Testing Gold and Bitcoin As Portfolio Diversification Tools

By James Picerno | The Milwaukee Company

A simple test of adding gold and/or bitcoin to a stock and bond portfolio highlights key differences in risk and reward associated with these alternative assets

A backtest that adds bitcoin to a stock/bond mix raised performance sharply, but at a cost of dramatically higher portfolio risk

Gold, by contrast, does a better job of lowering portfolio risk, but only modestly lifts overall portfolio return

Alternative assets are enjoying a banner year. Two of the hottest: bitcoin and gold. Both are outperforming stocks, bonds, broad measures of commodities and property shares via real estate investment trusts by wide margins so far in 2025.

Holding bitcoin, gold, or both has been a win-win for portfolio design lately, which suggests that these assets should be included in every asset allocation plan. But a closer look at the numbers reminds that there’s more to evaluating assets than simply picking the winners in recent history.

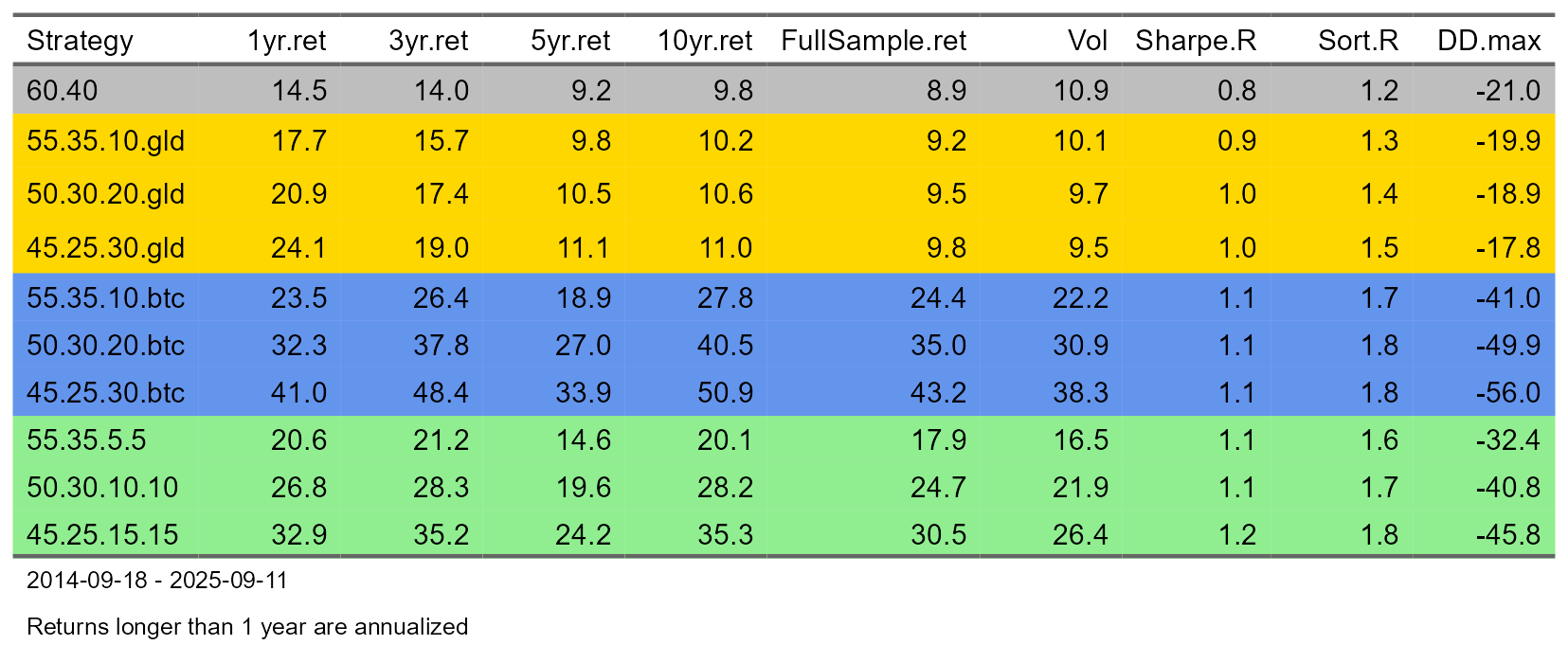

Variations on a Theme

As a starting point for analyzing how gold and bitcoin influence a traditional investment portfolio, TMC Research ran a backtest using ETFs representing US stocks, US bonds, gold and bitcoin (see fund list below). The benchmark is a simple 60% equities/40% bonds mix. Variations of this 60/40 mix are tested by incrementally adding gold, bitcoin, or both, with commensurate declines in stocks and bonds.

For example, in the table below, three adjustments to the baseline 60/40 portfolio (grey row at top) are made by adding gold and reducing weights in stocks and bonds (rows highlighted in yellow). As one illustration, the 55% Stocks/35% Bonds/10% Gold (GLD) portfolio (identified as the 55.35.10.gld strategy): 1) cuts stocks by 5 percentage points to a 55% weight; 2) trims bonds from 40% to 35% and; 3) redeploys to gold via a 10% weight. In all, there are three portfolios with varying degrees of a gold allocation at 5%, 10%, and 20%.

