Will Mild Trimmed-Mean Inflation Delay Fed Rate Hikes?

By James Picerno | The Milwaukee Company

Trimmed‑mean inflation is substantially cooler than standard price measures

Markets are expecting rate hikes despite calmer trimmed‑mean readings

The Fed faces mixed signals at a pivotal policy moment

The latest inflation numbers aren’t especially encouraging for Fed Chair Kevin Warsh, who emphasized at his first policy meeting two weeks ago that the central bank “will deliver price stability.” But the new Fed chief is a fan of so‑called trimmed‑mean inflation, which currently reflects a substantially lower, steadier pricing trend. The question is whether this alternative model for tracking inflation will persuade the Fed to delay—if not forgo—rate hikes.

Warsh appears committed to using alternative price measures and seems intent on giving them a larger role in Fed policy decisions. During his Senate confirmation hearing in April, he argued that “the data that’s being used to judge inflation is quite imperfect.” As a solution, he urged the Fed to focus on “trimmed averages” for a clearer, more reliable measure of the “underlying, generalized change in prices in the economy.”

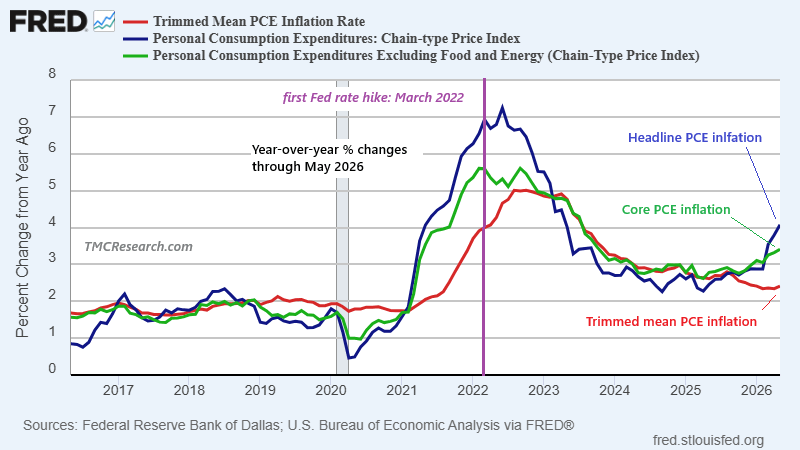

That’s a provocative idea at a time when a leading proxy for the trimmed‑mean inflation rate is running at a pace substantially below the Fed’s standard inflation metrics. Using the latest numbers for May, the one‑year change in the Dallas Fed’s trimmed‑mean core (excluding food and energy) PCE price index is a comparatively tame 2.4%, only modestly above the Fed’s 2% inflation target. By this standard, the Fed can afford to be patient about a future policy pivot.

By contrast, the standard core PCE inflation trend that the Fed has long focused on is considerably hotter, posting a 3.4% increase over the year‑ago level—the highest since late 2023 (green line in chart). Headline PCE, which includes food and energy, is even higher, topping a 4% annual pace through May for the first time in three years (black line).

The trimmed‑mean methodology drops the largest and smallest price changes and calculates inflation from the weighted average of the remaining, more representative items. Supporters say this approach can be superior because it filters out the most volatile monthly price swings, providing a steadier, more accurate real‑time signal of underlying inflation trends and future inflation than traditional core measures, which simply exclude fixed categories like food and energy.

But what sounds encouraging in theory doesn’t always translate into an advantage in practice. As the chart above shows, trimmed‑mean PCE inflation was slow to react to the 2021–2022 inflation surge compared with the standard PCE measures.

When the Fed began raising rates in March 2022, critics charged that policymakers had waited too long, allowing pricing pressure to run higher and last longer than if a hawkish pivot had come earlier. The slow change in trimmed‑mean inflation suggests that relying too heavily on this measure would have left the Fed even further behind in responding to the pandemic‑related inflation spike.

Whatever the flaws or advantages of trimmed‑mean inflation, it isn’t expected to play an outsized role in Fed decisions any time soon. That, at least, is the implied forecast from the Fed funds futures market, which is pricing in rising odds of rate hikes in the near term. For example, the roughly 30% estimated probability of tighter policy at the next FOMC meeting on July 29 climbs to 62% for September. The priced outlook for another hike later in the year has also been edging higher.

Even so, the path ahead for the Fed remains fluid, buffeted by shifting assessments of geopolitical risk in the Middle East and its impact on energy exports—an input that remains central to inflation expectations. The sharp drop in crude oil prices in recent weeks is, for now, holding, a decline that will soon translate into lower headline inflation pressure. The concern is that standard measures of core inflation, regardless of near‑term energy trends, may already be set on a path to rise further and widen the gap over the Fed’s 2% target.

Meanwhile, it’s unclear how much influence the trimmed‑mean data will exert on the Federal Open Market Committee and its upcoming decisions on interest rates.

One thing is certain: Warsh’s preferred inflation gauge may be trimmed—but the debate over its power to shape Fed policy is anything but.