Stagflation Risk Keeps Uncertainty High For Fed’s Upcoming Policy Decisions

By James Picerno | The Milwaukee Company | jpicerno@themilwaukeecompany.com

The Fed still appears to be struggling with deciding if inflation is a bigger risk than slower economic growth.

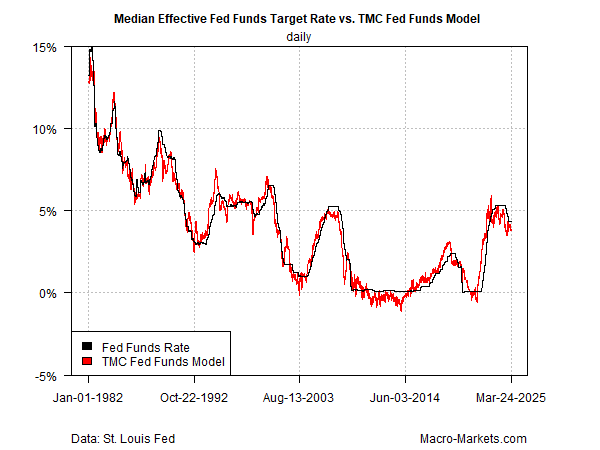

TMC Research’s Fed funds model anticipates a moderate bias for a rate cut in the near future.

A key source of uncertainty for monetary policy: how or if inflation changes due to Trump tariffs that are scheduled to take effect on Apr. 2.

Signs of slower US economic growth continue to emerge while inflation remains “sticky.” A degree if stagflation risk, in other words, remains a near-term challenge for policy decisions.

The central bank’s standard playbook is to focus on either supporting economic growth and boosting hiring with low interest rates and rate cuts, vs. taming an inflationary bias with high rates and rate hikes. The two strategies tend to conflict with one another. Normally that’s not an issue because most of the time one or the other dominates. But in the current environment, the combination of slowing economic growth and inflation that’s no longer moving lower, closer to the Fed’s 2% target, is creating uncertainty about how policy will evolve for the near term.

The TMC Fed Funds model, which estimates the optimal target rate based on several economic and financial factors, shows that the Fed is keeping its interest rate moderately higher than current conditions suggest is optimal. The implication: there’s a slight bias for cutting rates in the near term.

Most Fed officials continue to expect that the central bank will lower interest rates this year, despite higher inflation expectations of late, based on last week’s policy meeting, when the central bank announced it would keep its target rate unchanged at a 4.25%-to-4.50% range. The “appropriate” path for the median Fed funds rate, according to policymakers, should fall to a median 3.9% this year, based on the latest projections, the central bank reports.

In the week since those estimates were published, some Fed officials have revised their outlook to account for inflation. Atlanta Fed President Raphael Bostic on Monday said he now anticipates only one rate cut this year rather than his previous forecast of two cuts. His reasoning: he foresees inflation as “very bumpy” and on track to remain steady. In an interview with Bloomberg, he added that reducing inflation to align with the Fed’s 2% inflation target will take longer, perhaps not arriving until 2027, he advises.

Federal Reserve governor Adriana Kugler today said she favors keeping interest rates steady for “some time.” Reflecting a bit more hawkish stance than Bostic, she explained: “I am paying close attention to the acceleration of price increases and higher inflation expectations, especially given the recent bout of inflation in the past few years.”

The Fed is still expected to remain in a wait-and-see mode for the next policy meeting on May 7, based on Fed funds futures. A key uncertainty that’s expected to be closely monitored is how, or if, inflation and/or economic activity changes in response to Trump tariff policies, which are set to take effect on Apr. 2.

Futures are currently pricing in a moderately high probability (66%) for a rate cut at the Jun. 18 policy meeting, based on CME data. The implied estimate suggests that slowing economic will become a higher priority for the Fed, if only on the margins.

Read a pdf version of this article: