US Budget Deficit Pressures Mount as War Spending Surges

By James Picerno | The Milwaukee Company

War costs rise as the deficit deepens

Fiscal gauges flash pandemic‑era stress

No credible deficit plan from Washington yet

The US budget deficit was already on shaky ground before the Iran war, and reports that the Pentagon will seek an additional $200 billion in military funding only complicates the outlook for fiscal risk. Defense Secretary Pete Hegseth has also suggested the request could rise depending on operational needs.

Whatever the extra costs associated with the ongoing conflict, higher spending arrives at a difficult time for the US budget outlook. In February, the Congressional Budget Office (CBO) revised its forecast for government finances and projected that the already hefty deficit will deepen this year to $1.853 trillion. Over the course of the decade ahead, the non-partisan CBO estimates that the deficit-to-GDP ratio will increase to 6.7% from the current 5.7%. If correct, the rise would mark the highest ratio since the pandemic.

The prospect of bigger deficits may be worrisome for several reasons, starting with the fact that the current level of debt is unusual for an economy that’s not in recession. Atypical or not, the fiscal burden poses a potential threat to financial markets by raising inflation and interest rates.

TMC Research routinely analyzes the data in this corner, but fiscal‑risk modeling remains inherently imprecise for estimating the true level of vulnerability and gauging debt markets’ tolerance for government indebtedness. But this much is clear: if the current level of outstanding government obligations increases from current levels — especially in relation to the size of the economy — the implied risk also increases.

“Higher debt adds to the risk of inflationary pressure in both the short- and the long-run, through aggregate demand, inflation expectations, crowding-out of private investment, and worries about fiscal dominance,” advises The Budget Lab at Yale.

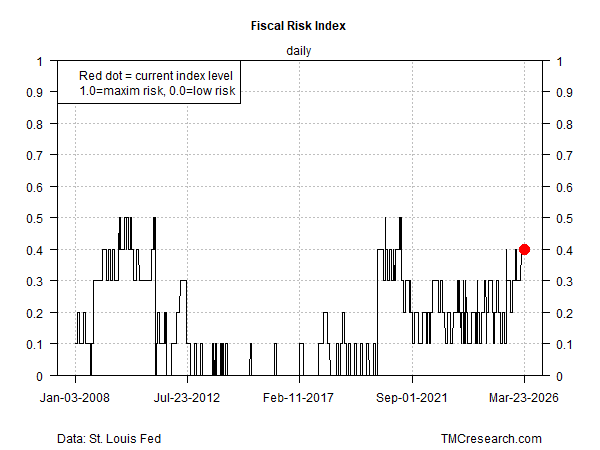

Fiscal Risk Index

US fiscal pressure has increased lately, according to TMC Research’s Fiscal Risk Index (FRI). The current reading rose to 0.4, rebounding once again to the highest level since the pandemic.

