Will Tariffs Convince The Federal Reserve To Cut Interest Rates?

By James Picerno | The Milwaukee Company

Expectations are building for a Fed interest-rate cut.

The US 2-year Treasury is trading down again today, trading at a six-month low.

Economic data, starting with Friday’s employment report for March, will significantly influence the timing and magnitude of potential rate cuts.

Expectations are building for a rate cut by the Federal Reserve as the US prepares to impose 20% tariffs on nearly all imports starting tomorrow, Apr. 2. The change in trade policy is expected to increase inflation and reduce economic growth in the near term. The Fed has been struggling with how to respond, preferring to remain in a “wait-and-see” mode. But the bond market and Fed funds futures in recent days are starting to price in higher odds for rate cuts. Markets, in other words, are anticipating that the central bank will increasingly focus on the risk of slower growth (and perhaps recession) over higher inflation as the priority for monetary policy.

Fed funds futures this afternoon still indicate a high probability for no change in rates at the next FOMC meeting on May 7. But the outlook has shifted in recent days and the market is now estimating a roughly 78% probability for a rate cut at the June meeting, based on data published by CME Group.

The 2-year Treasury yield, which is widely followed as a proxy for policy expectations, continued trading lower today, slipping to 3.85% this afternoon – a six-month low. The decline suggests that the bond market is pricing in higher odds for a new round of policy easing in the near term.

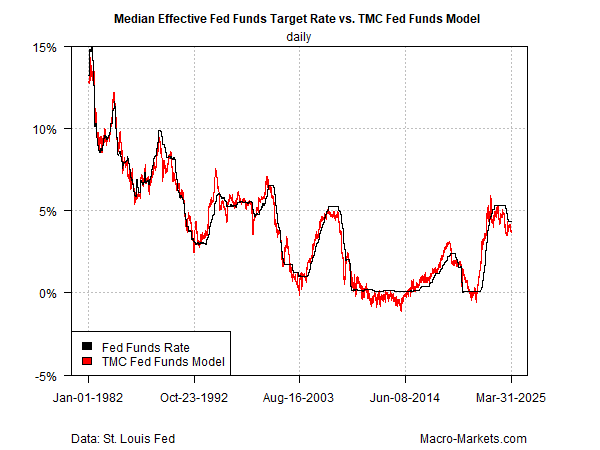

TMC Research’s Fed model still indicates that monetary policy is moderately tight, which implies that the central bank has room to cut rates. The model’s current estimate of the “optimal” median rate is roughly 56 basis points below the actual median Fed funds rate, as of Mar. 31. That suggests a ½-point cut would shift policy to a neutral stance. Using this estimate as a guide points to an even bigger cut if the Fed repositions policy and takes an aggressive stand to support economic growth via lower rates.

At the moment, markets are pricing in a cut no sooner than June, with expectations leaning heavily toward a ¼-point cut to a 4.0%-to-4.25% range for the first round of easing, according to Fed funds futures. The crucial variable is how the economy and markets react to higher tariffs in the days and weeks ahead – reactions that will probably influence the timing and magnitude of the Fed’s policy decisions.

The next major economic report that could shift expectations: this Friday’s employment report (Apr. 4). The consensus forecast sees a moderately softer pace of hiring. If the actual data is significantly weaker than forecast, markets will likely revise rate-cut expectations in anticipation of easing policy sooner and perhaps deeper than currently estimated.

Read a pdf version of this article: