US Growth Is Slowing, But Recession Risk Still Appears Low

By James Picerno | The Milwaukee Company | jpicerno@themilwaukeecompany.com

Several economic indicators that are updated frequently suggest the start of a US recession still doesn’t look like a high risk in the immediate future.

The relatively upbeat profile is based on hard data via three sources: Dallas Fed’s Weekly Economic Index, Philadelphia Fed’s ADS Index, and the Labor Dept’s weekly jobless claims report.

Recent surveys paint a more worrisome outlook, but until the hard data agrees it’s reasonable to view recession forecasts cautiously.

Using several recent surveys as a guide reflects a view that US recession risk is rising, and could start soon. The expectations index for the Conference Board’s consumer survey for March, for example, fell to the lowest level in 12 years. A key driver of the worrisome outlook is the assumption that tariffs will slow the economy, perhaps leading to economic contraction. But several key data sources that reflect actual economic activity suggest a stronger profile. Until the hard data shows clear and persistent deterioration, recession forecasts should be viewed with a degree of skepticism.

To be fair, the current macro climate is certainly fluid, which implies that significant changes for the economy can arrive quickly and unexpectedly, depending on how US tariff policy unfolds and foreign countries react. All the more reason that relatively objective measures of real-time (or close to real-time) activity are essential to minimize emotional reactions to headlines. With that goal in mind, three indicators that are updated weekly are useful proxies for evaluating economic conditions based on published numbers rather than guesstimates about what could happen.

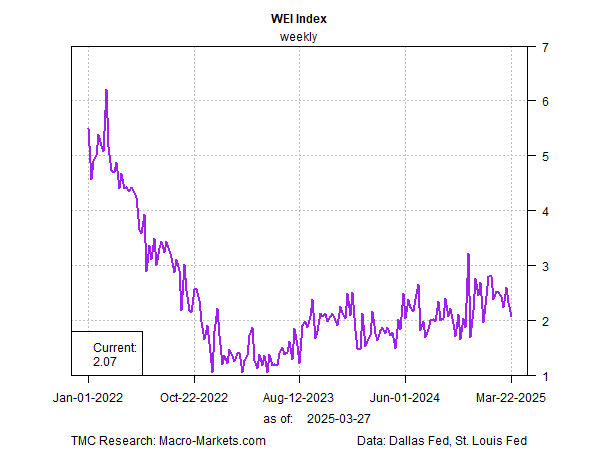

Let’s start with the Dallas Fed’s Weekly Economic Index (WEI), which tracks 10 indicators that cover the consumer sector, the labor market and production activity. Today’s update shows WEI continued to ease, although the 2.1% reading as of Mar. 27 (which can be used as a proxy for year-over-year economic change) aligns with moderate economic growth. For comparison, US GDP rose 2.5% for the year through 2024’s fourth quarter.

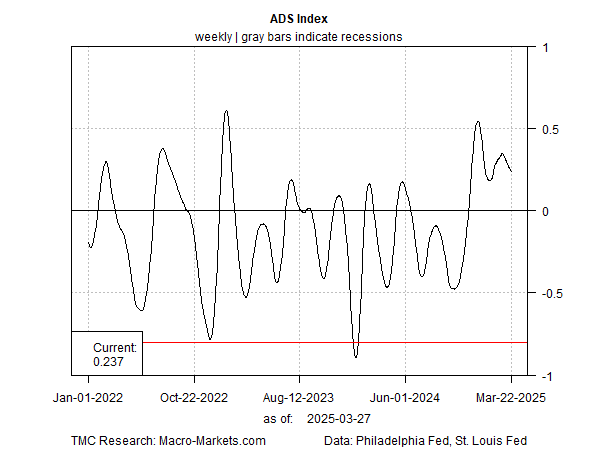

The Philly Fed’s ADS Index, which tracks several indicators, also shows economic activity has been slowing recently, but the latest reading through Mar. 22 continues to reflect a moderately strong growth bias. ADS edged down to 0.24, the lowest in nearly two months. Note, however, that the current reading is still above zero, which suggests that economic activity is above average vs. the historical record. TMC Research estimates that an ADS value of -0.80 or lower equates with recession (indicated by the red line in ADS chart). For the moment, that tipping point is nowhere on the near-term horizon.

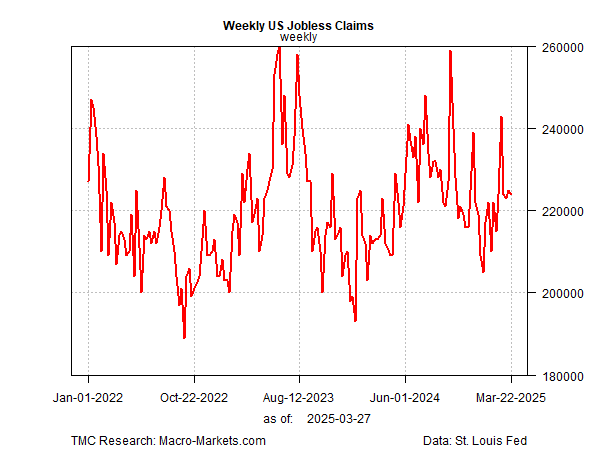

Weekly jobless claims offer another valuable indicator to watch for assessing economic conditions in real time using hard data. Claims for new unemployment benefits are a leading indicator for the labor market and tend to rise going into and during recessions, which makes this time series a useful early-warning indicator. But for the moment, claims remain subdued, holding at a middling range that’s close to the lowest level in decades, as of Mar. 22.

None of this dismisses the risk of an economic slowdown, or worse. As WEI and ADS show, economic activity has downshifted recently. This could be a prelude to recession, but no one’s sure. What is clear is that the indicators discussed suggest that a recession isn’t imminent. If that changes, we’ll likely see warning signs that a downturn is approaching in updates to the charts above.

Read a pdf version of this article: