The US Dollar’s Slide Has Been A Tailwind For Investing In Foreign Markets

By James Picerno | The Milwaukee Company

The US Dollar Index dropped to a four-year low on Jan. 27

Dollar weakness has become a meaningful driver of outperformance for foreign assets

Hedging currency risk has been a headwind recently for international investing

The recent decline in the US dollar relative to foreign currencies may seem like an abstract concept for investors. But the ebb and flow of the greenback can be a crucial factor for risk and return in globally diversified portfolios. That alone is a reason to monitor the dollar’s trend for deciding if currency hedging looks reasonable.

Foreign exchange risk doesn’t receive as much attention in the US compared with the rest of the world, which can be explained by the size and relative independence of the American economy and running the world’s reserve currency. But international investing levels the playing field for everyone, and so hedging forex risk, or not, can be a crucial aspect for portfolio strategies.

Forex’s influence waxes and wanes across the years, depending on macro backdrop. Theoretically, the expected return associated with forex risk is zero in the long run. But over shorter periods currencies rise and fall, sometimes dramatically, and the US dollar isn’t immune. As a result, the forex factor can be a non-trivial influence on performance for anyone who ventures into foreign markets.

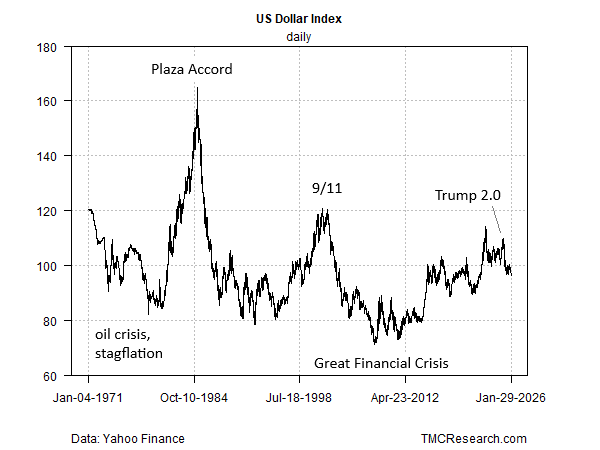

For historical context, the chart below shows the US Dollar Index (a basket of major foreign currencies) since the early 1970s, with select events that coincided with peaks and troughs. The significance is that a rising (falling) dollar translates into a headwind (tailwind) for US investors holding offshore stocks and bonds.

Like all risks factors, forex can help or hurt, depending on exposure, time period, and other variables. The main question for investors holding international assets: To hedge or not to hedge forex risk?

There’s no right answer for everyone since every investor is different in terms of risk tolerance, investment objective, time horizon, etc. What’s clear is that whatever you decide, the results could be significant, for ill or good.

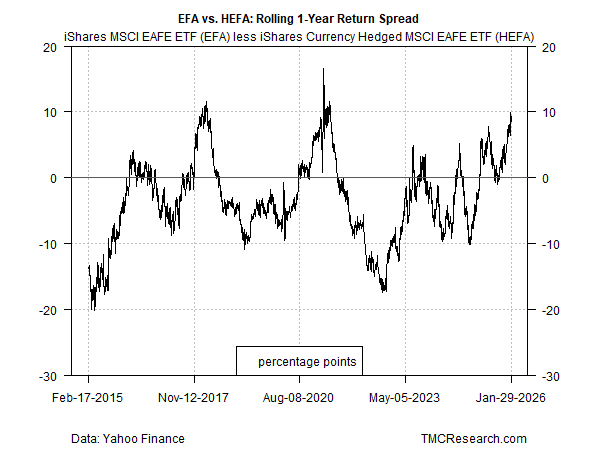

As an example, consider the rolling one-year return spread for two iShares ETFs targeting stocks in developed markets ex-US, based on the MSCI EAFE Index. The key difference between these ETFs: one fund is essentially unhedged in forex terms (EFA), the other employs forex hedging (HEFA). When the line in the chart is rising, the unhedged ETF (EFA) is outperforming, and vice versa.

The key insight: outperformance goes through cycles, driven partly by forex trends. In recent history, the unhedged fund has beaten its hedge counterpart by roughly 9 percentage points (as of Jan. 29, 2026).

EFA’s stronger run has been supported by a weak dollar. The US Dollar Index has dropped more than 10% over the past year.

Owning foreign assets in unhedged-dollar terms has juiced returns lately, but this isn’t a constant. At some point, unhedged currency risk will work against you, as it has at times in the past.

Weighing the pros and cons of hedging, to minimize if not eliminate the currency effect, starts by deciding if forex risk is worthwhile. A useful place to start the analysis is developing a view on the outlook for the dollar. The recent slide in the greenback is related to several factors, including concerns about tariffs, America’s growing federal budget deficit, lingering worries about inflation, and uncertainty about how the next chair of the Federal Reserve will manage monetary policy (Keven Warsh, who nominated by President Trump on Friday).

President Trump recently fueled speculation that the White House favors a weak-dollar policy. On Jan. 27, The Wall Street Journal asked the President if the dollar’s decline was excessive. “No, I think it’s great,” he responded. “The value of the dollar — look at the business we’re doing.”

US fiscal risk may be the biggest catalyst for the weak-dollar narrative for the foreseeable future. US debt as a share of GDP was roughly 121% as of 2025’s third quarter — close to a record high in the modern era — and is on track to rise further, to 134% by 2035, according to a recent estimate by the Committee for a Responsible Federal Budget, a self-described non-partisan think tank in Washington.

In some corners of academia, there are growing concerns that fiscal deficits may have been positively intertwined with the steady, gradual rise in corporate earnings and profitability. The argument is that government spending adds to the bottom line of companies, while investment in productivity has declined over time, suggesting that, absent any structural shocks, the growing debt-to-GDP ratio doesn’t appear likely to reverse. Additionally, the U.S. economy’s growing reliance on AI-related spending, which is being driven by the so-called hyperscalers and is increasingly financed through more esoteric private credit instruments, has drawn renewed attention.

Whatever the reasons, a weak dollar will boost returns for returns for foreign stocks and bonds for US investors, all else equal. At some point the cycle will play out and the dollar will rebound. Forecasting the turning point is impossible. Meantime, the bearish bias for the greenback remains a tailwind for offshore investments sans currency hedging.

Fascinating. Your breakdown of the dollar's influence is super clear, especialy the bit about hedging. It really makes me wonder how much of this global economic dance will eventually be influenced by increasingly complex algorithmic trading, especialy as AI gets more sophisticated. A truly insightful piece.