Investing Isn’t Risk-free, Which is Why Risk Management is Essential

By James Picerno | The Milwaukee Company

Managing behavioral risk should be a top priority for most investors

Psychological factors can meaningfully shape investment decisions

Designing portfolios that help investors live with market volatility is essential

Risk management matters for several reasons, but it starts with a simple fact: investment losses don’t always behave symmetrically.

This mismatch threatens to weaken an otherwise sound investment plan because behavioral risk can spike when markets decline. In those periods, the average investor is prone to letting emotions drive ill-timed decisions that can have adverse effects on portfolio performance for years.

For most investors, there’s a strong case for managing portfolios in an effort to soften the periodic volatility spikes that are part of the normal ebb and flow of markets through time.

There are several reasons why developing portfolio strategies can help cushion short-term declines, which can trigger behavioral mistakes. A review of the math tells the story and illustrates why buy-and-hold investing can be so difficult to endure when markets hit a rough patch.

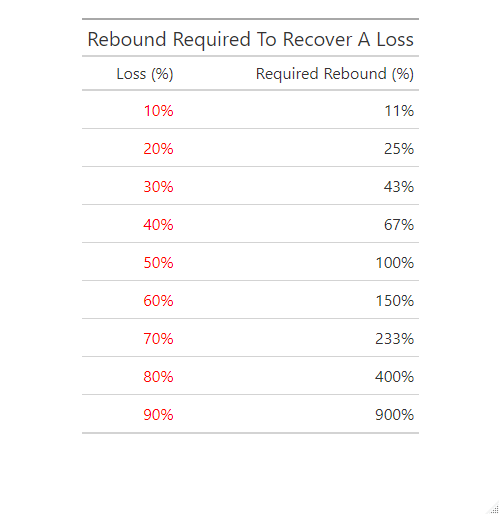

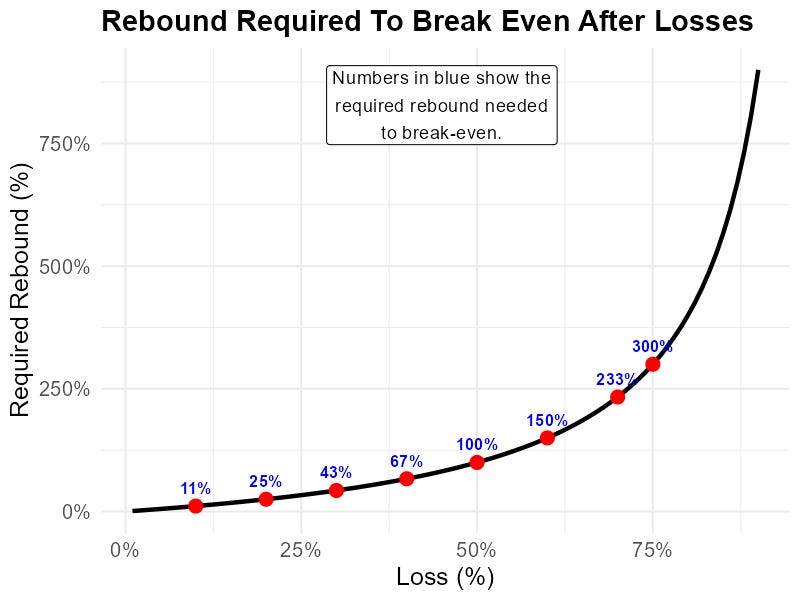

Consider the hurdle required to regain an investment loss. To fully recover from a 10% decline requires an 11% rebound. A 20% decline needs a 25% recovery, and a 30% slide is healed only after a subsequent 43% increase. As the table below shows, the math only gets uglier as losses deepen.

The chart below highlights the exponentially higher performance hurdle associated with deeper losses.

The key lesson is that while market risk can’t be avoided, it can be managed to a degree. Holding a multi-asset class portfolio is one dimension of risk management. Another is adjusting asset allocation systematically based on risk analytics, which can help minimize volatility spikes relative to a passively managed strategy.

Although risk can’t be completely avoided when investing, it is possible to reduce the odds of enduring the deepest losses that are mathematically and behaviorally difficult to recover from. The wisdom of using risk management isn’t only about outperformance, although that can be part of the strategy agenda. No less important is preparing for the emotional response that can arise during the deepest market drawdowns.

Numerous research studies over the years find that investor psychology can be a key factor in portfolio performance. Although some investors can muster the steely discipline to look through bouts of market volatility and focus on the long run, such restraint is generally rare.

The average investor, by contrast, may be vulnerable to an array of behavioral biases—fearing losses more than enjoying gains (loss aversion), following the crowd (herding), and overestimating skill (overconfidence), to name a few. Developing an investment strategy to help manage these risks is a critical input for tipping the odds in favor of achieving long-term financial objectives.

To the extent that risk management can help mute volatility spikes, it lowers the odds of emotional decisions that can disrupt long-term plans.

The point about asymmetric losses is often underappreciated in standard risk frameworks. A 50% drawdown requires a 100% gain to break even, not a 50% gain, and that mathematical asymmetry has real consequences for investor behavior and portfolio design. Many retail investors intuitively know this but still fail to act on it when markets are trending upward.

The behavioral dimension here is critical. Standard deviation and VaR metrics tell you about the distribution of outcomes, but they don't capture the human response to those outcomes. An investor who panic-sells at the bottom and chases performance on the way back up can underperform even a flat market. That execution gap is arguably the biggest source of alpha destruction, and it's rarely addressed in asset allocation discussions.

One nuance worth adding: behavioral risk management isn't just about controlling emotions in downturns. It also includes managing overconfidence and recency bias in bull markets, which may actually be the harder problem to solve systematically. Good framework to keep thinking about.