The Price of Peace: Iran Negotiations Could Decide Whether Inflation Breaks or Builds

By James Picerno | The Milwaukee Company

Iran peace talks will dominate near‑term inflation risk through the energy channel

Central banks are split as price pressures stay elevated and data stays hot

Middle East stability — or renewed tension — remains the biggest swing factor ahead

A new peace proposal to end the war is reportedly under consideration between the US and Iran. Its success or failure will be a key driver of inflation risk, which has climbed since the conflict sent energy prices soaring. Even a durable end to the fighting — and a return to normal Gulf energy exports — would still leave elevated inflation pulsing through the global economy in the near term. The central question is whether hotter inflation proves temporary or persistent.

The answer will be a crucial factor for markets and the global economy in the weeks and months ahead. If price pressures stay higher for longer, the Federal Reserve and other central banks may feel compelled to tighten policy.

The Reserve Bank of Australia (RBA) decided earlier this week to start tightening policy. “As expected, developments in the Middle East are having an impact on inflation,” RBA announced. “Higher fuel prices are adding to inflation and there are indications that this is likely to have second-round effects on prices for goods and services more broadly.”

The Federal Reserve, by contrast, is widely expected to keep rates steady for now. Last week the Fed kept rates unchanged, and the Fed funds futures market expects the central bank will stand pat for the rest of the year.

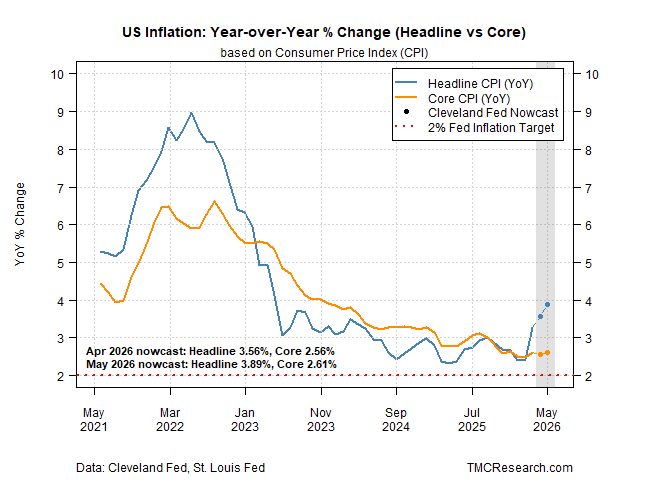

Incoming data may be the final arbiter, starting with next week’s April CPI report. Headline inflation jumped to 3.3% in March — a two‑year high — and economists expect the 3%‑plus trend to continue, running well above the Fed’s 2% target.

The Cleveland Fed’s inflation nowcast also sees prices remaining sticky. The regional Fed bank estimates that headline CPI’s annual pace will heat up to 3.6% in April and 3.9% in May.

Markets tend to price geopolitical risk asymmetrically: escalation premiums build quickly, but they unwind only when investors believe a durable resolution is plausible. A credible peace framework would therefore have immediate implications for inflation expectations, especially through the energy channel.

The Federal Reserve is watching these dynamics closely. While policymakers do not react to geopolitical events directly, they do respond to the inflation expectations channel. A meaningful decline in energy‑driven inflation expectations would strengthen the case for future rate cuts, whereas continued uncertainty could keep the Fed cautious. The trajectory of the Iran conflict—and the credibility of any peace proposal—has become intertwined with the central bank’s policy outlook.

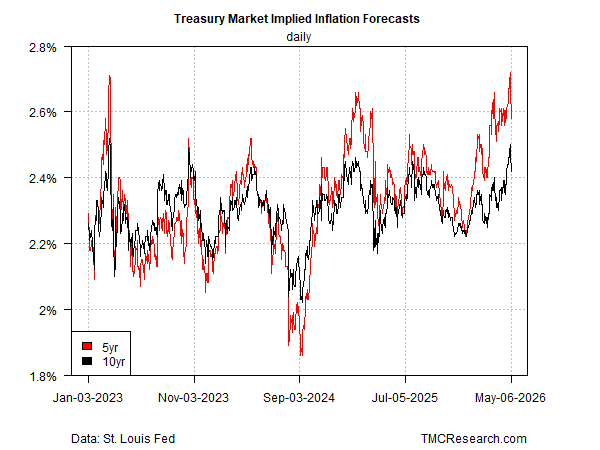

One sign of tentative optimism: the Treasury market’s implied inflation forecast has eased from its recent spike, with the 5‑year breakeven slipping to 2.58% (May 6) after peaking at 2.72% earlier this week.

Inflation’s path, however, will be shaped by far more than geopolitics. Wage growth, productivity trends, supply‑chain normalization, housing costs, consumer spending, and financial‑market conditions all influence how price pressures evolve. Layer on top the uncertainty surrounding global trade and fiscal policy, and the Fed faces a landscape where no single indicator can dominate the outlook.

Yet one factor stands above the rest in the near term: the trajectory of the Middle East conflict. Energy markets remain the fastest transmission channel for geopolitical shocks, and any shift toward peace — or renewed instability — would quickly ripple through oil prices, inflation expectations, and ultimately the Fed’s reaction function.

In an already crowded field of economic risks, the presence or absence of a credible peace framework is likely to exert the strongest influence on how inflation evolves in the months ahead.