Steady Inflation Supports More Rate Cuts, But Markets Still See A Pause Ahead

By James Picerno | The Milwaukee Company

Inflation remains steady, giving the Fed room to cut interest rates

Markets are still pricing a near-term pause despite moderately tight policy

Mixed signals from the labor market, inflation, and the Powell probe will keep the 2026 rate path uncertain for the near term

US consumer inflation remained steady in December, providing the Federal Reserve with more room to lower interest rates. But market-based expectations suggest the central bank will remain cautious on further rate cuts for the near term after easing policy three times last year.

Although it’s not directly relevant, the news this week that the US Department of Justice launched a criminal investigation of Federal Reserve Chair Jerome Powell potentially adds another layer of uncertainty for assessing the outlook for monetary policy. But after reviewing a range of indicators, the outlook remains mixed for more rate cuts in the near term.

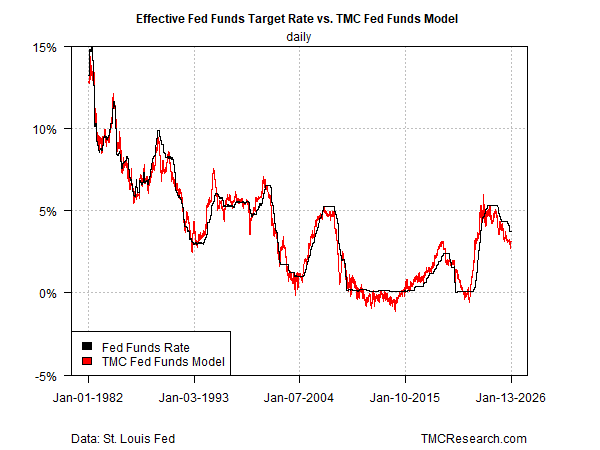

The key economic factors that will guide policy in 2026: inflation and the labor market. The latest numbers on these fronts suggest there’s still a case for more easing. Meanwhile, TMC Research’s Fed Funds Model indicates that current monetary policy remains moderately tight, which leaves the central bank with space for additional dovish adjustments.

Let’s start with inflation. The Bureau of Labor Statistics reports that consumer inflation held steady in December for the year-over-year trend. For both headline and core readings of the Consumer Price Index (CPI), pricing pressure stabilized from the previous month, rising 2.7% and 2.6% from the year-earlier level, respectively.

Although there are still data concerns for CPI, due to lingering effects from the government shutdown, taking the numbers at face value suggests inflation remains sticky in the mid-2% range. That’s moderately above the Fed’s 2% target, but inflation isn’t reheating, which implies that rate cuts are still possible.

Combine the behaved CPI data with the slowdown in the labor market in the second half of last year and a recipe for easing emerges, or so one can argue. Yet deciding why hiring has slowed will be crucial for deciding if more rate cuts are warranted.

At issue is whether the softer pace of hiring reflects business-cycle weakness vs. still-healthy growth that’s linked to a lower “breakeven” for job creation due to recent declines in US net immigration. Though the probability of finding a job hit a record low of 43.1% in December, according to the Federal Reserve Bank of New York’s latest Survey of Consumer Expectations, this lends slightly more credence to the former than the latter narrative.

Identifying which explanation is more influential (or whether both play a role) will likely take several more months before a consensus begins to emerge.

Meanwhile, TMC Research’s Fed funds model still shows monetary policy running moderately tight, implying that the target rate can be cut while still maintaining a slightly hawkish stance.

By our estimate, the current target rate is roughly 90 basis points above the optimal rate, which is our assessment of neutral for a set of financial and economic indicators. The current spread continues to reflect a middling degree of tightness compared to the range since September.

Market expectations continue to anticipate that the Fed will keep rates steady for the near term. Fed funds futures are estimating a high probability for no change at the next policy meeting scheduled for Jan. 28. Looking further out, the odds slide, but still favor standing pat for the two subsequent meetings in March and April.

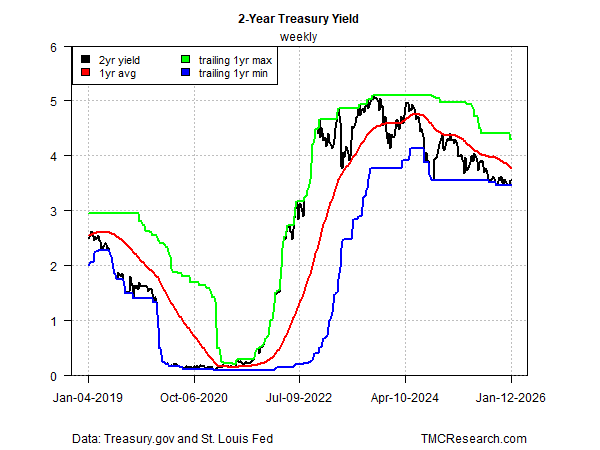

The bond market also suggests that the Fed may pause with rates cuts at the next meeting. In particular, the policy-sensitive 2-year yield is trading around 3.5%, which is also the low end of the current range for the Fed funds rate. The implication: the market is comfortable with the current target rate. That’s a significant change from recent history, when the 2-year yield traded well below the target rate, a spread that foreshadowed rate cuts.

Reasoned or not, the Fed looks set to keep rate steady for the near term. Although there’s a case for another cut or two, economic conditions are still muddled from the effects of the government shutdown and other factors. As new numbers arrive, and the state of inflation and the labor market become clearer, the Fed will reassess the wisdom of cutting rates further or standing pat.