The same adjustments to the 60/40 benchmark are applied using bitcoin – for example, the 55.35.10.btc strategy holds a 10% weight in bitcoin, financed by a reduction in stocks and bonds by 5 percentage points each. (The three strategy variations that add bitcoin are highlighted in blue.)

For the third set of strategy tests, portfolios hold equal weights in gold and bitcoin and lower amounts of stocks and bonds (green rows). For instance, one variation of the 60/40 portfolio is revised so that stocks and bonds are cut to 55% and 35% weights, respectively, with 5% shifting to gold and 5% to bitcoin (55.35.5.5 strategy).

Unsurprisingly, the results show that the more gold and/or bitcoin held, the higher the portfolio performance. The caveat is that the sample period tested only dates to 2014, a limitation related to bitcoin’s short history. The years since then primarily reflect a strong bull market for the asset. The original cryptocurrency was launched in 2009, but the data set we’re using (Yahoo Finance) begins in 2014, arguably the year when bitcoin started moving from the fringes of finance into the mainstream. As such, 2014 is the earliest common date for all the assets.

In other words, the bitcoin results reflect a strong bullish bias in the extreme. Simply put, there’s a reasonable case to make that the test presented doesn’t fully capture the risk of a bear cycle that could weigh on the cryptocurrency for an extended period in the future. The same caveat applies also applies to stocks, bonds, and gold, although the scale of bitcoin’s rally is far greater.

Risk Lessons

All that aside, the test highlights several takeaways beyond the fact that recent history has been kind to investors adding gold and/or bitcoin. The first observation: Despite a roaring bull market in alternative assets in recent years, adding bitcoin substantially raises overall portfolio risk.

One could argue the sharply higher risk is worthwhile to earn a significantly higher return. Agreement or disagreement on that point depends on each investor’s objective, time horizon, and other factors that influence how to customize a portfolio for a specific individual (or institution).

The fact remains that history (at least since 2014) shows that holding more bitcoin raises portfolio risk. How much more? It depends on the risk metric. Take maximum drawdown, which measures the deepest peak-to-trough decline. In the table above, the 60/40’s steepest drawdown is -21% -- a non-trivial interim loss that doubles with a 10% weight in bitcoin (55.35.10.btc).

Compare that with a 10% weight in gold, which lowers the maximum drawdown, albeit only slightly, based on the 55.35.10.gld strategy, while lifting performance a bit for the full-sample period.

Crypto advocates can rightly counter that the full-sample return for the strategies that hold bitcoin rise several fold over the 60/40 mix and relative to the strategies holding gold.

A related question: How do the risk-adjusted returns compare? Two metrics are shown to estimate answers: Sharpe ratio and Sortino ratio. Each measures return per unit of risk (return volatility), with the Sharpe ratio treating upside and downside vol equally, while Sortino focuses on downside risk, offering a better approximation of how investors treat real-world volatility. In both cases, a higher reading equates with a higher risk-adjusted performance.

Both risk measures indicate that gold and bitcoin improve risk-adjusted performance. That said, the improvement stalls for allocations above a 10% weight in gold and/or bitcoin.

Overall, the results suggest that while bitcoin is promoted by some as a digital version of gold, the risk profile of the two assets is quite different, at least over the past decade or so. Bitcoin, in short, is far riskier than gold, although so far that higher risk has translated into sharply higher returns for the cryptocurrency.

The crucial question centers on whether the substantially higher performance for bitcoin vs. gold, stocks or bonds is worth the sharp increase in risk? Comparison of the Sharpe ratios suggests not, although there’s more scope for a cautious “yes” based on the Sortino ratios.

Perhaps the bigger hurdle is the maximum-drawdown track record. Everyone wants higher returns, but deciding if the potential for a sharply deeper, if temporary, portfolio loss may be a price too high to bear for some investors.

For most investors, the bitcoin risk hurdle may be a bridge too far in search of portfolio diversification. One reason: digital assets, including bitcoin, are often subject to periods of heightened volatility, commonly referred to as “crypto winters,” which can occur when regulatory developments, macroeconomic conditions, or shifts in risk sentiment are unfavorable. These periods can result in swift and sharp drawdowns, as was the case in much of 2022 and in December of 2017. On the other hand, the results above suggest that a small amount of bitcoin may be sufficiently potent to reap most of the rewards from a strategic portfolio perspective. Gold, by contrast, seems to require a higher weight for relatively meaningful results.

Keep in mind that the rosy view in the current rear-view mirror presented above may be misleading. All the more so when you consider that the next decade for the leading cryptocurrency — with a minuscule (and therefore highly speculative) track record vs. stocks, bonds and gold — could look very different from the previous ten years.

By contrast, stocks, bonds and gold have long histories across many business cycles, which is valuable for gaming out future scenarios. Bitcoin, by contrast, is still in the early innings for proving what it’s capable of, or not, in different macroeconomic conditions.

The backtest above was conducted with the following ETF proxies:

* US stocks: SPDR S&P 500 (SPY)

* US bonds: iShares Core US Aggregate Bond (AGG)

* Gold: SPDR Gold Trust (GLD)

Bitcoin: Grayscale Bitcoin Trust (GBTC), backfilled with bitcoin price via Yahoo Finance prior to 2015