Five Key Steps to Stay Grounded When Markets Turn Volatile

By James Picerno | The Milwaukee Company

A spike in volatility is a reminder to revisit your investment plan—does it still match your goals?

Rely on process — asset allocation, rebalancing, and tax-loss harvesting

Look for opportunities to swap into lower-cost ETFs when harvesting losses

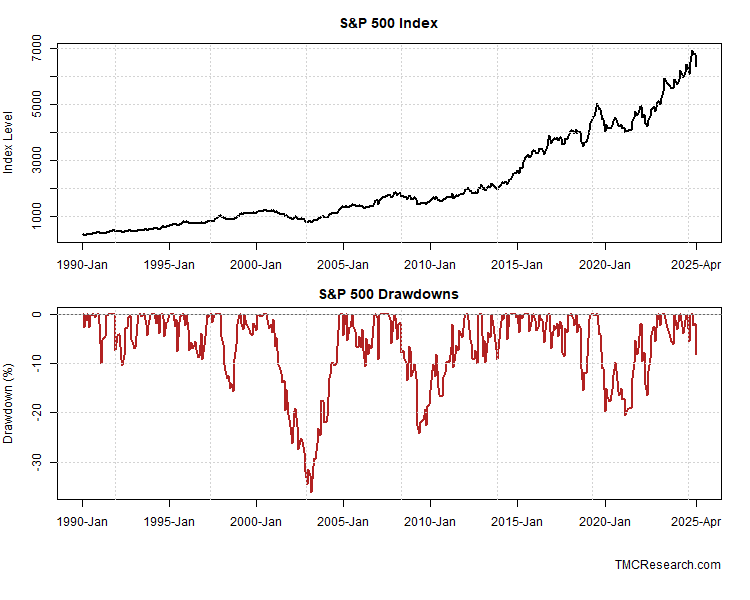

Bond yields are rising again, and some pundits say that the spillover could start to pressure stocks.

In moments like these, it’s easy to feel the temptation to retreat into cash, overhaul your portfolio, or chase whatever seems safe. But those impulses carry their own risks, and can potentially knock long‑term plans off track.

A better way to navigate periods of market stress is to treat volatility as a prompt to reassess and reinforce the parts of your strategy that actually drive long‑term results—while reducing the short‑term behavioral risks that can quietly undermine them. When markets turn rocky, these five forecast‑free tasks are worth revisiting to help keep your investment plan moving in the right direction.

Asset Allocation

Reassessing your asset‑allocation plan during periods of market stress is a practical way to make sure your portfolio still reflects your goals and your true tolerance for risk. Volatility has a way of exposing whether your mix of stocks, bonds, cash, and other assets is still aligned with your long‑term strategy—or whether market moves have quietly pushed you off target. Taking a fresh look at your asset allocation plan also gives you a clearer read on how comfortable you really are with your current level of risk when conditions get bumpy.

This isn’t about reacting to headlines or trying to time the next move. It’s about confirming that your allocation still fits your objectives, time horizon, and capacity to stay invested through uncertainty. The value proposition is straightforward: a well‑aligned asset‑allocation plan helps reduce emotional decision‑making and keeps your long‑term strategy intact when markets are most distracting.

Rebalancing

Rebalancing becomes especially valuable during periods of market stress, when asset prices move sharply and portfolios can drift away from their intended mix. Volatility can create meaningful gaps between your target weights and the actual holdings, leaving you either unintentionally overexposed to risk or too conservative at precisely the wrong time. Revisiting your rebalancing plan in these moments helps ensure your portfolio stays aligned with your long‑term strategy rather than the market’s latest swings.

The goal isn’t to react to every bump in the market, but to use volatility as an opportunity to realign your portfolio in a disciplined, tax‑aware way. Systematic rebalancing helps you trim what has become too large, add to areas that have lagged, and maintain the risk profile you intended. The agenda is clear: a consistent rebalancing process keeps your strategy on course and reduces the odds that short‑term turbulence will push you into decisions that undermine long‑term results.

Tax-loss Harvesting

Here’s another area worth revisiting when markets turn volatile. Sharp declines can create potential opportunities to realize losses in a controlled, intentional way—allowing you to offset current or future capital gains, reduce your tax bill, and reinvest the proceeds in similar exposures without disrupting your overall strategy. Periods of stress often widen the gap between winners and losers, making it easier to identify positions that can be harvested without compromising long‑term goals.

The value of this approach is straightforward: thoughtful tax‑loss harvesting turns market turbulence into a tangible benefit, improving after‑tax returns while keeping your portfolio aligned with its intended risk profile.

Use Tax Losses to Move Into Lower‑Expense ETFs

Periods of market stress often create opportunities to harvest tax losses, and those same moments may present opportunities for upgrading the underlying building blocks of your portfolio. When you sell a fund to realize a loss, you may be able to reinvest the proceeds in a similar—but not “substantially identical”—ETF with a lower expense ratio. This keeps your market exposure intact while reducing the ongoing cost of holding the position. (It is best to consult current IRS guidance and a tax adviser regarding wash sale rules and other tax considerations associated with tax-loss harvesting strategies.)

The benefit of this approach may include lowering expenses, which is one of the few levers investors fully control—even small reductions compound meaningfully over time. Using tax‑loss harvesting as a chance to swap into lower‑cost ETFs can turn a short‑term setback into a long‑term advantage, and may help improve tax efficiency and reduce portfolio costs while maintaining similar market exposure consistent with an investor’s overall investment strategy and risk tolerance.

Stay disciplined with contributions and withdrawals

Periods of market stress are an ideal time to revisit how consistently you’re adding to (or drawing from) your portfolio. For savers, maintaining regular contributions—especially through automated deposits—turns volatility into a potential advantage by buying more shares when prices are lower. For retirees or anyone taking withdrawals, stress periods are a cue to review your spending rate and ensure you’re not pulling too much from a declining market.

Steady contribution and withdrawal habits help smooth the impact of volatility, reduce the temptation to time the market, and keep your long‑term plan intact when conditions are most unsettled.

None of these steps are meant to replace personalized financial advice tailored to your specific goals, time horizon, or risk tolerance. Market volatility can be a useful reminder to revisit your broader financial plan. For many investors, working with a qualified financial adviser may be the best way to determine whether these strategies make sense within the context of their individual circumstances.