Resilient, Not Immune: The US Faces an Energy Stress Test

By James Picerno | The Milwaukee Company

Inflation is rising on the energy shock, but growth indicators still look resilient

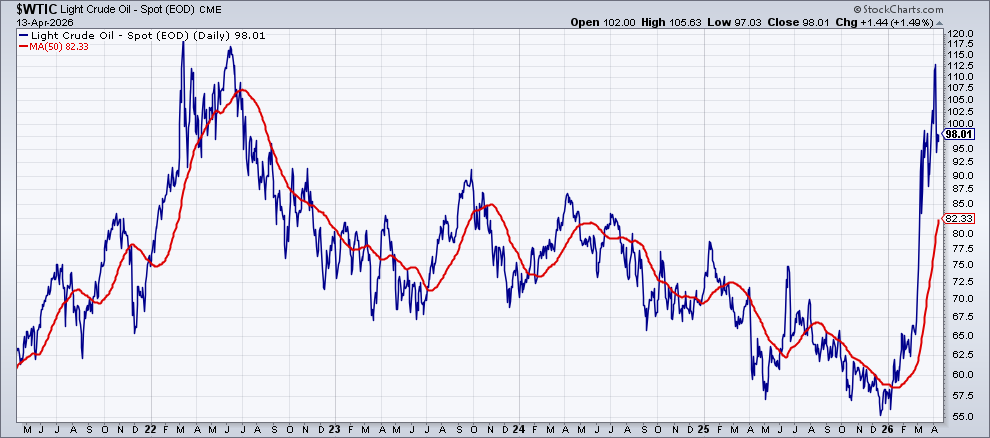

Oil’s 50‑day average is above $80, which suggests energy risk is becoming elevated

Fed policy is still on hold for now

Economic risk is rising as the Middle East conflict keeps energy prices elevated, but several business‑cycle indicators tracked by TMC Research suggest that the war’s negative effects remain limited for the US economy so far.

The situation remains fluid, and facts on the ground can quickly change the analysis. Current data, however, indicates that economic activity remains relatively resilient. Conditions could deteriorate, but it’s encouraging that, for now at least, the war’s blowback has yet to make a meaningfully negative impact.

Oil prices remain the critical variable. The recent spike pushed the US benchmark (West Texas Intermediate) above $112 a barrel last week, but the price quickly pulled back and remains just below $100 (as of Apr. 13). The run‑up in price volatility is worrisome, but the main risk is if oil stays elevated for an extended period. In that scenario, energy prices generally will remain high, which could trigger demand destruction and raise inflation.

The challenge is defining what counts as “elevated,” and for how long? One way to monitor the risk is by tracking the 50‑day average price of oil, a crucial input that filters through the economy. Economists debate where the tipping point lies for signaling a danger zone. A reasonable starting point is watching the rolling 50‑day price: a rise into the $80–$100 range that persists for a month would be a warning sign that energy costs are poised to threaten the economic outlook.

The 50‑day average has recently crossed above $80, suggesting that the outlook for inflation and economic activity is starting to look worrisome (red line in chart below).

The supply‑side energy shock has already lifted inflation. The Consumer Price Index (CPI) at the headline level rose to a two‑year high of 3.3% for the year‑over‑year change through March—sharply above February’s 2.4% increase. TMC Research estimates that the longer the 50‑day average stays above $80, the higher the odds that inflation will hold at current levels, if not rise further, for some period of time.

Economic activity, however, has yet to show a meaningful impact from the war so far. One example is the Dallas Fed’s Weekly Economic Index (WEI), a real-time measure which continues to reflect year‑over‑year economic growth at a mid-2% pace, based on data through Apr. 9.

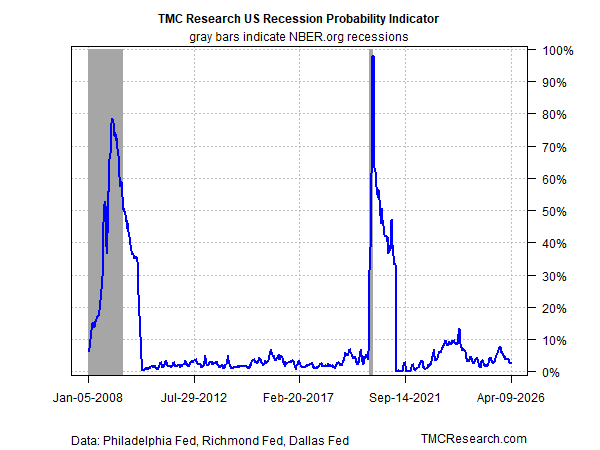

TMC Research’s model for estimating US recession risk in real time still reflects a low probability that an NBER-defined contraction has started or is imminent, based on data through early April. Our US Recession Probability Indicator aggregates and models data from three business-cycle indicators published by regional Fed banks (see here for details).

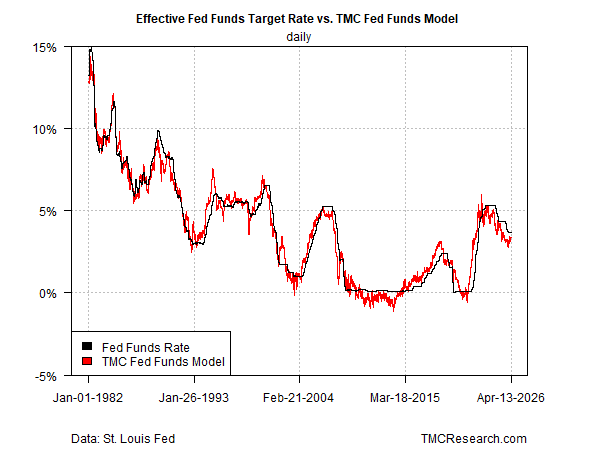

Market expectations are still anticipating that the Federal Reserve will leave its target rate unchanged for the foreseeable future, based on Fed funds futures. That suggests the debate remains open about the severity of the inflation threat.

Several policymakers at the central bank are considering that rate hikes may be needed to counter inflation, according to the minutes of the March 17-18 meeting. “Some participants judged that there was a strong case for a two-sided description of the [Federal Open Market] Committee’s future interest rate decisions in the post-meeting statement, reflecting the possibility that upwards adjustments to the target range for the federal funds rate could be appropriate if inflation were to remain at above-target levels,” the minutes said.

TMC Research’s Fed Funds Model estimates that monetary policy continues to reflect a modestly hawkish bias. That stance may give the central bank time to determine whether the war‑driven increase in inflation is temporary or requires a new round of rate hikes. For now, keeping policy steady appears to be the more likely path.

Oil remains the critical variable in the near term. The latest sentiment on Wall Street leans toward cautious optimism that a peace deal with Iran is still possible following failed negotiations over the weekend and Monday’s implementation of a blockade of maritime traffic to and from Iran’s ports.

“I can tell you that we’ve been called by the other side,” Trump told reporters on Monday. “They’d like to make a deal very badly. Very badly.”

The war hasn’t broken the cycle yet. Whether it stays that way may depend on how long oil prices stay elevated. The economy can absorb a lot, but the clock is ticking. If oil keeps grinding higher, the pressure may reach a tipping point.