The Ongoing Economic Expansion Is Helping Keep The Bull Market Alive

By James Picerno | The Milwaukee Company

Recession risk remains low, supporting the bull run in stocks

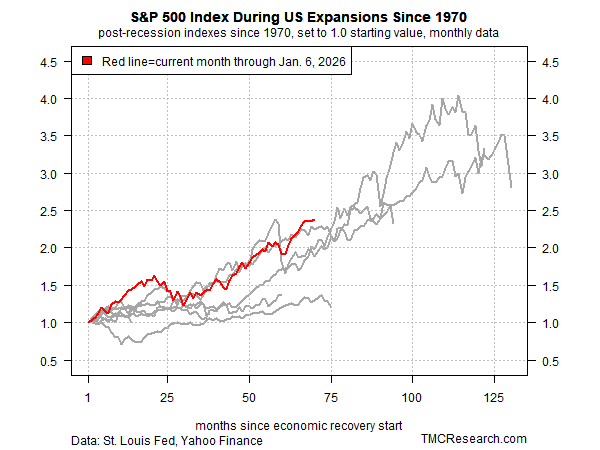

US equities are outperforming past post‑recession rallies

The bull market is expected to endure if the economic expansion continues

There are many factors that drive bull and bear markets for stocks, but arguably the first among equals is the business cycle.

More than a year ago, TMC Research noted that the outlook for stocks remained positive, in part because the risk of recession appeared low. Fast forward to today, and the S&P 500 Index is up 19% since those remarks were published and closed at a new record high on Tuesday (Jan. 6). Although the catalysts for higher share prices extends beyond the business cycle proper, it’s fair to say that economic growth promotes and supports bullish conditions, creating fertile ground for growing corporate earnings, for instance.

Stocks can and do correct when the economy’s expanding, and so it’s important to avoid the trap of assuming that market risk is always low when a recession isn’t threatening or underway. Other factors can and do arise that derail equities. Recent examples include the sharp but temporary market slide last April after President Trump announced US tariffs. And during much of 2022, US shares trended down, cutting the S&P 500 by 19% that year. In both cases, the economy was expanding, which is to say that the market tumbled despite the absence of an NBER-defined recession.

Using the business cycle for guidance on the outlook for stocks is useful, but it’s no silver bullet, especially in the short term. But for the task of assembling a list of factors that are likely to influence the directional bias of equities beyond the immediate horizon, if not longer, the broad economic bias is a solid place to start.

The business cycle, in short, can be thought of as a crucial source of fuel for bull and bear markets. One could say that the ebb and flow of expansions and recessions are the crucial known risk factors underlying market cycles. Accordingly, stocks tend to rise during periods of economic growth, and suffer during recessions.

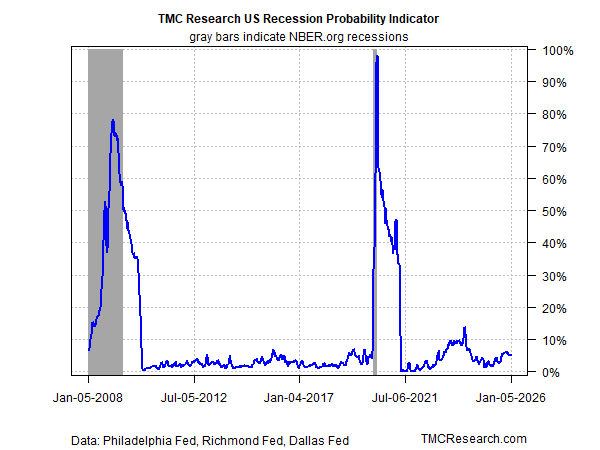

With that in mind, recession risk remains low for the US, based on the TMC Recession Probability Indicator, which currently estimates a roughly 5% probability that the economy is contracting, or is in imminent danger of sliding over to the dark side.

Recent nowcasts for the government’s upcoming fourth-quarter GDP report suggest as much. The Atlanta Fed’s GDPNow model, for instance, is estimating (as of Jan. 5) that while economic output will slow in Q4, the 2.7% nowcast, if correct, will leave the economy humming at a moderate pace after posting strong gains in each of the previous two quarters.

To be fair, there may be important caveats beneath the surface of the headline GDP figures. Reuters reported that roughly two-thirds of US GDP growth in the first half of the year was tied to the AI infrastructure buildout. Separately, The Economist argued in August of last year that the US AI boom may be squeezing the rest of the economy, noting that the technology sector, while accounting for roughly 7.5% of total GDP, has contributed close to 40% of overall growth.

For the moment, the bull market in stocks does not appear immediately threatened, at least not in terms of rising recession risk. Near record-high valuations and the economy’s growing sensitivity to a relatively narrow segment of activity make the market increasingly susceptible to shifts in sentiment. However, measuring the S&P 500’s historical record from the start of economic expansions since 1970 highlight that the present rally in equities is outperforming its predecessors at this stage of rallies following recessions. Investors, in sum, remain optimistic despite various risks.

How long will the bull market run? No one knows, of course, but for now the odds appear favorable to the extent that the economy continues to sidestep a new recession.