The Hidden Flaw in Passive Investing: Tracking Market Weights May Not Always Be a Smart Asset Allocation Strategy

By James Picerno | The Milwaukee Company

Passive tends to work inside an asset class, while customizing may matter more for investing in several markets

Investors face finite time horizons and various behavioral challenges

Risk‑tuned asset allocation could potentially deliver steadier, more “livable” outcomes

The case for indexing is well‑established, supported by academic and empirical research. But while there’s a strong case for passive investing within an asset class, in our view the argument weakens—if not breaks down—when the focus turns to multi‑asset‑class portfolio strategies.

There are several reasons why asset allocation may reasonably be customized, which is to say intentionally designed to deviate from a passively managed, market‑value‑weighted strategy. One of the more compelling factors: the time horizon for a passive asset‑allocation strategy is optimal, in theory, only for the average investor with an infinite time horizon. No individual investor matches that profile, which lays the groundwork for customizing asset allocation for a real‑world portfolio.

The apparent contradiction between favoring passive strategies within an asset class vs. customizing strategies that use several asset classes isn’t inconsistent upon closer inspection. Markets are relatively efficient (or at least hard to beat) within a particular asset class. The most compelling example is large‑cap U.S. stocks, as S&P Global’s periodic updates remind. A recent update reports:

Of all active large‑cap U.S. equity funds measured, 79% underperformed the S&P 500 in 2025, worse than the 65% rate observed in 2024 and the fourth‑worst year for active large‑cap managers over the 25‑year history of the SPIVA Scorecards.

Using index funds to capture asset class beta is defensible, if not compelling, but the rationale doesn’t always transfer to asset allocation for reasons related to risk management, particularly for individual investors. Saving for retirement, planning for college expenses, and similar goals are bound up with finite time horizons, even if they run for several decades. That’s a mismatch with a market‑value‑weighted asset‑allocation strategy that, in theory, would hold all investable asset classes and never rebalance.

A passive asset‑allocation strategy may be tough to beat over very long stretches of time, but investors have financial needs in the short term that require liquidating investments. There are also behavioral factors in play that raise the value of “livability” in portfolios. The short‑run volatility that a passively managed asset‑allocation strategy may exhibit could be a bridge too far for some—perhaps many—individuals. The ideal investment plan for the long haul is worthless if market volatility triggers a flight‑to‑safety decision during the depths of a bear market.

Managing risk, in other words, is necessary, but in our view, it tends to work best at the asset‑allocation level. One reason: while markets tend to be efficient within asset classes—which implies indexing is preferable in this context—cross‑asset‑class efficiency is often substantially lower.

Some research hints at the possibility that trading frictions can be higher and capital flows slower between asset classes at certain times compared with transactions within asset classes. One explanatory theory is that most market participants are highly specialized in a given asset class, in contrast to the smaller group of generalists who focus on reallocating capital across markets, such as stocks, bonds, real estate and commodities.

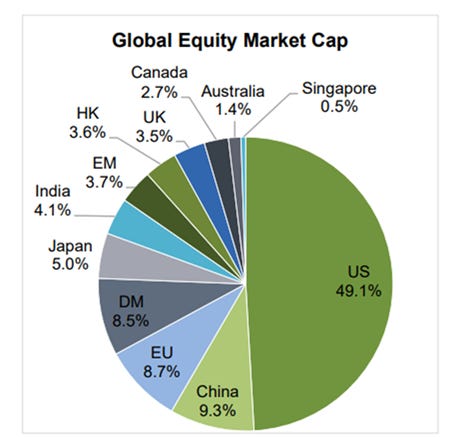

A contributing factor may be related to various behavioral biases and industry constraints. For instance, home bias—a tendency to invest a disproportionately high share of a portfolio in one’s domestic market—may play a role. Consider that U.S. equities in 2024 represented nearly half of global stock‑market capitalization, according to SIFMA, a financial‑industry trade group. Tracking a passive mix of global stocks translates to a 50/50 allocation. Most U.S.‑based investors with international equity exposure are probably holding substantially lower levels of foreign stocks.

Capital bottlenecks could also play a role—capital flows across borders, although streamlined in recent years, are still less efficient than money management within borders.

Another dimension is complex macro dynamics, including geopolitical risk and manipulated foreign‑exchange values, which also reduce cross‑border and cross‑asset allocation efficiency relative to single asset classes within a country. But therein lies a degree of opportunity, since lower market efficiency raises the potential for mining portfolio alpha through tactical asset allocation and related strategies.

Keep in mind that alpha can be defined in terms of risk‑adjusted return. That’s a key point, since individuals don’t have 50‑year investment windows. Retirement dates, college funding, home purchases, and health‑related expenses create fixed deadlines. A deep drawdown close to one of those deadlines can permanently impair outcomes because there isn’t enough time for markets to recover.

An added complication: humans are not rational compounding machines. They are emotional, pattern‑seeking, and loss‑averse. Risk management can reduce the emotional triggers that activate these biases. Shallower drawdowns, for example, mean fewer panic decisions. More stable return paths reduce temptations to chase performance.

Customizing an asset‑allocation strategy using low‑cost index funds tends to be the more effective path for managing risk and designing portfolios that are “livable,” while providing investment solutions that match an investor’s goals, risk tolerance, and other factors. This approach may, over the very long run, trail a true passive asset allocation that holds all investable markets in proportion to their market values. But as a practical compromise for real‑world investing, it’s a reasonable—if not compelling—concession to potentially deliver more stable outcomes for investors who must balance growth with the practical realities of time, behavior, and risk.