Fed Rate Cuts on Hold, But Liquidity Conditions Still Look Supportive For Stocks

By James Picerno | The Milwaukee Company

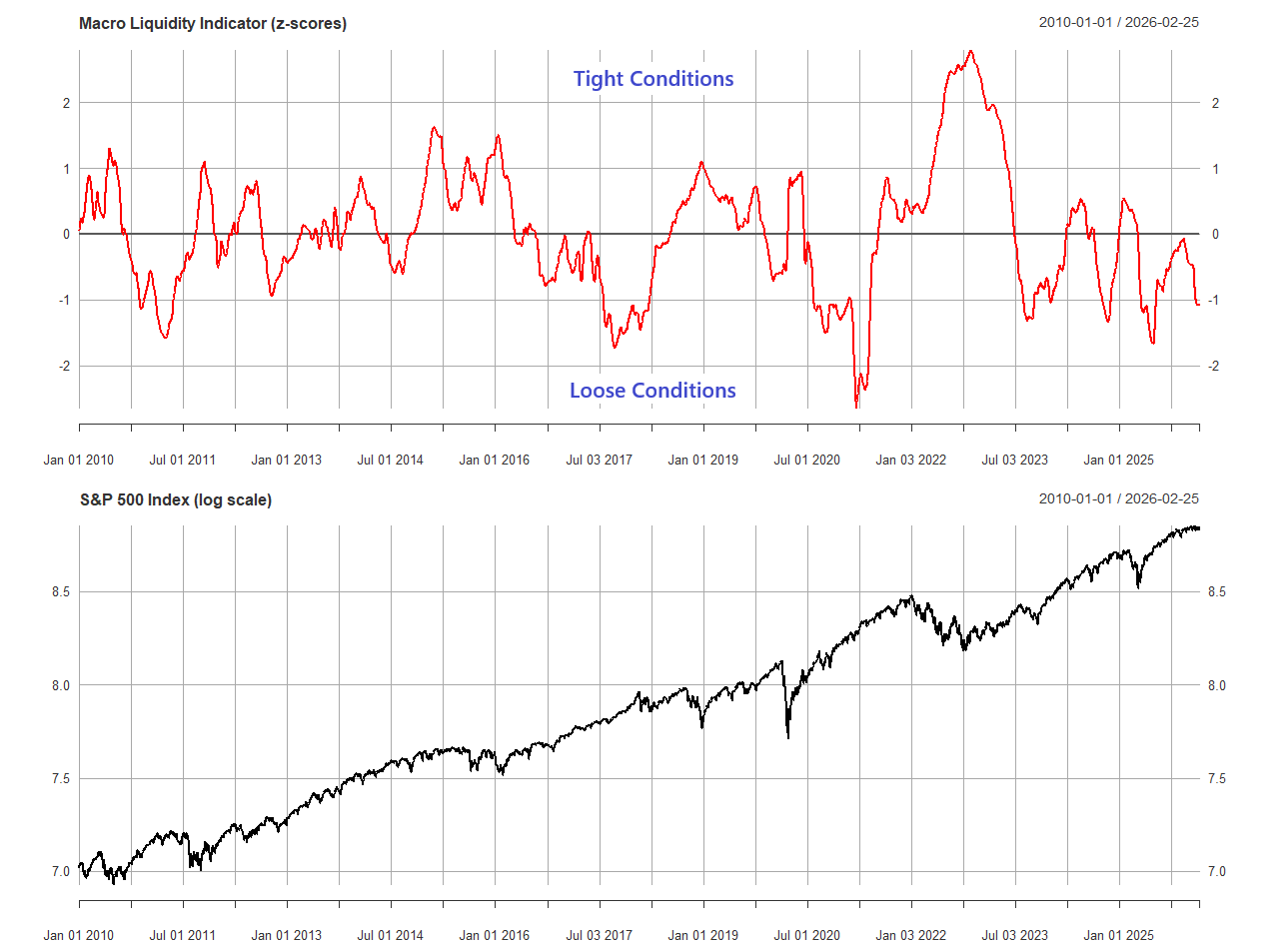

Macro liquidity conditions remain favorable for stocks

The Fed is expected to keep rates steady for the near term

The odds appear low that macro conditions will soon turn tight

The Fed is expected to hold steady on rates for the next two policy meetings, but liquidity conditions still look favorable for the stock market, according to analysis by TMC Research.

There are many factors that drive equity prices, and the overall degree of liquidity flowing through the economy is usually on the short list of relevant variables. In line with recent history, our broad measure of liquidity continues to skew loose, which is to say a tailwind remains intact. Whether that alone is enough to keep equity prices rising is unclear, but it helps tilt the odds in the bulls’ favor, if only on the margins.

By contrast, relatively tight macro conditions on the liquidity front are usually a headwind. Ahead of the 2022 correction, for example, conditions tightened, which was likely a factor in the S&P 500 Index’s slide that year.

When macro liquidity flips to tight conditions, as it inevitably does in every cycle, a new challenge for the bull run will emerge. Tighter conditions don’t always translate into immediate market stress, in part because other forces can temporarily counteract the drag. But to the extent that liquidity conditions move from one extreme to the other, that can be a sign of trouble ahead.

For now, a major shift from loose to tight conditions doesn’t appear imminent, echoing conditions in our previous update for this indicator in September. The implication: whatever the trigger for the next stock market correction, the catalyst isn’t likely to arise from restrictive liquidity conditions, at least for the near term.

The Macro Liquidity Indicator in the chart above uses five inputs to assess conditions: the US dollar, the high-yield bond spread, commercial bank loans and leases, consumer inflation, and the US 10-year Treasury yield. There are many variations on measuring this risk factor, but the mix shown above is a reasonable first approximation.