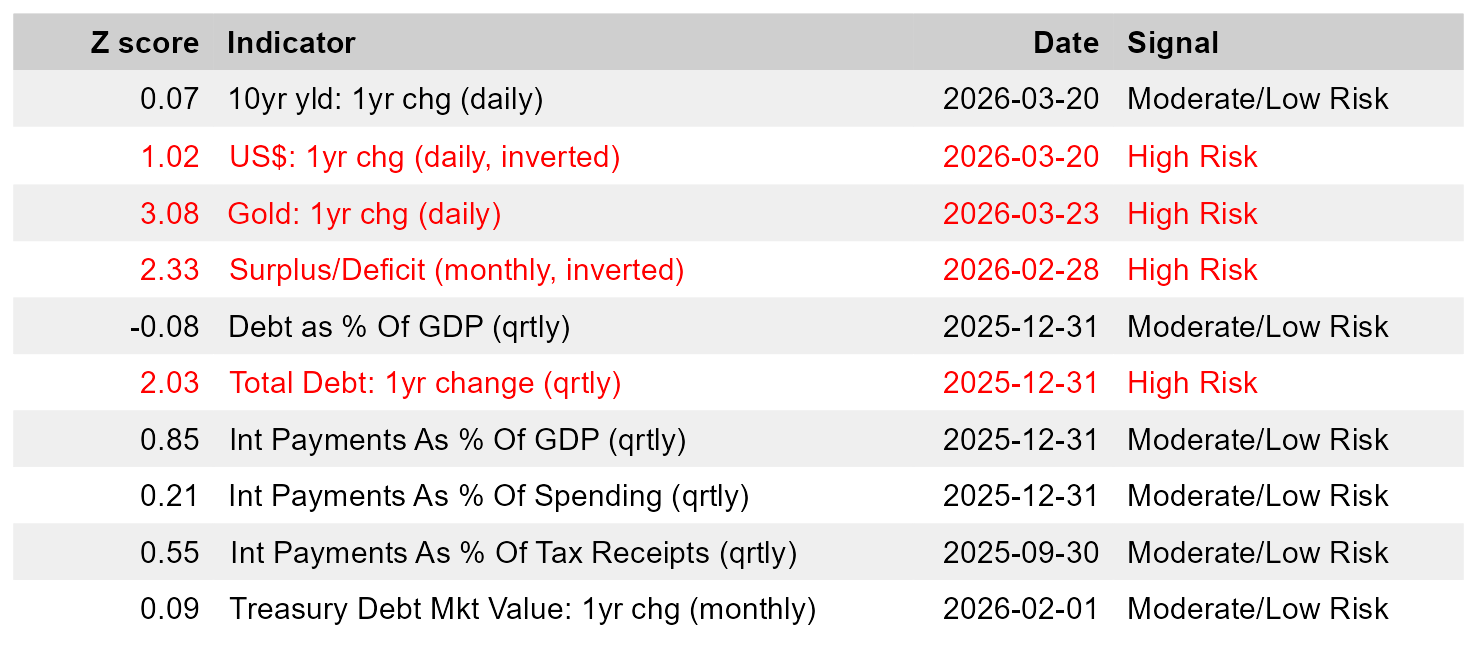

The increase shows that four of FRI’s ten inputs (see table below) are flashing warning signs, relatively speaking, based on our assumptions for modeling the data.

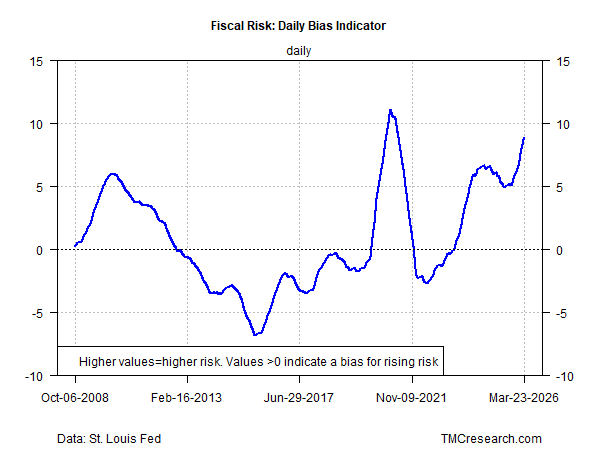

For another perspective, the Fiscal Risk: Daily Bias Indicator sums the z-scores for the ten inputs above, providing a more sensitive profile of how the aggregate mix is trending. On that basis, fiscal risk is approaching levels last seen during the pandemic (see chart below).

Our standard caveat for these indicators is worth repeating — namely, modeling fiscal risk is challenging for several reasons and the analysis above is, at best, a rough first approximation. In addition to the difficulty of quantitatively estimating the level of fiscal risk, there’s also debate about how much debt the financial markets will bear before demanding a significantly higher risk premium.

Further complicating the picture is a recent research paper arguing that financialization and deficit‑fueled spending have been key drivers of profit growth and market expansion, propping up elevated equity valuations even as fiscal vulnerabilities mount.

The common theme from our analysis that aligns with reporting from other sources: the deficit trend is still moving in the wrong direction. That’s worrisome on its face, and even more problematic when you consider that Washington has yet to lay out a credible plan to address the rising tide of red ink.

Hey! Just saw your post and thought I’d reach out—I really respect what you’re doing. I write about trading, mainly SPY and VIX, so it’s not exactly the same niche, but I think there’s still some overlap in audience. I’d appreciate your support, and if you like the content, maybe even a sub. Here’s one of my latest posts—curious to hear what you think.

This is a solid framing of the fiscal backdrop and the direction of travel.

The part I think is still underexplored is the mechanism through which fiscal risk actually transmits into markets. It’s often framed as a question of when investors “demand” a higher premium, but in practice it may be more about balance sheet capacity and collateral circulation.

Treasuries aren’t just assets, they’re the system’s core collateral. So the constraint isn’t necessarily demand, but how much can be intermediated and financed efficiently as issuance rises.

That distinction matters because it suggests stress may show up in liquidity and market functioning before it shows up cleanly in yields or inflation expectations.