, the softest since the pandemic was raging. In addition, August payrolls were revised to a loss of 4,000 jobs, while July’s gain was adjusted down to 72,000, leaving employment for the two months a combined 33,000 lower than earlier reported. The unemployment rate, which is tabulated separately from the payroll numbers, ticked higher to 4.4%, the highest in four years.

The debate about the economy’s near-term outlook – and the implications for interest-rate cuts by the Federal Reserve – remains unsettled. Both sides can point to numbers that favor, or reject, a case for a third rate cut this year at next month’s policy meeting, but a consensus at the central bank looks increasingly elusive.

Fed funds futures in recent days have been volatile, shifting from a coin toss on the odds for more easing at the Dec. 10 policy to a modest edge for predicting no change in rates later in the week. The latest update shows the futures market again showing favorable odds for a cut.

One of the few points of clarity is that a US recession still looks like a low probability for the near term, based the TMC Recession Probability Indicator (RPI), which aggregates data from three business-cycle indicators published by regional Fed banks (see here for details). The current reading (via numbers through Nov. 1) implies a roughly 5% likelihood that the economy is contracting.

A closer look at daily numbers for RPI reminds that while recession risk still appears low, it’s been edging higher lately, which suggests that headwinds could be building for early 2026. Meantime, short of a macro shock, the indicator appears unlikely to signal a recession warning in the immediate future.

Supporting RPI’s low-recession-risk estimate is the latest nowcast for the delayed third-quarter GDP report, which is expected to accelerate to a strong 4.2% seasonally adjusted annual rate, according to the Atlanta Fed’s GDPNow model (as of Nov. 19) – up from Q2’s robust 3.8% advance.

The question is whether the momentum carries over into the fourth quarter? Answering will be tougher than usual now that the Labor Department canceled the October jobs report, citing the government shutdown, which prevented the agency from collecting data last month.

The data void arrives at a time when divisions within the central bank have deepened on opinions for whether it’s timely to cut rates again next month.

“In discussing the near-term course of monetary policy, participants expressed strongly differing views about what policy decision would most likely be appropriate at the committee’s December meeting,” Fed minutes said for the Oct. 28-29 policy meeting.

Chicago Federal Reserve president Austan Goolsbee, who’ll cast a vote at the Dec. 10 policy meeting, is on the fence on how to proceed. “I’m not decided going into the December meeting,” he said this week, before the September payrolls report was released. “I am nervous about the inflation side of the ledger, where you’ve seen inflation above the target for 4.5 years and it’s trending the wrong way.”

Fed Governor Waller, by contrast, supports a rate cut. Speaking at a conference on Monday, he said: “I am not worried about inflation accelerating or inflation expectations rising significantly. My focus is on the labor market, and after months of weakening, it is unlikely that the September jobs report later this week or any other data in the next few weeks would change my view that another cut is in order.”

Normally, these disagreements would move closer to a consensus view as incoming data is published ahead of the rate decision. But thanks to the government shutdown and other factors, these are far from “normal” times.

“What do you do if you’re driving in the fog?” asked Fed Chair Powell late last month. “You slow down.”

Three weeks later, the analogy remains timely. Leaving rates unchanged, as a result, remains a reasonable policy choice until the data fog lifts.