Will Economic Contraction In The First Quarter Speed Up The Timeline For Fed Rate Cuts?

By James Picerno | The Milwaukee Company

Rate cut expectations have risen, but Fed officials remain cautious amid tariff-related inflation risk.

US Q1 GDP fell 0.3%, mainly due to import-related accounting effects.

Inflation is still moderating, supporting the case for a rate cut.

Few analysts on Wall Street were surprised to learn that the US economy downshifted in the first quarter after Q4’s solid gain. Signs of a slowdown have been showing up in various data reports for weeks, but a contraction was considered unlikely for the first three months of the year.

The worst-than-expected comparison for GDP in Q1 has strengthened expectations that the Federal Reserve will start cutting interest rates, although a closer look at why the economy shrank in the first three months of the year still leaves room for debate about the timing and magnitude for easing monetary policy.

On its face, the 0.3% decline in Q1 GDP (seasonally adjusted annual rate) looks worrisome, but the decrease is misleading to a degree because it was driven by a surge imports, which subtract from GDP in the government’s accounting rules. The import-related reduction in GDP was nearly 5 percentage points, the biggest quarterly reduction on record (since 1947).

The unusually large negative impact from imports was reportedly the result of frontloading purchases ahead of tariffs. But the increase in offshore buying may overstate the real-world effect on US economic activity.

Focusing on monthly data for consumer spending through March points to a slowdown in economic activity, but not a contraction. Personal consumption expneditures in Q1 – the single-biggest economic factor, representing nearly 70% of GDP – slowed to a 1.8% increase from 4.0%, for example.

The red ink for GDP in Q1 may be disingenuous, but a downshift in economic activity still appears to be unfolding. In turn, a softer trend suggests the Fed is that much closer to cutting interest rates. But in the current climate, the “normal” business-cycle factors may not apply, according to recent comments by Fed officials. The reasoning: tariffs may lift inflation, if only temporarily, even if economic activity slows, Federal Reserve governor Chris Waller said last month.

Inflation, however, still looks relatively tame as it continues to trend lower, based on the Fed’s preferred set of price deflators. Headline PCE inflation eased to a 2.6% pace in March vs. the year-ago level, the lowest since September; core PCE decelerated to a 2.7% increase, also the lowest since September. Inflation remains above the Fed’s 2% target, but the trend still moving in the right direction.

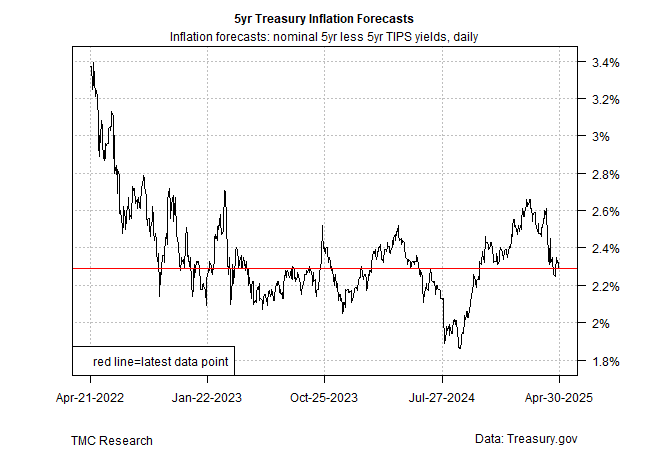

Waller noted that he favors the Treasury market’s implied inflation forecast for monitoring expectations, a crucial input for evaluating the outlook. By that yardstick, the 5-year breakeven inflation rate (nominal 5-year yield less its 5-year counterpart) was 2.29% on Wednesday (Apr. 30), which is roughly in line with the pre-tariff turmoil.

TMC Research’s Fed funds model continues to indicate a bias for cutting interest rates. Our current estimate of the neutral rate is more than one percentage point below the median Fed funds target rate. That’s close to the widest difference since October and a sign that Fed policy has become passively restrictive (i.e., a tightening of monetary policy by leaving rates unchanged when economic conditions appear to be weakening without a material increase in inflation).

The Fed recently noted that it remains in a wait-and-see mode and is monitoring the data for signs that inflation may heat up due to tariffs. But the effects from tariffs have yet to show up in the data. Upcoming reports could reveal otherwise, of course. Meantime, there’s a risk that monetary policy remains unchanged as the economy continues to weaken, a combination that threatens to exacerbate the slowdown in some degree.

The Fed is struggling with deciding if inflation will continue to ease (or hold steady) as the effect from tariffs works their way through the economy. But obtaining clarity on that question will take time. Meanwhile, growth is weakening. The Fed’s window of opportunity is narrowing for being proactive with rate cuts to support economic activity and minimize a future downturn. Political pressure also appears to be increasing as President Trump has reiterated calls for immediate rate cuts and openly questioned the Fed’s cautious approach.

The Fed funds futures market is currently pricing in a virtual certainty that rates will remain unchanged at the May 7 policy meeting, and a roughly 60% probability that the first rate cut will be announced at the June 18th FOMC meeting.

Waiting till June, however, could allow negative economic momentum to accelerate. The Fed seems to be betting that inflation will pick up and become its primary focus for policy decisions. Even if that turns out to be an accurate forecast and appropriate policy stance, it may come at a price of strengthening economic headwinds.