Shutdown Threatens Next Week's Inflation Report, Making Fed's Job Harder

By James Picerno | The Milwaukee Company

The government shutdown could delay next week’s inflation report

Uncertainty is rising for the next Fed policy decision as economic data is postponed or canceled

Markets are still expecting another rate cut at the end of the month

The government’s September report on consumer price inflation (CPI) is scheduled for release next week (Wed., Oct. 15), but the main uncertainty isn’t about the numbers. Rather, the question is whether the data will be published on time. At the moment, the odds don’t look encouraging, thanks to the ongoing government shutdown.

The Bureau of Labor Statistics is reportedly working on a plan to bring some employees back from furlough to publish the data, but as of this writing there’s no official confirmation. [UPDATE: BLS advises it will release the CPI report for September on Fri., Oct. 24, but “No other releases will be rescheduled or produced until the resumption of regular government services.”]

This much is clear: Incoming CPI updates are especially critical for the Federal Reserve these days as it attempts to navigate between signs of a slowing labor market and a modest but persistent rise in the inflation trend in recent months.

Whether there’s new inflation data or not, the next monetary policy meeting is approaching, set for Oct. 29. Even with a normal schedule of inflation updates, the Fed’s job has become increasingly challenging as tries to decide if tariffs will lift inflation. As a result, the central bank must decide if inflation risk should take a back seat to prioritizing the downshift in hiring lately.

Rate cuts are still the expected policy path

Most Fed policymakers support further rate cuts, according to the minutes from the last FOMC meeting on Sep. 16-17, when the central bank announced a ¼-point cut – the first reduction this year.

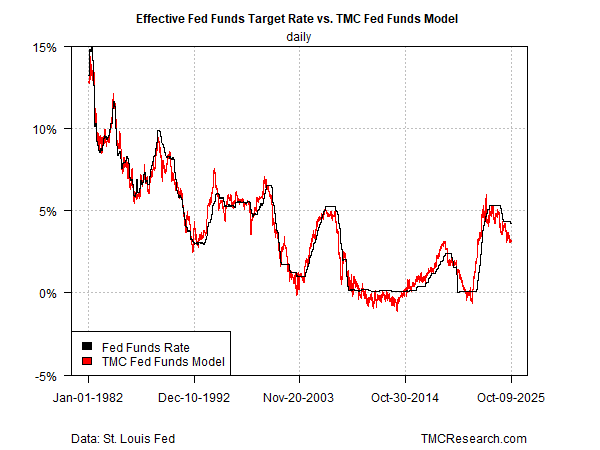

TMC Research’s Fed funds model continues to indicate that policy remains moderately tight, which implies that there’s still a case for rate cuts while maintaining a relatively hawkish bias to combat inflation. Our current estimate: the effective Fed funds rate is a bit more than one percentage point above the neutral rate, based on modeling inflation, economic activity and other macro factors – a spread that’s remained relatively stable in recent weeks.

The market continues to expect another rate cut at the end of the month, based on the Fed funds futures estimate, which is pricing in a 95% probability that the central bank will ease policy for a second time this year on Oct. 29.

No sign of inflation anxiety in the 10-year yield

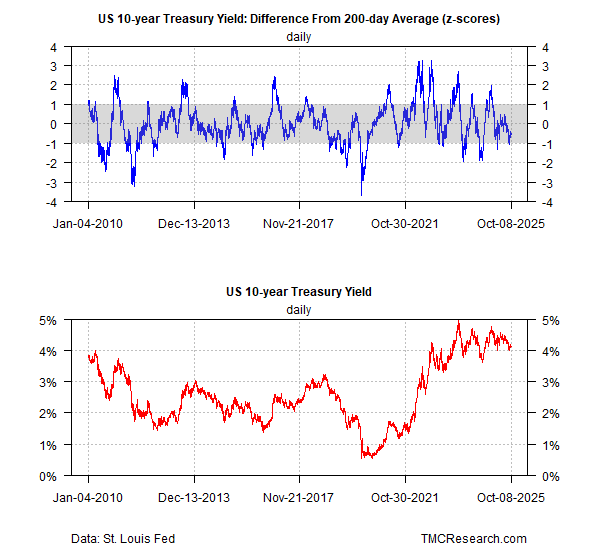

Concern about future inflation appears muted in the bond market via the US 10-year Treasury yield. The benchmark rate has been trading around 4.1% lately, which is near the lower end of its range so far in 2025.

Mixed outlook for inflation from various sources

The jury’s still out on whether tariffs will raise inflation in the months ahead. The recent pickup in the 1-year change for headline and core CPI through August suggests that pricing pressure may be strengthening. The core reading rose to a 3.1% increase vs. the year-ago level, the highest since February and well above the Fed’s 2% target. Headline CPI’s rise is softer, but it’s also turned up in recent months.

Despite moderately hotter inflation, Fed officials generally see the bigger risk in a slowing job market, which aligns with easing policy to stimulate hiring.

New York Fed President John Williams supports more rate cuts even as inflation has edged higher. “The risks of a further slowdown in the labor market is something I’m very focused on,” he said on Thursday. He reasoned that inflation risk has eased in recent months compared with the initial view after the increase in tariffs in the spring. Williams also expected that the tariff-related impact on inflation to fade over time.

Yet there are hints that inflation could rise further before peaking. The New York Fed this week updated its monthly consumer survey, noting: “Median inflation expectations in September increased at the one-year-ahead horizon to 3.4% from 3.2% and at the five-year-ahead horizon to 3.0% from 2.9%.”

At the betting market Kalshi, a slight majority (52%) expect that headline CPI will top 3.0% in September (up from 2.9% in August).

If the shutdown continues into the second half of the month, the CPI report for September might be scrapped entirely and raise questions about whether October data will be published.

“If we’re up to October 22, October 23? That — to me — is almost a cutoff point where we should start to think [that] we’re probably not going to have an October CPI,” said Omair Sharif, the president of Inflation Insights, a consultancy.

The Fed, of course, remains open, thanks to funding that’s independent from Congress, and so the central bank is scheduled to make a decision on monetary policy at the end of the month, with or without updated inflation data from the government. It was a tough call before the shutdown, and it’s not getting easier if key data updates are postponed or cancelled. The risk of a policy mistake, as a result, could be rising.