The World’s Debt Alarm Is Ringing—Will Treasuries Hear It Next?

By James Picerno | The Milwaukee Company

Japan’s yield surge is sharpening global attention on fiscal strain and debt risk

Dollar softness, soaring gold, and rising debt metrics add to the pressure

A sustained climb in the US 10‑year yield could be a sign that markets are pricing in higher fiscal risk

Economists have long warned that US government debt is on an unsustainable upward path. Markets, however, have downplayed the risk of fiscal strain. But in the wake of a sharp rise in Japanese bond yields in recent days, concerns about fiscal profligacy are starting to focus minds and the macro implications are resonating across international markets. A key question: Will the US Treasury market start to feel the heat, too?

Earlier this month TMC Research reasoned that Treasury yields could play a bigger role with determining the overall appetite for risk this year. At the moment, key US government yields continue to trade in a range, albeit after rising moderately in recent weeks. The benchmark 10-year Treasury yield, for example, after briefly trading below the 4.0% mark in late-2025, last week rose above 4.30% for the first time since August before pulling back to end yesterday’s session at 4.22%.

Global investors are closely monitoring the rise in Japanese bond yields, in part because the country’s long run of ultra-low rates appears to be fading. If the rise in yields continues in Japan, the effects could reverberate around the world and affect demand for government debt in other nations.

One line of reasoning is that as Japan’s yields rise, the higher rates may attract assets – particularly in Asia – that previously flowed into US Treasuries. Japan’s 10-year yield, for instance, has in recent weeks jumped above 2% for the first time in more than 25 years. If the increase continues, Japan’s government bonds will become more competitive in the global hunt for buyers — an increasingly essential challenge as government debt levels rise.

Nearly 13% of the US Treasury market is held by investors in Japan and throughout Asia. If Japanese bonds attract more buyers, the shift could be a factor that raises US yields if demand on the margin falls.

Red Ink Risk

Although it’s debatable if the Japan factor will directly affect US yields in a meaningful degree, the discussion comes at a time of elevated concern about government debt, in America and around the world.

A key reason why Japanese yields have shot higher in recent days: Prime Minister Sanae Takaichi is heading into the country’s Feb. 8 general election on a platform of tax cuts and stimulus spending, which threaten to further exacerbate the country’s debt burden, according to some critics. It’s no trivial issue for Japan, which has the highest gross debt-to-GDP ratio among developed countries: roughly 230% in 2025, according to Statista.

The US debt-to-GDP ratio is substantially lower, but it’s still concerning, in no small part because it’s increased in recent years and Washington shows little appetite for making meaningful reforms.

US debt as a share of GDP was roughly 121% as of 2025’s third quarter — close to a record high in the modern era — and is on track to rise further, to 134% by 2035, according to a recent estimate by the Committee for a Responsible Federal Budget, a self-described non-partisan think tank in Washington.

Economic Growth, Or The Lack Thereof, Will Be Crucial

A more immediate risk is less about the level of debt vs. the cost of servicing the red ink. A critical metric to watch: Federal government interest payments, which have surged in the last several years and now routinely top $1 trillion on a seasonally adjusted annual rate basis (as of 2025’s third quarter).

The key variable is how the rate of growth for debt payments compares with economic growth. If the economy can expand faster than the average interest rate paid on debt, the US federal debt challenge could be manageable and avoid sparking a crisis.

Economic growth, in short, is the essential variable since it will play a big role in determining if the government can, in time, grow its way out of its fiscal hole. If not, higher inflation, deeper deficits, and higher interest rates may be lurking.

Dollar Risk

Treasury yields are one of the main real-time proxies for measuring perceptions on how the US is faring with debt management. Another is the ebb and flow of the US dollar in foreign exchange markets. On that front, forex risk is looking more worrisome lately as the value of the greenback slides.

The US Dollar Index (a weighted basket of the dollar against the six major foreign currencies) has slumped in recent days and is trading near the lowest level in four years. A sustained drop below current levels could unleash a technically bearish posture that triggers more selling, pushing the US currency even lower, which implies higher inflation and interest rates.

In that scenario, the Federal Reserve may be persuaded to put rate cuts on hold for longer than expected, and perhaps even start raising them again. The Fed funds futures market, by the way, is pricing in high odds that the central will leave its current target rate unchanged at tomorrow’s FOMC meeting.

Unsurprisingly, gold has been soaring lately, in part due to a weak dollar. Earlier this week the precious metal topped $5,000 an ounce for the first time. Analysts cite a combination of drivers, including elevated geopolitical risk, the dollar’s slide, and concerns about debt-driven fiscal instability.

