Oil Spike Lifts Recession Risk, But Outlook Still Depends on Broader Conditions

By James Picerno | The Milwaukee Company

Oil’s rise is adding to recession risk, but history suggests the signal remains mixed

The US is less sensitive to energy shocks than in past cycles

The war’s impact on global supply and sentiment in the weeks ahead will determine how much risk ultimately materializes

Oil has been a central pressure point in most US economic downturns of the post‑WWII era, but not every spike in the commodity automatically leads to a recession.

Higher oil prices clearly raise economic risk, largely because crude is a primary feedstock, influencing a wide range of products, services, and prices. A sharp rise in energy costs tends to ripple across the economy. But the effects vary, depending on the economy’s strength at the time of the price jolt, prevailing financial conditions, and how long the surge lasts.

The risk from an oil shock can be significant, although the potential for blowback is lower than in previous decades. One reason: the US is less vulnerable than many other countries because America pumps more oil than it consumes. Another advantage: lower energy intensity. The amount of oil needed to generate a given unit of GDP has fallen sharply in recent decades.

Lower risk isn’t zero risk, however, in part because oil is priced globally, as TMC Research discussed earlier this month. That means higher energy costs stemming from disruptions in Middle East exports will spill over to the US to some degree.

Gauging how much of a shock the economy will absorb is challenging because the medium‑term effects of several key variables remain unknown. At the top of the list: How long will the war last, how quickly will Middle East exports rebound toward normal levels, and how will US consumers and businesses respond in the interim?

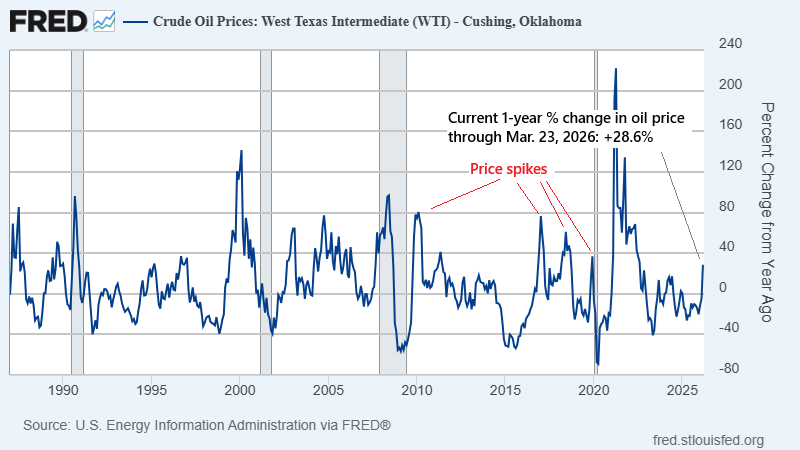

What we do know is that previous oil spikes don’t always line up with recessions. Consider the year‑over‑year changes in the US oil benchmark — West Texas Intermediate (WTI) — in relation to economic contractions, as defined by NBER.org, the official arbiter of the US business cycle. The key lesson: recession risk rises when oil prices rise sharply, but the relationship varies because other macro conditions matter, too. Higher energy costs usually slow growth, but to varying degrees, depending on other conditions that are unique to each point in time.

For example, following the economy’s recovery from the financial crisis in 2008 through the eve of the pandemic in early 2020, oil rose sharply relative to the year‑ago level on four separate occasions. In each case, the economy sidestepped a business-cycle recession, even if there was a price tag to some degree.

The reasons why an oil shock may or may not push the economy over the edge vary. Energy is a crucial factor for the business cycle, but conditions matter in other areas, such as interest rates, the labor market, consumer spending, and the pace of economic activity going into the spike, to cite a few examples. These and other macro factors play a role in determining how a rise in energy prices will affect growth and inflation.

It’s also worth noting that the current increase in oil — approaching a 30% year‑over‑year gain, based on prices through Mar. 23 — is a hefty change from recent history. But the increase, so far, is still well below changes associated with the three recessions prior to the pandemic, which was unusual in the extreme and therefore of limited value for studying business‑cycle behavior.

If oil prices continue to rise, recession risk will follow. But until there’s more clarity on how the economy adapts to the war’s effects and the associated run‑up in oil, there’s still room for debate over whether a US recession is inevitable.

The determining factors that will have the last word are the war’s duration and the degree to which it constrains global energy flows and influences risk sentiment in the US and abroad.