US Pumps More Oil Than Ever, But The Commodity Is Still Priced Globally

By James Picerno | The Milwaukee Company

Oil trades in one global market, so US prices move with worldwide supply, demand, and geopolitical shocks

Fungibility, dollar pricing, and arbitrage keep benchmarks aligned, limiting any country’s pricing power

No one nation controls enough supply to set prices, leaving global forces—not domestic output—in charge

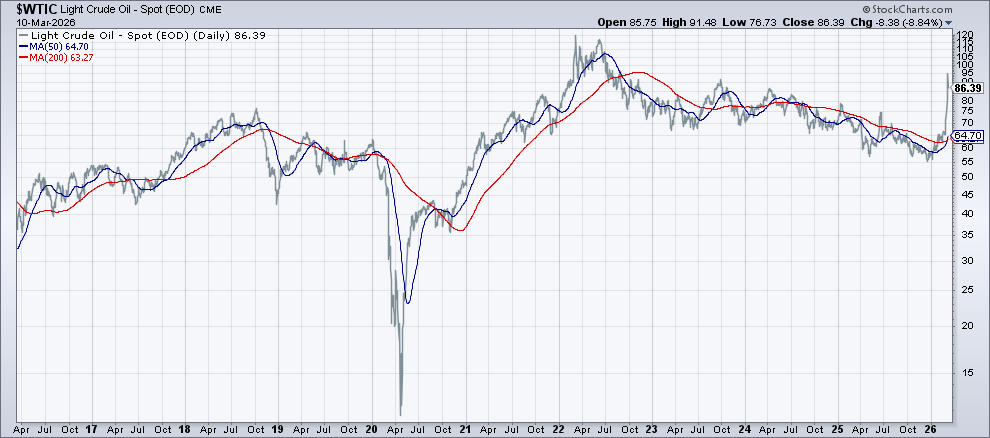

The United States may be the world’s largest oil producer and a net exporter, but that doesn’t fully shield America from price spikes when global supply is jolted by events like the war in Iran.

Oil is priced in a single worldwide marketplace, which means that shifts in supply, demand, and geopolitical risk spill across borders regardless of how much a country produces. When global benchmarks jump, US prices follow because American barrels compete with — and are valued against — the same international forces that apply to all countries.

A useful analogy for how oil prices are set was outlined in a 2009 speech by Yale University Professor William Nordhaus, who explained the oil market as a giant bathtub holding the global supply of inventory. There are spigots of incoming oil from multiple countries that fill the tub, along with various drains that represent purchases. “The price and quantity dynamics are determined by the sum of these demands and supplies and the level of total inventory, and are independent of whether the faucets and drains are labeled ‘US,’ ‘Russia,’ or ‘Denmark.’”

Why Oil Prices Converge Worldwide

Oil is priced globally rather than locally for several reasons, starting with fungibility – the commodity is interchangeable with barrels of the same grade and quality around the world. There are two main benchmarks: West Texas Intermediate (WTI) for the sweet (low-sulfur) US grade, and Brent, the international benchmark for high-grade oil pumped outside the US. Although there are a number of other grades, standardizing the commodity in these two buckets fosters global pricing.

To the extent that pricing moves out of line in one trading venue vs. another, arbitrageurs exploit the gap for profit, which helps keep pricing in alignment around the world. Local price differences can still arise, if only at the margins, due to other factors, such as infrastructure bottlenecks, shipping constraints, and regulatory issues. But for WTI and Brent, the law of one price tends to prevail.

Another reason why pricing is set globally: crude oil is priced primarily in US dollars. By trading in one currency, the volatility in pricing that could emerge across different currencies is muted and largely transferred to the local buyer, who assumes any foreign exchange risk. Single-currency pricing, in short, promotes pricing that is directly related to global economic conditions.

Another driver that strengthens global pricing: the commodity is the primary raw material (feedstock) for a wide variety of fuels and products used nearly everywhere, with transportation as the main source of demand. Upwards of 85% of crude is refined into gasoline, diesel and jet fuel. The rest goes to produce petrochemicals, plastics, numerous consumer products, and beyond.

The rise of electric vehicles threatens to pare oil’s transport-related demand, but for the foreseeable future the transition is expected to be modest and gradual. Meantime, oil remains integral to most economies around the world, which translates to a relatively steady state of global demand.

No Country Controls the Price

The key result is that no single country, no matter how much it produces, has more than a marginal influence on global pricing. OPEC, the oil cartel that represents countries with about 35% of the world’s output, has more leverage, but it’s limited.

“OPEC membership has less to do with controlling oil prices and more to do with geopolitical and domestic political benefits,” notes a recent report by the Cato Institute, a think-tank in Washington. “The OPEC nations appear to use oil production as an international bargaining chip to provide the regimes with domestic legitimacy.”

The rise of US production in recent years, thanks to advanced drilling technologies, is not without its benefits. For starters, America no longer relies on imports to the extent that it did in decades past. Although certain grades of oil must still be imported, foreign-oil dependence is a fraction of what it was in the 1973-74 energy crisis, for example, when OPEC imposed an oil embargo on the US.

A repeat performance with deep economic effects is unlikely in 2026, thanks to the increase in US production. But one thing hasn’t changed: oil prices are still subject to global supply and demand factors, and lifting domestic output isn’t likely to change that basic framework.