Widening Spread Between Fed Funds Rate and 30-Year Treasury Yield Signals Rising Policy Risk

By James Picerno | The Milwaukee Company

The Fed continues to cut rates despite inflation stuck above its inflation target

The bond market, so far, mostly accepts the Fed’s policy decisions, but…

The rising gap in the 30-year Treasury yield over the Fed’s target rate highlights the market’s growing policy doubts

The Federal Reserve has been cutting interest rates for more than a year, including last week’s cut. Although the central bank has less influence over the long end of the yield curve (dramatically less, at times), maturities overall tend to move in line with the Fed’s dovish policy pivots, albeit slowly and unevenly. Is this time different?

At issue is the lingering concern that inflation remains a risk factor for the Fed. Consider the core reading of the price index for Personal Consumption Expenditures, the central’s preferred measure of inflation. Since 2021, core PCE has been running at an annual pace that’s well above the Fed’s 2% inflation target. In the most recent update, core PCE rose 2.8% for the year through September.

The Fed began cutting rates more than a year ago. Core PCE inflation, after sliding from 2022 through mid-2024, has been stuck in a 2.6%-3.0% range. Sticky inflation over the last year and a half has raised concerns that cutting interest is premature.

The Fed counters that the recent weakness in the labor market is a more pressing concern, thus the decision to ease monetary policy. Nonetheless, economists continue to debate the wisdom of rate cuts.

A key question is whether the bond market will endorse rate cuts at a time when inflation risk is still a concern? The answer, so far: bond investors have accepted the Fed’s focus on labor market weakness as the correct policy priority. How do we know? Treasury yields have fallen for much of the year, which suggests that the bond market is still comfortable with focusing on labor-market weakness over inflation risk.

But there are signs that one corner of the Treasury market is becoming anxious. With the possibility that the Fed could cut rates further next year, the potential is brewing for a bond-market revolt.

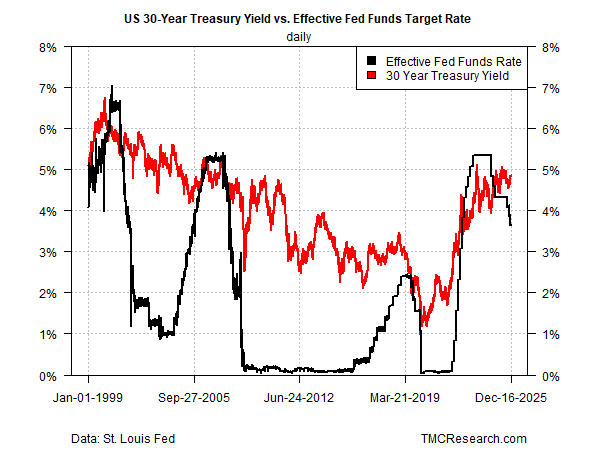

A useful way to track this dimension of risk is by comparing the 30-year yield – the most inflation-sensitive maturity – relative to the effective Fed funds rate. The central bank controls the latter, but has limited, and at times nil influence over the latter. As a result, the dance between the two rates speaks volumes on how the market perceives Fed policy through an inflation-risk lens.

Consider the two have evolved over the past quarter century. During the three-rate cutting cycles prior to the current one, the 30-year yield generally eased in due course. That’s been a sign that the market has a relatively high degree of confidence that the dovish change in Fed policy was an appropriate course of action.

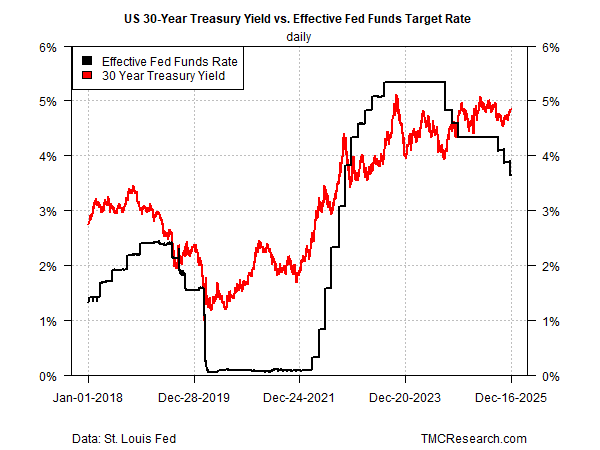

Notice, however, that the 30-year yield has flipped the historical script lately. For a clearer look, let’s zoom in on recent history in the second chart below, which highlights a growing gap between the long yield and the Effective Fed funds rate.

It’s unclear if the 30-year yield will continue to rise, or if the Fed will continue to cut rates. But this much is clear: if the gap becomes wider in the weeks and months ahead, the divergence will signal that the market has serious doubts about Fed policy. In turn, those doubts could reverberate across asset classes and the economy.

For now, the wider gap could be noise, a delayed reaction among bond traders to follow the Fed, or a temporary bout of market turbulence unrelated to pushback regarding the monetary policy decisions. But at some point, if these two rates continue to move in opposite directions, it will become increasingly difficult for the Fed, or investors, to ignore the spread.