The Federal Reserve Is In The Hot Seat Today As Stagflation Risk Lurks

By James Picerno | The Milwaukee Company

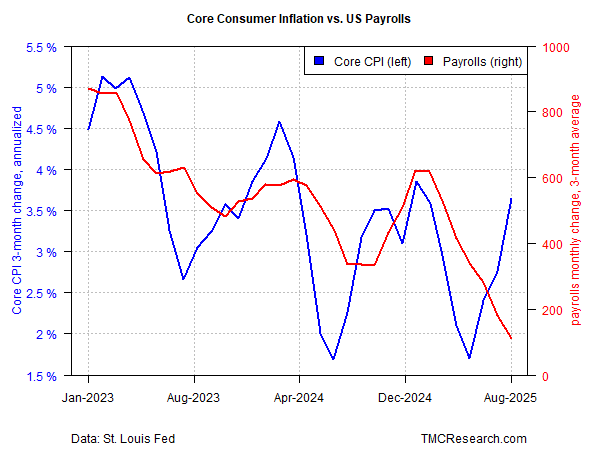

The Fed’s dilemma deepens as hiring slows an inflation edges higher

Core CPI has accelerated for three straight months while the trend in payrolls growth has slowed since February, hinting at early-stage stagflation

Markets expect a rate cut at today’s policy announcement, but Wall Street will be left wondering if the decision risks stoking inflation

A whiff of stagflation hangs over today’s interest-rate decision for the Federal Reserve.

These are still early days for evaluating if stagflation – slowing growth accompanied by rising inflation -- is a serious risk, or not, in the months ahead. What is clear is that the inflation-payrolls dynamic at the moment could be an early warning.

As shown in the chart below, the core rate of the Consumer Price Index (CPI) has accelerated in each of the three monthly updates through August, based on the annualized 3-month change (blue line). Meanwhile, the average 3-month change for non-farm payrolls (red line) has been sliding since February, dropping in August to the weakest level since the pandemic was raging in late-2020.

Is It Different This Time?

The pickup in inflation, and the slowdown in hiring, are still relatively moderate compared with the extreme stagflationary episodes of the past, such as during the 1970s. In a “normal” business-cycle slowdown, weaker payrolls growth is expected to lead to softer inflation. The question is whether this time is different?

Some economists think it is, partly because the introduction of tariffs in the spring has changed the calculus — a change that puts the Fed in a bind.

The central bank’s primary mandate is maximizing employment while keeping inflation at or near its target, which is currently 2%. On both fronts, success has been slipping away recently, if only on the margins.

A key problem is that monetary policy is challenged when the agenda is simultaneously containing inflation and supporting hiring. The Fed has powerful tools to address each of those objectives in isolation – particularly if risk for the other objective is relatively modest. But the efficacy of monetary policy overall starts to fade when trying to address both fronts at the same time.

That leaves the next-best option: prioritizing one objective over the other. Most of the time that’s not an issue because inflation and employment tend to be positively correlated. When inflation heats up, hiring tends to be relatively strong, thereby opening the door to rate hikes at a time when the economy is robust. The opposite is also true: disinflation or deflation generally accompanies a slowdown in hiring, and so cutting rates is optimal on both fronts.

A problem for policy arises when the trends diverge, namely: inflation accelerates and employment weakens. In that case, focusing on one policy concern threatens to exacerbate the other. Raising rates helps cool inflation, but threatens to weigh on an already weak hiring trend. The opposite challenge: cutting rates to support the labor market, which is problematic if inflation is picking up, and so easing policy can strengthen an existing run of reflationary pressure. Damned if you do, damned if don’t.

Policy Meeting To The Rescue?

Although the diverging trends between inflation and employment are still modest, there’s a growing concern that tariffs will continue to create a tailwind for inflation at a time when the economy appears to be downshifting, based on the recent slowdown in hiring.

Markets are pricing in high odds that the Fed will prioritize employment concerns by cutting interest rates. That’s a reasonable decision when considering the downside bias in payrolls in isolation. But factoring in the upside trend for inflation in recent months raises questions about the wisdom of giving pricing pressure more fuel to accelerate.

Is there a compelling rationale for cutting rates in the current environment? The Fed wants to minimize the risk that a slowing economy deteriorates into a recession. But is recession risk high enough at the moment to warrant rate cuts when inflation may be picking up? There’s room for doubt. Economic growth may be slowing, but the odds that a recession is imminent remain low, based on analysis by TMC Research earlier this week.

Meanwhile, crucial questions hang over the economy and today’s Fed meeting: Will tariffs continue to be a factor that lifts inflation? Or will softer economic growth do most of the Fed’s job in the months ahead and contain if not slow inflation, leaving the central bank with a relatively free hand to cut rates to support growth?

Tough questions, which will be front and center at today’s press conference with Fed Chairman Jerome Powell following the policy announcement at 2:00pm eastern.