Softer Inflation and Expectations for Stronger Q1 Economic Growth Push the Fed Toward a Pause

By James Picerno | The Milwaukee Company

Nowcasts for Q1 economic activity point to a rebound after Q4’s downshift

CPI inflation cooled in January, moving closer to the Fed’s 2% target

Fed officials signal patience, keeping rate‑cut expectations muted

The slower-than-expected growth rate for the US economy in Friday’s fourth-quarter GDP report suggests the Federal Reserve may cut rates sooner than expected. But Fed funds futures continue to price in a pause for the next two policy meetings. Support for this outlook comes from expectations for a rebound in economic growth for this year’s first quarter, along with a slightly softer inflation trend for January.

Nowcasts from various sources point to a pickup in Q1. The Atlanta Fed’s GDPNow model, for example, is currently estimating a 3.1% annualized increase for GDP (as of Feb. 20) for the first quarter, more than double the 1.4% rise reported for Q4. Part of the reason for the weaker advance in last year’s final quarter was the temporary effects of the government shutdown.

If growth is firming in Q1, the rationale for rate cuts is less compelling, all else equal. Perhaps that’s why Fed funds futures are still pricing in high odds for no change in the central bank’s target rate for the next two policy meetings in March and April. By June, the odds for a rate cut shift to a coin flip.

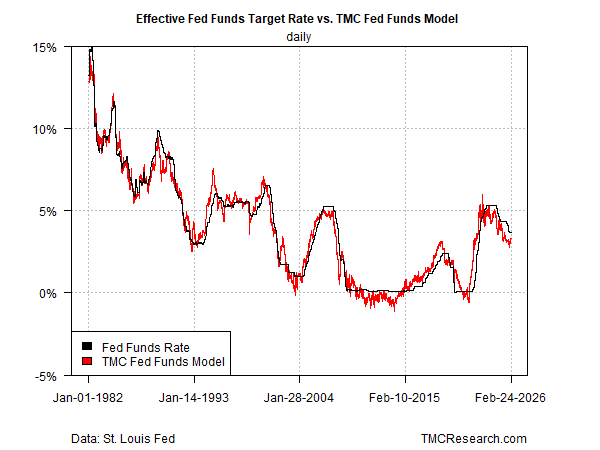

Policy Tightness Eases as Inflation Cools

TMC Research’s Fed funds model continues to show policy as modestly tight, but far less so than in recent history. The current spread between our model and the effective Fed funds rate has fallen to roughly 30 basis points, or half as much as a month ago and the lowest in nearly a year. The Fed’s hawkish stance, in other words, has faded, primarily due to softer inflation reported for January.

The consumer price index (CPI) rose 2.4% in January vs. the year-ago level, the lowest since May. The current trend for CPI puts it close to the Fed’s 2% target rate.

The combination of expected firming in economic activity and the latest downshift in CPI inflation lays the foundation for anticipating steady Fed policy for the near term.

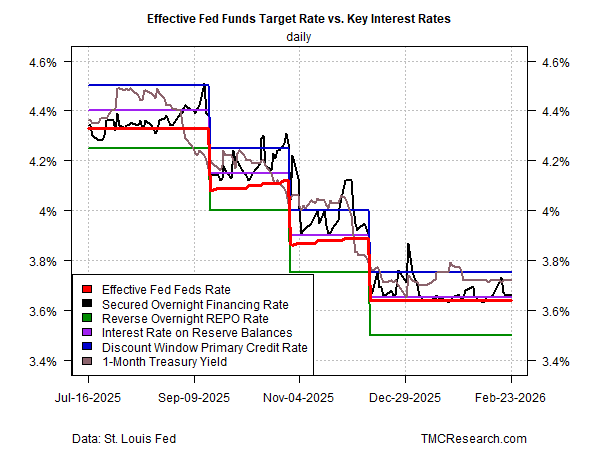

A market-based profile also points to a stable Fed funds rate for the near term, according to several key interest rates that are sensitive to policy-bias expectations. Note the 1-month Treasury yield, which is holding in the upper half of the channel (relative to the effective Fed funds rate), implying that the market isn’t pricing in a change of policy to the downside.

Fed Officials Urge Patience

Although inflation has eased lately and may be set to move closer to the Fed’s target, some Fed members remain cautious on further cuts. Chicago Federal Reserve President Austan Goolsbee, a voting member of the Federal Open Market Committee this year, said on Tuesday that it was still premature to start a new round of cuts until there’s more evidence that the recent downshift in inflation will hold.

“People express that prices are one of their most pressing concerns. Let’s pay attention. Before we cut rates more to stimulate the economy, let’s be sure inflation is heading back to 2%,” he remarked at a conference yesterday.

In a sign of the times, Federal Reserve Governor Christopher Waller, who recently dissented from the majority and recommended cutting interest rates, has turned cautious lately. In a speech this week he said that, while the January payrolls report surprised with a stronger-than-expected increase in hiring, “One month of good news does not constitute a trend, but a year does, and the year of 2025 was an extraordinarily weak one for job creation.”

Waller is still leaning toward cutting, but he’s become open to keeping policy unchanged. That’s a subtle shift to a casual observer, but it may reflect how the broader Fed policy bias has changed lately. As he explained:

“Before the next meeting of the FOMC on March 17 and 18, we will get employment and inflation data for February, as well as more data on job openings and retail sales. If these data support the idea of an improvement in the labor market in January that continued in February, along with additional progress toward 2 percent inflation, that could result in my outlook turning a bit more positive and my view of appropriate monetary policy may tilt toward a pause at our upcoming meeting.”

If growth is firming and inflation easing, the path of least resistance appears to tilting toward patience—and the Fed seems ready to take it.