Oil Spike May Scramble the Fed’s Policy Script as War in Iran Continues

By James Picerno | The Milwaukee Company

War-driven spike in oil prices pushes expected Fed cut from June to July at the earliest

Energy inflation risk complicates the outlook for monetary policy

The incoming Fed chair will be in the hot seat if war-related inflation heats up

The Federal Reserve was already facing a delicate transition as Kevin Warsh prepares to take over in May, pending Senate confirmation, when Fed Chair Jerome Powell’s term ends. The war in Iran adds another layer of uncertainty to an already fraught policy environment.

Energy prices have spiked since the US and Israel attacked Iran on Saturday, a conflict that’s slowed oil exports to a crawl through the Strait of Hormuz. Roughly one-fifth of the world’s seaborne oil trade moved through this strategic chokepoint last year. If this narrow waterway remains closed for an extended period, it raises the possibility that inflation could heat up and force the Fed to respond — if not by raising interest rates, then by delaying rate cuts for longer than recently expected.

Fed funds futures are now downplaying the odds of a rate cut in June. Before the war, this was considered the month when the central bank would start cutting again, extending last year’s run of easing. But the market is rethinking that logic and is now pricing in a moderately high probability that the Fed leaves rates steady in June, pushing out the expected date for the next cut to July or possibly September at the earliest.

The concern is that if energy costs remain elevated, the higher prices of crude oil, gasoline, and natural gas will soon feed through to the broader economy, delivering a so-called negative supply shock. Standard economic theory, along with the historical record, suggests that the higher prices will slow growth and lift inflation in some degree.

Energy prices are expected to fall once the conflict is over, but US and Israeli officials say the war could run for weeks. A related concern is that the widening damage to energy infrastructure in the Persian Gulf region from Iran’s retaliatory attacks will take time to repair, a bottleneck that will keep supplies lower for longer.

Geopolitics vs. monetary policy

The main concern for the Fed is how, or if, to respond to higher energy costs. To the extent that oil drives headline inflation higher, the shift presents an especially difficult challenge for monetary policy, since interest rates have no direct effect on the supply of crude. That’s one reason why the Fed and other central banks tend to target core measures of inflation, which strip out energy and food costs — a subset of pricing over which policy has substantial influence.

The Fed’s job will be even tougher because deciding if the war has raised inflation in a meaningful and persistent degree will take time. Next week’s scheduled release of consumer price inflation for February, for instance, is already irrelevant in the current environment.

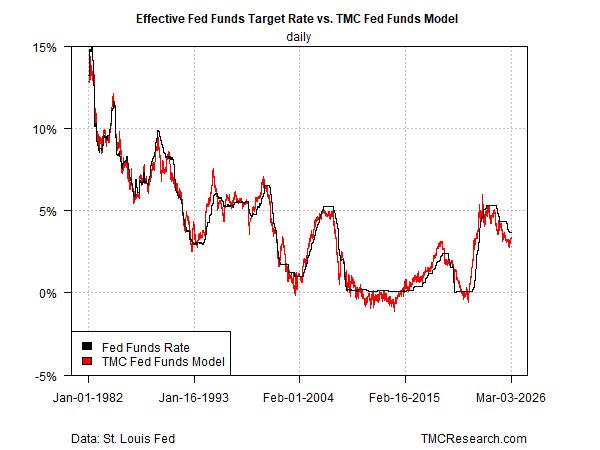

TMC Research’s Fed Model continues to indicate that policy remains modestly tight, but the hawkish spread of the effective Fed funds rate over our estimated neutral rate is fading. As recently as late-January, the Fed’s target rate was more than 60 basis points above this proxy for estimating an equilibrium level. The premium (implying a moderately hawkish bias) has been sliding since, dropping to under 30 basis points on Tuesday (Mar. 3). In other words, Fed policy is approaching a neutral bias, and looks set to continue into dovish terrain – a trend that may quickly become inappropriate if inflation heats up.

.

Hikes Off the Table — For Now

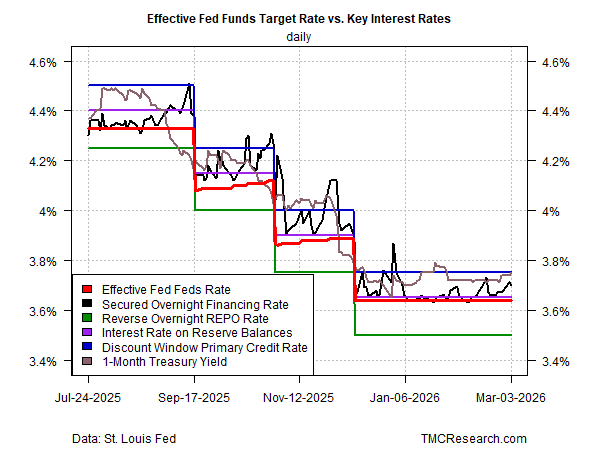

Rate hikes are still unlikely, based on market expectations for inflation. The Treasury market’s 5-year breakeven inflation rate (nominal less inflation-indexed yield) was just below 2.5% yesterday (Mar. 4), a middling level vs. recent history for this bond market inflation gauge.

The 1-month Treasury yield appears to be pricing in no change in the target rate, as it remains at the upper half of the policy channel. The calculus would change if the 1-month yield – currently at 3.75% — decisively breaks above the channel’s upper range, marked in the chart below by the Fed’s discount window primary rate, which is also at 3.75%. In that case, the shift would signal that the market is starting to factor in the possibility of a rate hike.

This macro mix would be hard enough for any new Fed chairman, but it may be especially challenging for Warsh, who has supported President Trump’s public calls for lower interest rates, partly on the view that an artificial-intelligence-driven productivity boom will boost economic growth without raising inflation.

Whatever the merits of that forecast (and there’s ongoing debate on the topic), the Iran war may rewrite the script for Warsh’s policy plans well before he arrives at the Eccles Building on Constitution Avenue.