Oil Is a Critical War Gauge for Tracking Iran Risk in Real Time

By James Picerno | The Milwaukee Company

The price of oil has come to be widely recognized as a valuable real‑time gauge of Iran‑war risk

Moves toward either price extreme since the war started would signal a shift in macro expectations

Stability near the midpoint implies investors see the status quo holding—for now

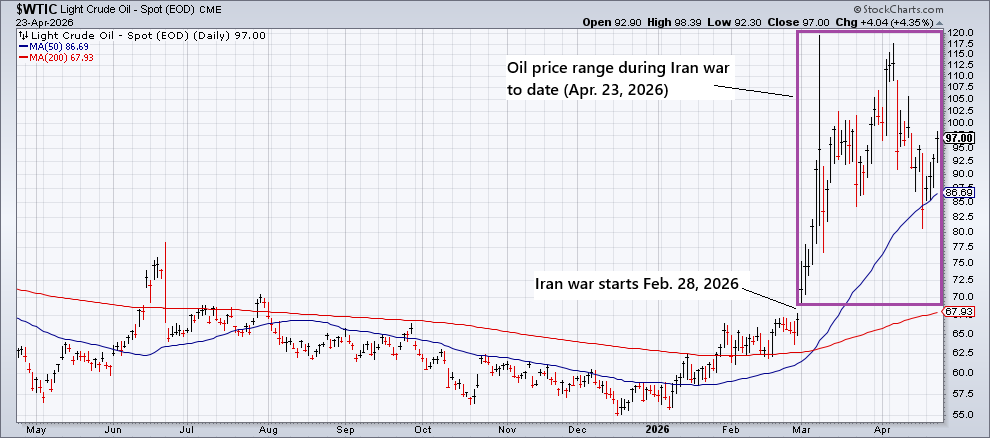

Tensions between the US and Iran remain elevated as a fragile ceasefire holds, but the war’s trajectory is still highly uncertain. Assessing risk in real time is difficult given how quickly conditions on the ground are evolving. One practical way to monitor sentiment and expectations in this environment is to track how crude oil trades relative to its history since the war started on Feb. 28.

Markets are imperfect, but shifts in oil prices tend to reflect a global, real‑time synthesis of information related to the conflict. The supply-side energy shock remains the war’s primary transmission channel, with disruption of oil and gas exports through the Strait of Hormuz driving the key macroeconomic and financial‑market risks for the global economy. Pricing this risk through oil offers a first‑order approximation of how investors are interpreting the conflict’s shifting contours.

Oil, in short, functions as a risk indicator—capturing sentiment about the war and the implied level of threat it poses for the global economy. A useful starting point is to frame the risk in terms of the range of oil prices since the attacks began on Feb. 28.

Using the US benchmark (West Texas Intermediate), prices have traded between roughly $70 and nearly $120 a barrel. The current level—around $97 (as of Apr. 23)—is near the midpoint of that range.

A significant move away from this middle zone toward either extreme, particularly over a period of days or weeks, would likely signal a meaningful shift in expectations about the war’s path. Such a move would also carry implications for the outlook on inflation, economic growth, and broader macro conditions.

For now, oil’s relative stability near the center of its war‑era range suggests that global investors expect current conditions to persist. The key development to watch is a decisive break—up or down—from this middling zone, which could reflect a material change in the conflict’s macroeconomic implications relative to the current outlook.

Ultimately, this framework deserves close attention because it distills a complex, fast‑moving conflict into a single, market‑based signal that captures how global investors are repricing risk in real time. Oil may not tell the whole story, but it reliably reflects the channel through which the war is most likely to affect macro conditions generally in the weeks and months ahead.

As long as the Strait of Hormuz remains a potential flashpoint, tracking crude’s price within its post-Feb. 28 range offers investors a clear, disciplined way to monitor whether the macro narrative is shifting—and how quickly those shifts may ripple through markets and portfolios.