Stock–Bond Dynamics May Be in Flux, but Global Diversification Proved Its Worth In 2026

By James Picerno | The Milwaukee Company

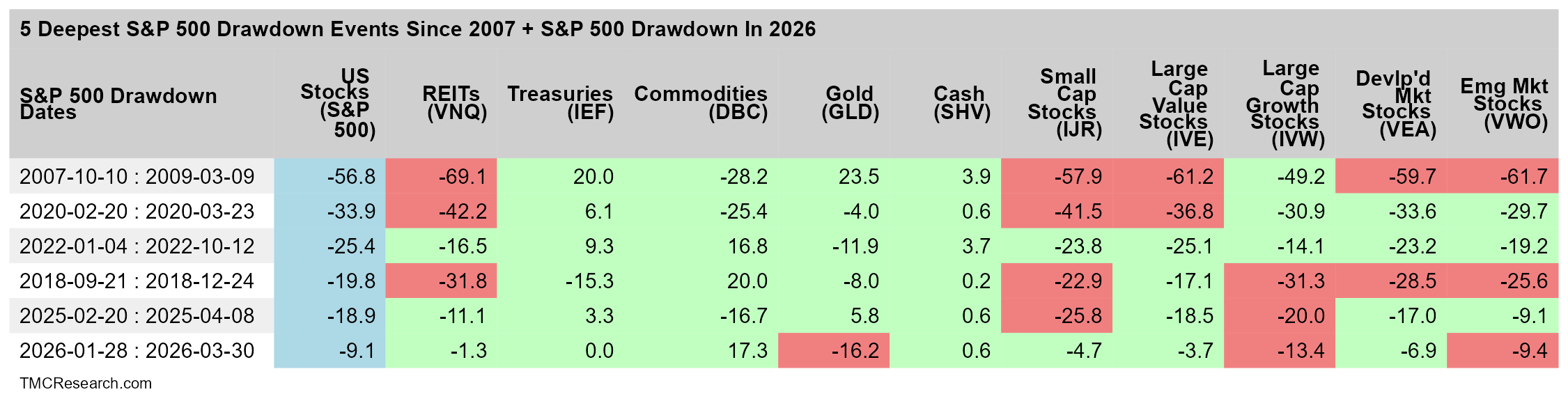

Several asset classes beat the S&P 500 during the 2026 drawdown

Treasuries, commodities, and cash have routinely outperformed the S&P in recent drawdowns

Cash remained the only asset to post absolute outperformance in every major drawdown since 2007

The recent rise in the correlation between stocks and bonds has sparked debate about assumptions for risk models and the role of asset allocation. The market volatility triggered by the Iran conflict has only sharpened the discussion about what to expect from cross‑asset relationships in the design and management of investment portfolios.

One way to monitor and evaluate asset allocation’s value as a risk-management tool is tracking how markets behave during the steepest drawdowns for U.S. stocks. Last October, TMC Research analyzed the five deepest peak‑to‑trough declines in the S&P 500 Index since 2007 relative to ten markets that, at various times, provide some degree of hedging against sharp losses in U.S. equities. In today’s update, the results of this year’s S&P 500 drawdown are added to the mix.

As shown in the table below, the benefits of a diversified portfolio across asset classes proved valuable once more in the recent stock-market decline. This year’s S&P 500 drawdown was relatively moderate by historical standards—the 11th deepest since 2007, briefly touching a 9.1% loss from the previous peak. Seven of the ten markets listed outperformed U.S. stocks, either in relative or absolute terms, based on a set of proxy ETFs.

The dates shown in the table (reading left to right) indicate the S&P’s peaks and troughs for each drawdown event. This year’s decline (bottom row) cut the S&P by 9.1% before the market recovered.

The assets that fared worse than the S&P 500 during this year’s drawdown: gold (GLD), large‑cap growth stocks (IVW), and emerging‑markets equities (VWO). The best performer during this year’s correction: commodities (DBC), which surged more than 17% during the S&P 500’s slide.

Note, too, that only three asset classes have outperformed the S&P in all six drawdown events listed in the table: Treasuries (IEF), commodities (DBC), and cash (SHV). Although outright gains were recorded in several cases, only cash (SHV) consistently outperformed in absolute terms across all six episodes.

The key lesson from the results above is unchanged from our previous update: diversifying across asset classes remains a useful risk‑management tool. Although the relationships between asset classes aren’t fixed and continue to evolve, the general strategy of holding a global portfolio as a hedge against uncertainty still looks compelling.

History doesn’t offer any guarantees on how assets will perform in the next crisis, but using this year’s stock‑market correction as a guide suggests that maintaining broad, multi‑asset exposure is a powerful tool for navigating an increasingly unstable investment landscape.