Upside Inflation Bias Continues as Fed Faces Data Blackout

By James Picerno | The Milwaukee Company

Alternative inflation indexes suggest pricing pressure will continue in the near term

The Fed is expected to cut rates again, but the government shutdown clouds the outlook because key data updates could be postponed

Consumer sentiment weakened in September, driven by rising concerns over inflation

Consumers are concerned about prices and inflation, according to the latest survey by the Conference Board. The consultancy’s widely-followed survey for September highlights weakening consumer confidence amid worries about prices and inflation, the latter being “the main topic influencing consumers’ views of the economy.”

It’s still debatable if the recent rebound in inflation in recent months will be a temporary, moderate affair, or an early sign of new run of pricing pressures that will require a hawkish pivot in monetary policy. The Federal Reserve seems to be leaning toward the temporary/moderate view, based on the central bank’s decision to cut interest rates last month and prioritize a softer labor market as the higher priority.

A key update that is expected to provide timely clarification ahead of the next Fed meeting on Oct. 29: September consumer inflation data, scheduled for release on Oct. 15. Fed funds futures are currently pricing a near-certainty that the central bank will ease policy again by 25 basis points at the end of the month.

The upcoming consumer price index (CPI) report could crucial for deciding if further easing is appropriate, assuming the update is published. The government shutdown that started on Wednesday (Oct. 1) threatens to complicate and cloud the Fed’s analysis by keeping the door locked at the Bureau of Labor Statistics and other federal agencies that publish economic data.

A quick resolution to the political impasse in Washington would keep the inflation updates on track, but there’s also a non-zero possibility that, given the level of partisan animosity, the government shutdown stretches into weeks. Since 1976, the government has shut down 20 times, the longest (in 2018-2019) lasting 34 days.

Whatever happens, the inflation outlook could remain cloudy until the full effects of tariffs emerge in the months ahead. Meantime, in an effort to separate the noise from signal in real time, TMC Research monitors several alternative inflation indexes published by two regional Fed banks to check on the robustness of the recent trend shift in the standard CPI data.

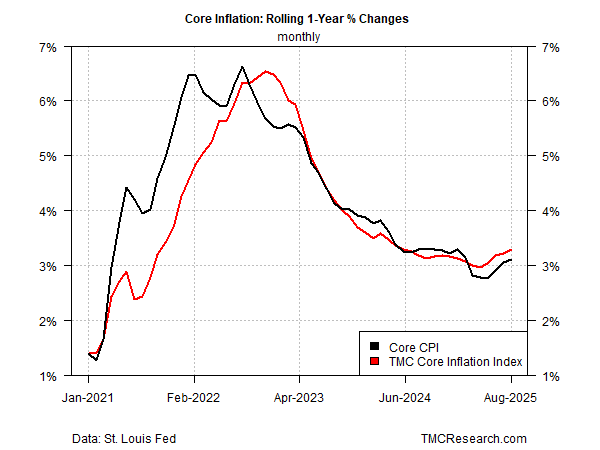

For example, the chart below compares core CPI’s 1-year trend against the TMC Core Inflation Index (CII), which is the median of five measures of prices that use varying methodologies to identify the underlying trend. The logic for this approach: any one inflation index has pros and cons, and so reviewing a range of alternatives offers a more reliable measure of the pricing bias.

The key takeaway: CII is confirming that inflation’s upward bias is picking up, rising further above of the Fed’s 2% inflation target through August.

Core readings of inflation, which strip out food and energy, are useful because studies show that excluding those commodities delivers a more reliable measure of the trend vs. headline indexes that include those items, which tend to be relatively volatile and move with greater independence vis-à-vis changes in monetary policy.

On that basis, the faster pace and ongoing acceleration in CII suggests that inflationary momentum has further to run in year-over-year terms. If September inflation data reconfirms the trend (assuming the data is published), the case for another Fed rate cut will be harder to justify at the end of the month.

On the other hand, if hiring is still slowing in September, perhaps further policy easing is prudent. For the moment, however, the official government data is on hiatus, and so private-sector estimates are the only game in town. On that front, the results are mixed, according to two updates this week:

The ADP Employment Report for last month indicates that companies cut payrolls for a second straight month in September. By contrast, non-farm payrolls rose 60,000 last, a moderate improvement over the previous month, according to estimates by Revelio Labs, a data analytics firm.

Here are the five price indexes used to calculate the TMC Core Inflation Index: