Will Inflation Uncertainty Remain A Speed Bump For Rate Cuts In 2026?

By James Picerno | The Milwaukee Company

Markets anticipate a January pause for rate cuts, but lean toward a March cut as Treasury yields stay calm

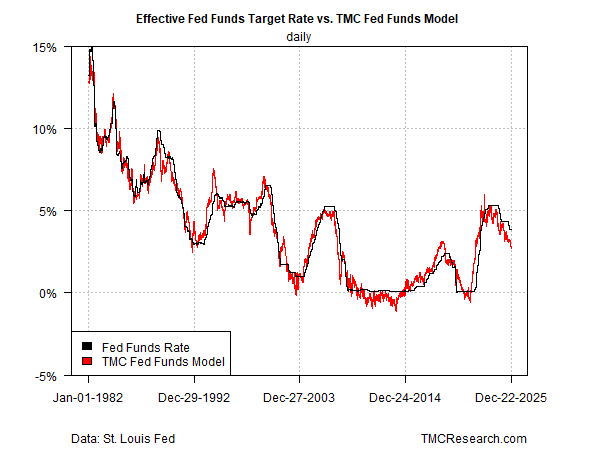

TMC Research’s Fed funds model continues to estimate monetary policy is relatively tight, leaving space for more easing

Inflation‑data uncertainty surrounding November’s CPI report tempers confidence on the outlook for 2026 rate cuts

Expectations are mixed on the outlook for more rate cuts by the Federal Reserve in 2026. After the central bank trimmed its target rate three times in 2025 (including this month’s cut), markets are taking a more nuanced view of what lies ahead next year for additional policy easing.

Fed funds futures capture the mood on Wall Street for gauging the Fed’s next moves. For the January policy meeting, the market appears to be pricing in moderately high odds that the central bank will leave rates steady. The outlook is more favorable for resuming cuts at the subsequent meeting in March.

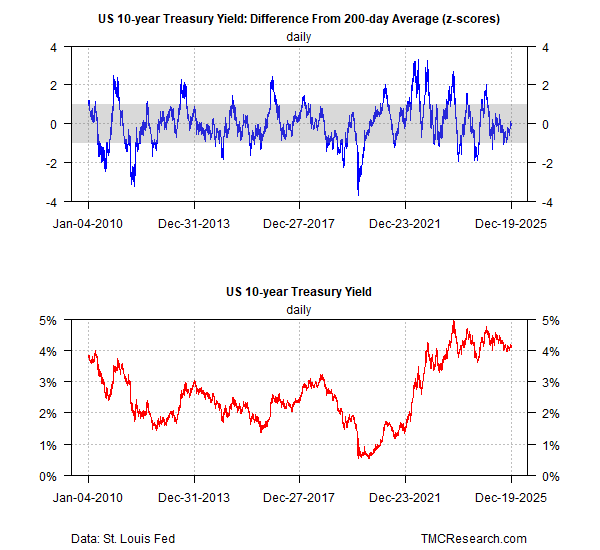

Meanwhile, the status quo continues in the bond market, based on the 10-year Treasury yield, which continues to trade in a range. In the final days of the year, the benchmark rate is a middling level for the year. The relatively subdued profile suggests that bond traders aren’t particularly anxious about inflation risk and are downplaying the odds for a hawkish policy pivot at the Fed.

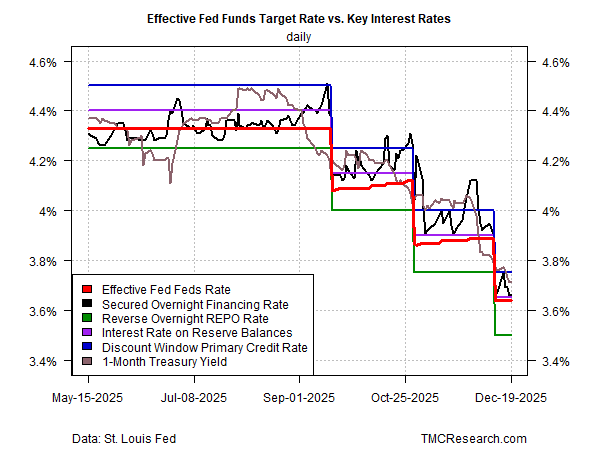

Several key yields that reflect expectations for the near-term path for the Fed funds rate continue to align with the dovish policy outlook. Two weeks ago, when the central bank announced another rate cut, Fed officials forecast that the target rate would ease further in 2026, based on the median projection. Market data since then suggest that investor sentiment is still satisfied with the Fed’s overall outlook.

TMC Research’s Fed funds model, which estimates the optimal target rate, given a set of economic and financial factors, continues to indicate that policy is moderately tight. The implication: there’s still room for cutting rates without setting policy overly loose for given macro conditions.

A key factor that could alter neutral/dovish expectations for monetary policy in the new year: incoming inflation data. The release of last week’s delayed report on consumer prices for November posted softer-than-expected numbers, providing support for projecting additional rate cuts next year. But questions about the reliability of the latest update highlights uncertainty about inflation’s path in 2026. In turn, the odds for more rate cuts may be lower than currently estimated.

At issue is the reliability of the consumer price index’s data-collection process, which was interrupted due to the government shutdown. To compensate for the disruption, a questionable methodology was used to fill in the missing numbers, which (by some accounts) resulted in an excessive downside bias for November’s inflation estimate.

On that basis, inflation may still be trending up, rather than holding in the 2.5%-3.0% range, per November’s inflation report. Deciding if that suspicion is warranted, or not, will play a significant role in refining the outlook for Fed policy in the months ahead.

No less important is how upcoming employment data compares. The latest payrolls report from the government show that hiring has slowed while the jobless rate has ticked up, rising to 4.6%, the highest in four years. Those trends are factors that persuade the Fed that rate cuts are needed to support the economy.

Higher inflation in the next round of updates could derail the focus on labor-market weakness, but for now, using the 10-year yield as a proxy, suggests that investors remain cautiously optimistic that inflation will remain steady, if not edge lower. Until or if the incoming data suggests otherwise, it’s too soon to rule out the case for more rate cuts in 2026.