Monitoring Fiscal Risk

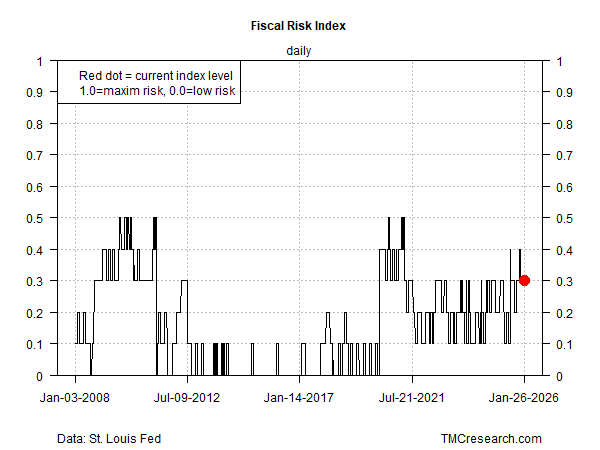

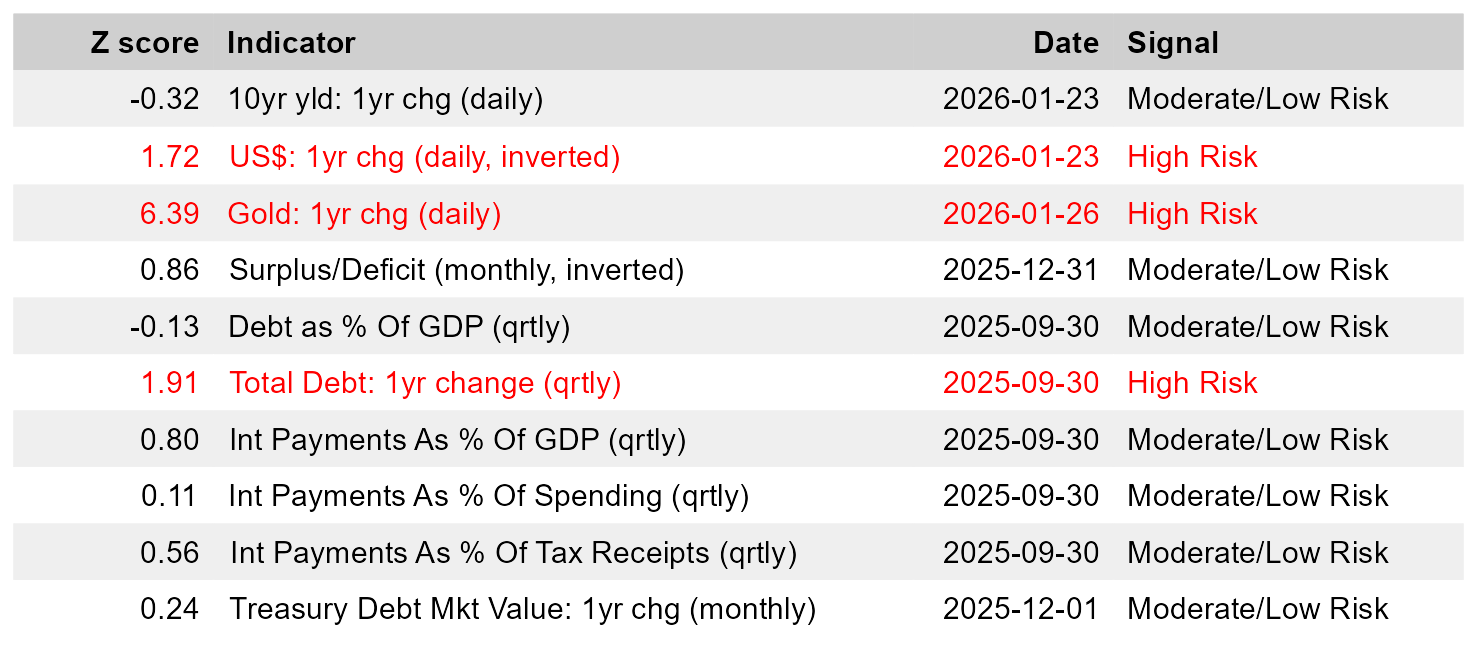

US fiscal risk overall hasn’t changed much in recent months, according to a model developed by TMC Research. The current reading of our Fiscal Risk Index (FRI) is 0.3. That’s near the higher end of recent history, but still below the previous peak of 0.5 that was briefly reached soon after a surge in pandemic-related government spending. (FRI values range from 0, which is low/nil risk, to 1, or extremely high risk.)

Among FRI’s ten inputs (see table below), the starkest warnings at the moment are coming from dollar weakness, surging gold prices, and a relatively hefty increase in total government debt over the past year.

For now, US stock and bond markets appear relatively calm with respect to risks tied to dollar weakness, fiscal deficits and inflation. To the extent sentiment changes, and investors demand a higher risk premium, an early clue of an attitude adjustment will likely show up as a sustained rise in Treasury yields.