US Fiscal Risk Edges Higher, Yet Remains Within Post-Pandemic Range

By James Picerno | The Milwaukee Company

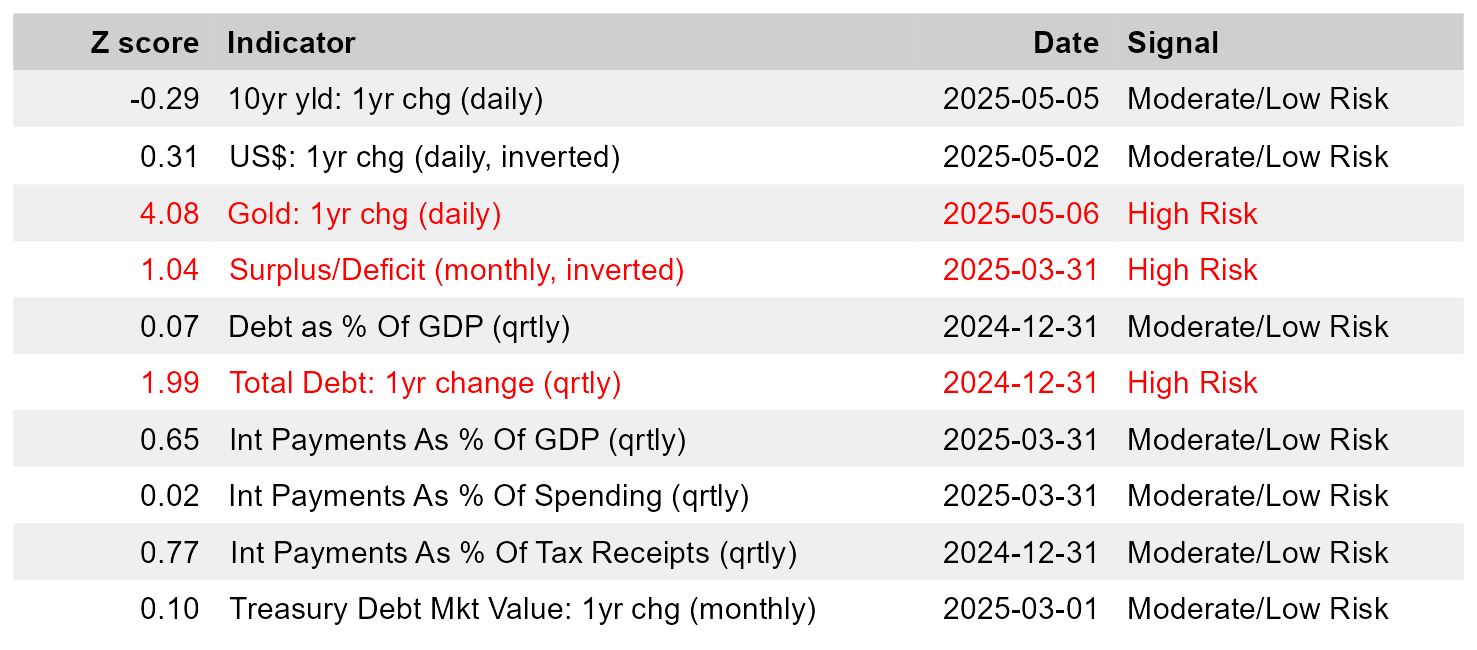

US fiscal risk has increased, with three indicators signaling high risk, up from two in our previous update that tracks ten data sets.

Despite the latest increase, overall fiscal risk remains in a range that’s prevailed post-pandemic.

Rising interest-rate payments as a percent of tax receipts may be the next indicator to shift to a high-risk profile.

US fiscal risk increased in the first quarter, according to analysis of newly released government data. The change is based on reviewing a framework developed by TMC Research for monitoring key factors related to the federal government’s overall risk profile.

For the ten indicators we focus on to track fiscal risk, three are reflecting a high-risk score, up from two in our previous update. The third indicator that switched to a high-risk reading in today’s update: the federal government’s deficit through March, as reported by the US Treasury. The other two metrics that remain in a high-risk stance: 1-year changes for the price of gold and the total amount of government debt.

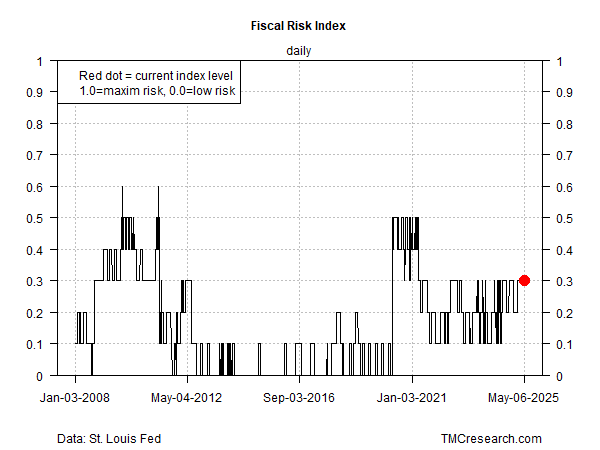

For a clearer view of how all the numbers in the table above are changing overall, The Fiscal Risk Index aggregates the data into a single indicator (see chart below). Although this reading edged up to 0.3, it remains in a range that’s prevailed in the last several years following the spike during the pandemic. Values range from 0 (low/nil risk) to 1.0 (extreme risk), and on that basis the current 0.3 level suggests a moderate degree of risk. That may strike readers as unreasonably tolerant, but keep in mind that the goal of these updates is to compare the relative changes in fiscal risk based on key signals from markets and federal budget numbers, and on that basis one can argue that conditions have only changed on the margins compared with recent history.

To put all numbers in the table above on a level playing field, the data are transformed into z-scores. A z-score quantifies how many standard deviations (a measure of volatility) a data point exceeds or falls below the average. In the modeling presented, changes that exceed +1 z-score equate with a relatively “high” state of risk. A change below +1 z-score is considered “normal,” which is to say a relatively “moderate” or “low” risk readings. Z-scores of +1 or -1 are selected as first approximations for evaluating “significant” changes in the data. The main objectives: quantifying how the changes compare vs. the other indicators and tracking the changes through time.

For context on how risk is evolving overall vs. history, all ten indicators are combined and tracked in the Fiscal Risk Index (FRI), which provides a top-down view of the data. At the moment, the FRI indicates a relatively middling level of risk compared with the readings after the pandemic-induced spike.

Note that two indicators that are currently assigned a moderate/low risk level may be poised to switch to high risk in updates later this year. Federal government interest payments as a percent of tax receipts are currently posting a 0.77 z-score, which is only moderately below the +1.0 trigger line. Another fiscal indicator that could soon cross into high-risk terrain: interest payments as a percent of GDP (currently at a 0.65 z-score).

Keep in mind that no one knows exactly where genuine tipping points lie for the data sets above. Financial markets may ultimately have the last word for deciding what’s a relevant risk level, but it’s unclear in advance when the crowd will demand sharply higher risk premia going forward. Presumably, there is a line that, when crossed, will trigger a higher level of blowback for the markets, the economy and the government.

The ten indicators and the selected parameters, rather than offering the last word on the discussion of fiscal risk, are offered as a first step in deciding how the US government’s debt burden is changing. Comparing changes through time is especially useful. Although most government observers agree that red-ink risk has become more challenging in recent years, the Fiscal Risk Index suggests that the threat, if only in relative terms, has yet to rise above the range that’s prevailed since the pandemic was raging.