The Bond Market Is Downplaying Fiscal And Inflation Risks, Focusing On Rate Cuts And Softer Economic Growth

By James Picerno | The Milwaukee Company

The 30-year Treasury yield is trading near April lows despite concerns about US debt

Investors are prioritizing economic growth worries over inflation or fiscal risk

A sentiment shift could spark a sharp reversal in long-bond yields.

The US government’s rising debt burden is old news. The question is whether the bond market will price in the elevated risk anytime soon?

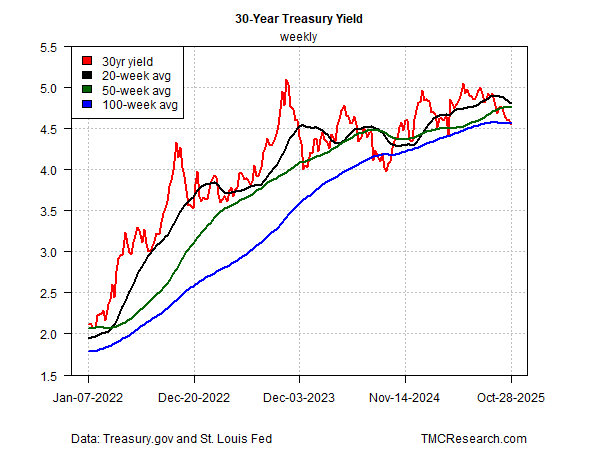

Judging by the recent slide in yields, investors aren’t worried. Consider the 30-year Treasury rate, the most-sensitive maturity for inflation risk and fiscal worries. If the last several months are a guide, the appetite for the long bond has been robust, driving the 30-year yield down to 4.55%, close to the lowest level since April (bond prices and yields move inversely).

Fiscal risk remains worrisome, even if market sentiment suggests otherwise. The already elevated 125% debt-to-GDP ratio (a measure of general government gross liabilities relative to the size of the economy) is projected to reach 143% (the second-highest level after pandemic-driven red ink) by the end of the decade, according to IMF forecasts.

The budget deficit is also raising red flags. The IMF estimates that the US government will run a shortfall of 7%-plus relative to GDP through 2030, marking the highest for any rich nation in the IMF’s database.

Waiting for solutions

How the debt burden is addressed could be as problematic as the red ink itself. Some analysts think that using inflation as a solution is easier political path for reducing the debt burden in real (inflation-adjusted) terms. The alternatives, such as raising taxes, lowering spending, or hoping that economic growth will ramp up sharply are considered substantially less-plausible scenarios.

Why, then, isn’t the bond market worried? If inflation is the path of least resistance at a time of rising debt, presumably the bond ghouls would be repricing fixed-income securities to reflect the risk, especially at the long end of the yield curve. Yet the opposite has been unfolding.

One explanation is that the bond market is focused on expectations for slower economic growth, which in turn will persuade the Federal Reserve to cut interest rates, as it’s widely expected to do in today’s monetary policy meeting. In that scenario, locking in today’s yields is a compelling trade, which will look increasingly attractive if the Fed continues to ease monetary policy.

Today’s yields are yesterday’s news

But market sentiment is fickle. Expectations for rate cuts and softer growth may be close to fully priced in. Unless a recession is likely, which still looks like a low probability at this point, rate cuts may soon end. If so, bond investors may refocus on inflation and fiscal risks in the months ahead.

Last week’s inflation report for September may have bought some time for deciding which way the macro winds are blowing. The headline rate of the consumer price index ticked up to a 3.0% pace vs. the year-ago level, the highest since January. Yet the gradual upswing in recent months has yet to trigger concerns in the Treasury market.

The 30-year yield is a useful proxy for monitoring inflation concerns, and on that front the trend still looks friendly, based on a weekly measure, which reduces some of the short-term noise.

If and when sentiment in the bond market shifts, and inflation and/or fiscal risk takes center stage for investors, an early sign of the attitude adjustment will likely show in the weekly 30-year yield chart.

Some market pundits argue that the bond market is underpricing inflation and fiscal risks. Perhaps, but it’s important to separate what you think should happen from how the market is trading. The old Wall Street line comes to mind: the market can stay irrational for longer than you can remain liquid.

When and if Treasuries pivot away from slowing growth, a downshift in hiring, and recession risk, we’re likely to see a marked upturn in the 30-year-yield trend. In other words, a clear reversal from what the chart above is currently indicating.

Meantime, the 30-year rate continues to trade in a range this year. A break to the downside from current levels will indicate a growing concern about softer economic conditions. In that scenario, inflation and fiscal risk will be further relegated to fringes of market concerns.

For how long? That depends on the incoming data, although for the moment that’s on hold until the government shutdown ends.