Slowing Labor Market Strengthens The Case For A Fed Rate Cut Next Week

By James Picerno | The Milwaukee Company

A weak jobs report and a slight rise in unemployment in August suggest the Federal Reserve will cut interest rates at the Sep. 17 policy meeting.

The bond market, Fed funds futures, and TMC Research’s Fed funds model indicate that a rate cut is a high-probability event.

The main uncertainty surrounding the expected rate cut is this week’s release of consumer inflation data for August.

The tepid rise in August payrolls gives the Federal Reserve another data point to cite for cutting its target interest rate at the next monetary policy meeting on Sep. 17.

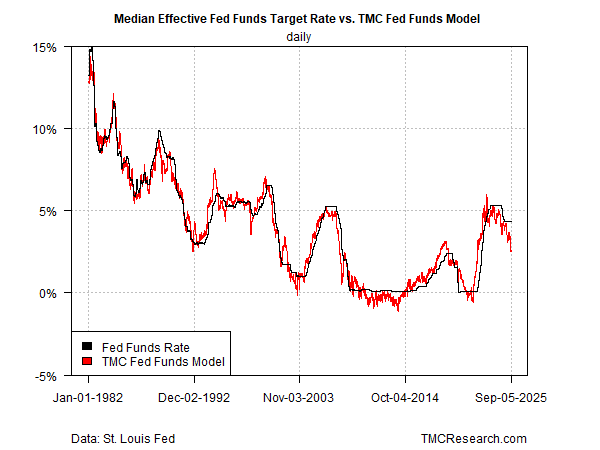

The bond market is certainly pricing in a new round of easing. A dovish pivot is also expected via TMC Research’s Fed Funds Model, which continues to signal that a rate cut is appropriate.

Let’s start with the labor market. The economy added just 22,000 jobs last month – well below what economists were expecting and close to the weakest monthly gain since the pandemic. Add sign of weak hiring: the June estimate for payrolls was revised down to show a modest loss, the first monthly decline since the pandemic. The unemployment rate rose slightly to 4.3% -- still low by historical standards, but enough to lift the jobless rate to its highest level in nearly four years.

The numbers suggest that the labor market is stalling, which gives the Fed more leeway to argue that a rate cut is appropriate. The consensus outlook is for a 1/4-point cut, but the slowdown in hiring raises the possibility that a ½-point cut may be under consideration.

TMC Research’s Fed Funds Model has been indicating for several months that a rate cut is appropriate. The model’s logic is based on analyzing several macro factors – multiple measures of inflation, real interest rates, the labor market, economic conditions and the yield curve – that offer a rough estimate of the optimal or neutral rate.

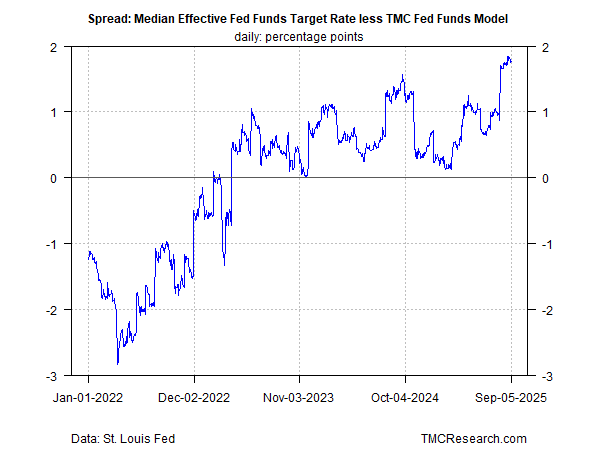

In our periodic updates over the summer, this indicator has routinely signaled that policy was moderately tight relative to current conditions, a view shown by Fed funds rate holding above the model’s estimate for an optimal rate. The spread signals that the case for a rate cut has strengthened lately — the median Fed funds rate is now close to 2 percentage points above the estimated neutral rate. That’s a robust sign that policy is tight – arguably too tight for current conditions.

The central bank’s reluctance to ease so far is linked to concerns that tariff-related inflation remains a concern and so a dovish policy pivot could be ill-timed for keeping a lid on pricing pressure. The dilemma for the Fed is that in recent months prices have shown only modest increases, suggesting tariffs have had limited impact as businesses absorbed much of the cost.

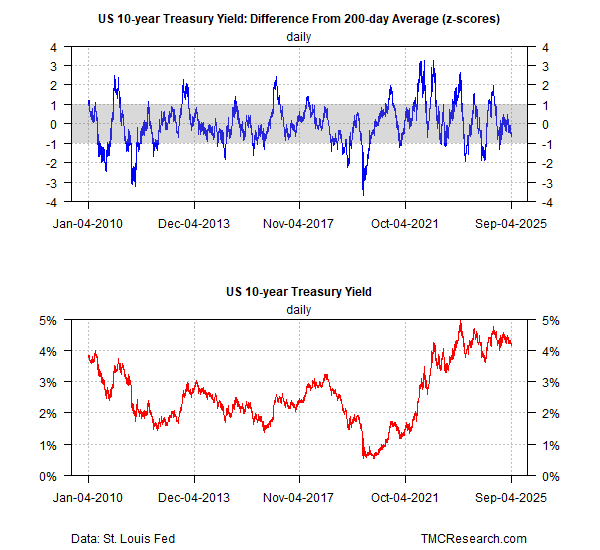

The pushback is that inflation could accelerate in the months ahead, reflecting a delayed reaction from tariffs. Yet the bond market doesn’t appear worried at the moment. The US 10-year Treasury yield, for example, has remained relatively stable recently. As shown in the charts below, the benchmark yield has held in a “normal” range lately (within the grey zone in the top chart).

This week’s update on consumer inflation for August (Thurs., Sep. 11) could test the Fed’s capacity to cut rates next week. But for now, at least, the market remains convinced that a rate cut is a high-probability forecast, which implies that the Fed is more concerned about a slowing economy than rising inflation. Fed funds futures reflect this view and continue to price in a high probability (90%) for a 1/4-point cut next week.

The main uncertainty centers on Thursday’s CPI data for August. Economists expect headline inflation to edge up to 2.9% in year-over-year terms, which would mark the highest level since January and further above the Fed’s 2% inflation target. But if the economy’s slowing, a gradual rise in pricing pressure probably won’t derail a Fed rate cut, in part because slower growth is disinflationary and will cool some of the tariff-related inflation effect.