US Debt Resolution Will Require a Delicate Mix of Policy Levers

By James Picerno | The Milwaukee Company

Rising US debt is a macro risk that’s becoming harder to ignore

Monetization of debt, fiscal austerity, and economic growth are three likely paths for solving the budget deficit

TMC Research expects a flexible mix of strategies will unfold in the months and years ahead to restrain the rising tide of red ink

It’s no secret that US government debt is a growing burden, according to Congressional Budget Office data — a macro risk factor that’s closely monitored at TMC Research. The mystery is how and when this mounting liability will be resolved, and what it will mean for financial markets and the economy.

One way or another, resolution is coming, by design or otherwise. As Newton famously observed: “An object in motion tends to remain in motion along a straight line unless acted upon by an outside force.”

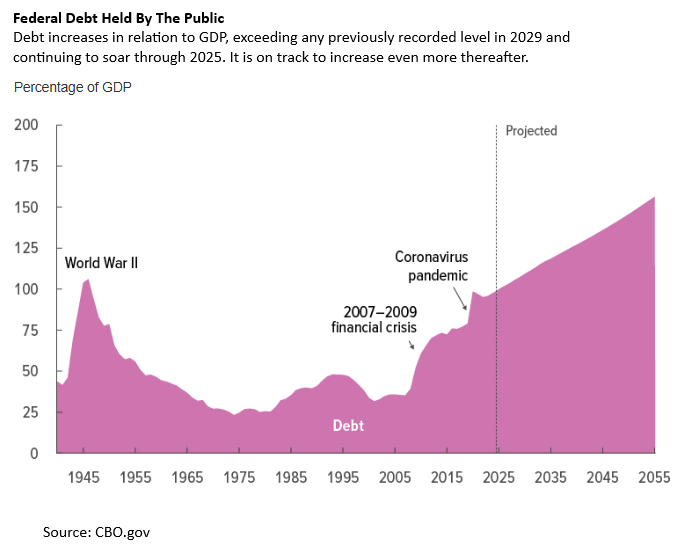

The straight line for the debt outlook was drawn earlier this year, when in March the CBO projected that “federal debt held by the public, measured as a percentage of gross domestic product (GDP), increases in every year of the 2025–2055 period.” This burden is expected to climb to an unprecedented 156% of GDP by 2055, based on current assumptions about spending and revenue when this long-term budget outlook was published.

The uncertainty is what “outside source” will address curtail the red ink? No one knows, but one point of clarity is that there are several known resolution paths. The risks associated with each vary, as do the probabilities that one path or another will prevail, and so it’s useful to engage in some preliminary scenario planning, if only to manage expectations and think about the implications for the economy and financial markets.

Default

Let’s start with least-likely path: default. This is the worst-case scenario, and one that almost certainly won’t happen because of the US government’s economic and financial strength. That’s a good thing because the default path would be the most disruptive for markets and the economy.

For all its fiscal challenges, America won’t be forced into default, which tends to be the case when a government can’t or refuses to repay its debt. This is a risk that applies primarily to certain small and/or emerging markets that run into acute fiscal troubles – think Argentina’s string of financial crises over the years, for example.

The US, by contrast, still has wide latitude to run afoul of fiscal red lines that would threaten other countries. Why? Overseeing the world’s largest economy is a pivotal factor, along with the unique advantages of issuing the world’s reserve currency. A strong global appetite for US Treasuries is also a crucial byproduct. Although these advantages aren’t written in stone, and are showing some signs of degrading lately, for the foreseeable future it’s a reasonable bet that American exceptionalism will continue.

Monetization of US Treasury debt

This option falls into the category of “likely,” in part because it’s a lever the government has pulled several times already. A recent example: 2008, when the Federal Reserve purchased Treasuries during the financial crisis. The central bank also bought bonds in the pandemic to keep interest rates low. In both episodes, the monetization was labeled “quantitative easing,” but the underlying mechanics arguably fall into the monetization category.

The logic is straightforward: Fed bond purchases reduce the burden of financing the government’s budget deficit. The mechanism is lowering interest rates, which would be higher in the absence of Fed intervention, all else equal.

The downside is that monetization can lift inflation, depending on how long and extensive the policy. Although economists are still debating the reasons for the inflation surge in 2021-2022, the Cato Institute advises that fiscal dominance (of which debt monetization is one variety) “has a track record of triggering severe inflation...”

Austerity

Another option for addressing a government budget deficit is cutting public spending and/or raising taxes. Research by economist Alberto Alesina — Austerity: When It Works and When It Doesn’t — finds that reducing deficits by way of tax increases tends to be substantially more painful than reducing spending:

Austerity policies based on spending cuts, at least in OECD countries over the past three decades, have had the opposite effects of those predicted by anti-austerity commentators. Their costs, in terms of output losses, have been very low, on average close to zero. Austerity based on tax hikes has often resulted in an increase in the debt over GDP ratio.

The Trump administration’s economic strategy, which includes raising tariffs on imports, could be seen as a component of austerity by raising prices and collecting higher import fees that flow into the government’s coffers.

Economic Growth

The White House argues that tariffs are, in fact, a source of growth because it will incentivize the reshoring of manufacturing. Although the jury’s still out on this point, it’s clear that implementing policies that ramp up economic activity, which in turn lifts tax revenue, is a path to resolving the budget deficit. Ideally, economic growth exceeds the pace of increase in debt.

The Trump administration asserts that this scenario is unfolding amid current White House policies:

Analysis by the Council of Economic Advisers (CEA) confirms that President Trump’s pro-growth economic policies and reining in wasteful spending are key to improving the fiscal outlook. President Trump’s proven economic formula — historic tax relief, rapid deregulation, balanced trade, and reining in wasteful spending — will slash our debt down to just 94% of Gross Domestic Product (GDP)… compared to 117% under Biden’s failed path.

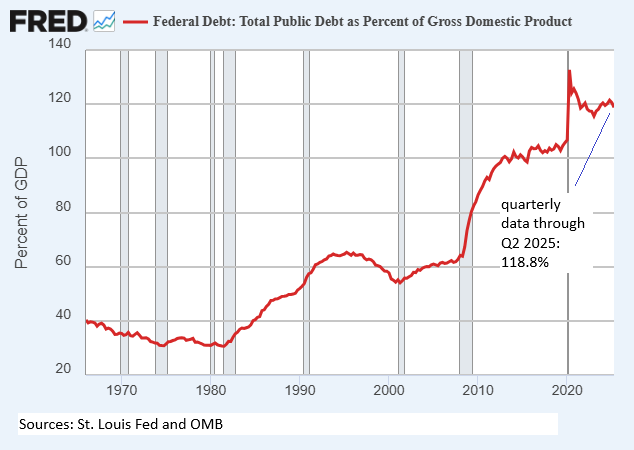

As of this writing, the ratio of total debt to GDP has declined only marginally, from 121% in Q1 2025 to 119%, based on quarterly numbers through Q2 2025, according to data from the Federal Reserve Bank of St. Louis. As a result, the administration still has a long way to go in achieving its professed target.

TMC Research’s View

Which path will prevail to resolve the US budget deficit? No one knows, but given the political and economic risks associated with each of the scenarios outlined above, we expect that some combination of monetization, austerity and economic growth will occur.

Our reasoning is that pursuing any one path in isolation has a potentially higher price tag in terms of a public backlash, political risk for Washington, and potential economic and financial shocks. By contrast, opportunistically threading this needle with a dynamic approach that adjusts each lever on an as-needed basis is arguably the least economically disruptive and politically destabilizing strategy. A mix of the three, in short, appears to be the least-worst of the choices.