Think All Small-Cap Funds Are Alike? Think Again

By James Picerno | The Milwaukee Company

Small-cap ETFs vary widely because there’s no consensus on defining “small cap” stocks

Benchmark rules also matter for risk and return

No one-size-fits-all — fund choice depends on several variables, including how it fits within a larger asset allocation strategy

Choosing an index mutual fund or ETF that tracks a large-cap stock benchmark is a relatively straightforward affair if the benchmark is weighted by market capitalization. There’s only one way to rank the largest companies on this metric and so the indexes and the funds that track them are tightly correlated and post similar, if not near-identical, risk and return numbers.

There are differences to consider for big-cap index funds, of course, but they generally matter less (a lot less, in some cases) compared with selecting small-cap funds. Results for small-cap index investing, in other words, can vary by a substantial degree, depending on the fund’s benchmark. The differences for standard large-cap ETFs tracking market-weight indexes, by comparison, are slight by comparison.

The first question for picking a small cap fund: What’s the line that separates “small” from “big”? There’s no consensus and so the rules vary, which in turn can cast a long shadow over risk and return. By some accounts, small cap refers to a range between $250 million and $2 billion, but that’s far from universal. One small-cap fund can target a substantially different set of companies vs. a competitor and so generalizing in this corner carries significant risks.

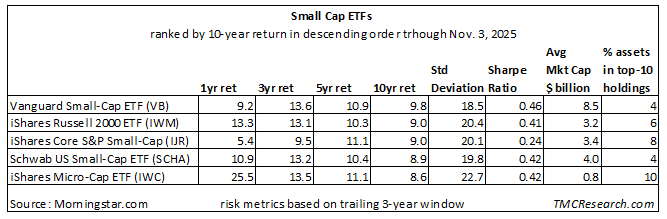

Consider the largest small-cap ETFs, based on assets under management, according to ETFdb.com. For example, Vanguard Small-Cap ETF (VB) has an average market cap of $8.5 billion – more than double the comparable figure for a leading competitor -- iShares Russell 2000 ETF (IWM) -- via data from Morningstar.com. (Note: for simplicity, we’re excluding factor tilts within the small-cap space and so value and growth strategies are ignored in favor of focusing on so-called core or blend funds.)

For some strategists, small cap means any company that’s not big enough to be in the mid- or large-cap universes. On that basis, a so-called micro-cap ETF are merely the smallest of the small. But others counter that micro cap is a subset of “small cap” and deserves separate consideration. In any case, the iShares Micro-Cap ETF (IWC) portfolio’s average market cap is far below the other small cap funds in the table – roughly $800 million, which is less than 10% of the average market cap for Vanguard Small Cap ETF (VB), which clocks in at $8.5 billion, the highest for the list above.

Another variation on differentiating small-cap funds is the use of filters, if any. The iShares Core S&P Small-Cap ETF (IJR) tracks the S&P Small Cap 600 Index, which has a profitability screen for companies. S&P Dow Jones Indices, which oversees the index, notes the S&P 600 has an “earnings requirement” and so “companies must have a track record of positive earnings before they are eligible to be added to the index.”

The Russell 2000 Index (the benchmark for IWM), by contrast, doesn’t screen constituents for profitability and instead simply holds the 2,000 smallest stocks in the Russell 3000 Index, which targets 98% of the US equity market. As such, the Russell 2000 Index has a higher level of risk for the dimension of profitability vs. the S&P 600 – a risk that can be linked to a higher, or lower, returns vs. other benchmarks during certain periods, depending on market conditions and other factors.

Rebalancing frequency also differs for some small-cap indexes. The S&P 600 is rebalanced quarterly vs. the annual “reconstitution” for the Russell 2000.

Unsurprisingly, the differences in how “small cap” is defined translate to different return and risk profiles – profiles that are in sharp relief lately. As shown in the table above, there’s a huge 20 percentage-point spread between the best performer in the table vs. the weakest fund over the past year.

Although it’s tempting to conclude that the “best” small-cap fund is the one with the highest recent performance, that rule of thumb is usually misguided since leadership in this space can be fluid at times, perhaps in unexpected ways.

Ultimately, intelligently picking a small cap fund (beyond the generic variables such as favoring low fees and sufficient trading liquidity) depends on multiple variables, some of which are investor specific. For example, one fund may be a stronger candidate than a competitor’s, thanks to superior diversification benefits for an existing portfolio. An investor’s plan for managing the overall risk of an asset allocation strategy is another factor.

There are no generic solutions when it comes to selecting a small cap fund. Much depends on expectations, investment strategy, time horizon, etc.

The good news is that the small-cap niche has a wide variety of choices – dozens of small-cap “blend” ETFs are trading, according to ETFdb.com, and there are many more when you include products with factor tilts.

Yet minds will differ on which fund is preferable. That’s hardly surprising when you consider that there are no standard investing strategies, assumptions, or risk expectations when it comes to integrating small-cap stocks into a broader asset allocation plan.