Warsh Nomination To Fed Introduces New Uncertainty For 2026 Policy Outlook

By James Picerno | The Milwaukee Company

Former Fed Governor Kevin Warsh is set to take the helm at the Fed in May

The leadership transition may complicate the outlook for policy decisions

The 30-year Treasury yield suggests the bond market is still wary about inflation risk

Federal Reserve Chair Jerome is officially a lame duck after President Trump last week selected Kevin Warsh to lead the central bank starting in just over three months. Between now and then, an unusual transition period awaits, which introduces an additional layer of uncertainty for monetary policy in the months ahead.

The main source of ambiguity for markets is deciding if Warsh will be hawkish, dovish, or something in between for policy decisions, when he takes over from Chair Jerome Powell, whose terms ends on May 15.

A number of news reports have described Warsh as a long-time monetary hawk, based on his speeches and commentary over the years. That’s a reasonable view because Warsh, a former member of the Fed’s Board of Governors, hasn’t been shy with criticizing some of the central bank’s dovish decisions regarding policy stimulus over the years. In 2011, he resigned from the Fed and blasted the expansion of the Fed’s balance sheet, calling it “bloated” and a “relic of crisis-era thinking.”

The question is how Warsh, if confirmed by the Senate, will manage policy when he arrives at the Fed in May? By some accounts, he’s become more dovish in recent years, a view that some Fed watchers claim will continue, and possibly deepen in the current political climate. President Trump, since returning to the White House, has made it clear that he wants lower interest rates and so the political factor may be part of the calculus for assessing the outlook for central bank decisions.

Perhaps that’s why the Fed funds futures market is expecting no change in the central bank’s target rate for the next two policy meetings (March and April), followed by modestly favorable odds for a rate cut in June, when Warsh is expected to oversee his first decision on interest rates.

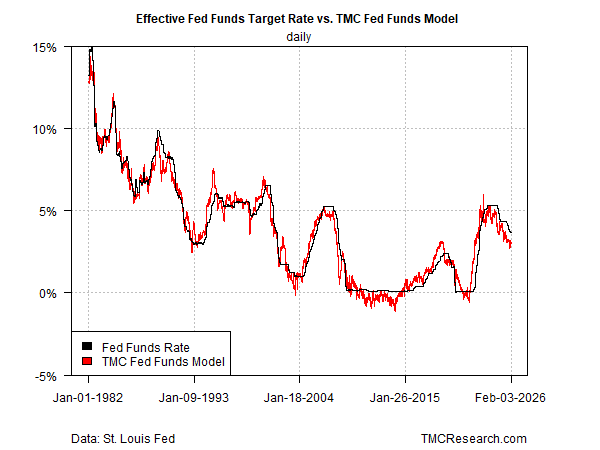

Tilting Less Hawkish

TMC Research’s Fed Funds Model shows that the policy bias has become less hawkish recently. Our current estimate of the optimal rate given current conditions is roughly 3.06%, or nearly 60 basis points below the current 3.64% median Effective Fed funds rate (based on monthly estimates as of January). The implication: Policy is still moderately tighter than current conditions suggest, which leaves room for more rate cuts, at least in theory.

The current difference between our model and Fed funds is close to the lowest spread in nearly a year and well below the previous peak of 126 basis of last August, when Fed funds were substantially higher in absolute and relative terms (vis-à-vis our model estimate). In other words, policy tightness continues to ease, moving closer to the neutral zone after three rate cuts in 2025.

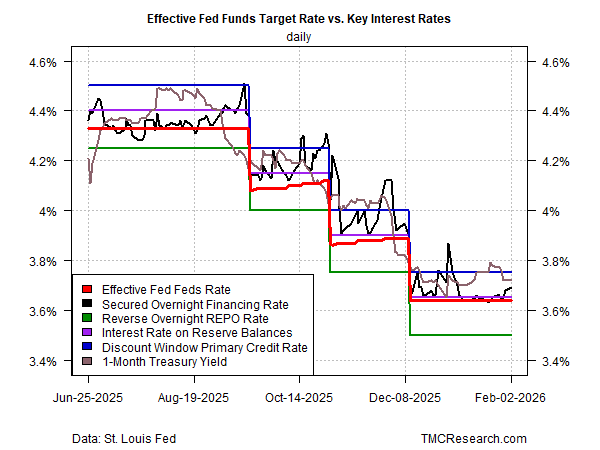

Channel Down

Another measure of how the policy bias is evolving from a market perspective can be seen from tracking several key interest rates that are sensitive to expectations for the Fed funds target rate. The current profile of the so-called policy channel indicates a relatively neutral bias at the moment. Ahead of previous rate cuts in 2025, the 1-month Treasury yield fell into the lower half of the channel — a repeat performance would suggest that the market is expecting another round of easing in the near future.

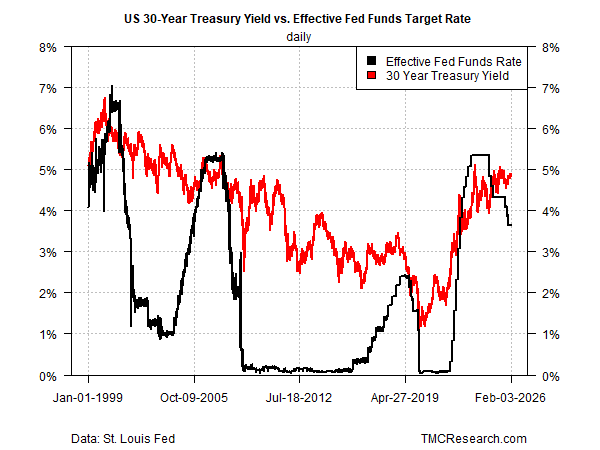

Is It Different This Time?

Amid concerns in some corners that the incoming Fed Chair will err on the side of dovish policy before inflation risk has fully subsided, the 30-year Treasury yield deserves close attention in the months to come. As we discussed in mid-December, the long yield (the most inflation-sensitive maturity) tends to fall in line with Fed rate cuts in due course – a history that’s not playing out this time, at least so far.

The divergence from history could be a warning flag that the bond market is becoming anxious about the policy outlook vis-a-vis inflation. Note that in the wake of the latest rate cut in December, the 30-year yield edged higher, and has been trading above 4.80% for much of the past two months.

If the 30-year yield holds steady or moves higher, at a time when market expectations for Fed policy are looking for a pause followed by a rate cut in June, the mismatch may signal the bond market’s growing anxiety about inflation risk.

Much will depend on how incoming economic data stacks up for assessing how the Fed should act. No less a critical factor is how the new Fed chair navigates Washington’s tricky terrain. Warsh’s biggest challenge is convincing markets that he will act independently of White House influence. The bond market will be watching.