New Research Highlights That One of Your Portfolio's Biggest Risks May Not Be the Market—It's Often Your Own Fear

By James Picerno | The Milwaukee Company

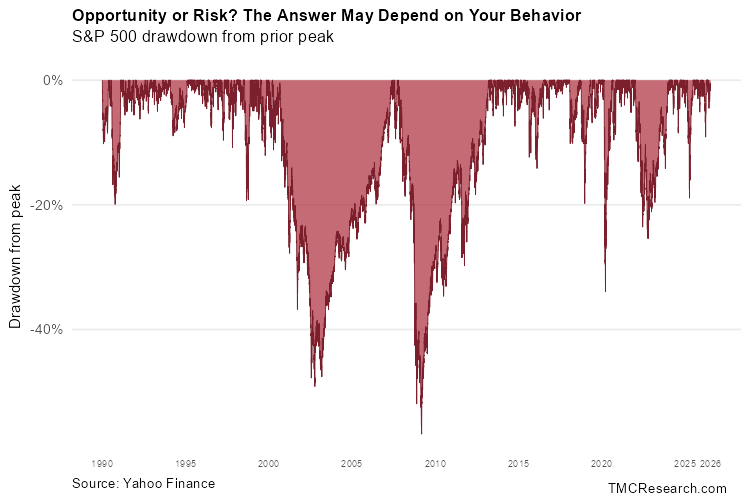

Investors often flee to safety fast, but crawl back to risk slowly

Fear tends to drive the trade, not math

Staying safe too long can cost you the recovery

One of the biggest threats to long‑term investing isn’t a volatile market or high fees, but it can be the way our brain reacts to them.

While we like to think of ourselves as rational, humans are hardwired to react emotionally to financial highs and lows — a vulnerability generally known as behavioral risk. When investors panic-sell during market drops or chase hyped-up trends at their peak, they run the risk of locking in losses and dragging down their returns. Ultimately, managing your own behavior and sticking to a plan can matter far more to your lifetime wealth than trying to outsmart the stock market.

There are various dimensions of behavioral risk, and perhaps the facet with the highest stakes arises during periods of extreme market volatility. A recent study adds crucial insight by demonstrating that investor behavior is itself highly volatile during periods when “safety” is in high demand. The analysis highlights several pitfalls that emerge when market stress is elevated, according to “Risk Perception under Uncertainty: A Behavioral Analysis of Safe-Haven Asset Return Responses,” published last month in the Journal of Research in Economics, Politics & Finance.

One of the study’s main findings is that investor risk is not a static, mathematical formula, but a dynamic, psychological reaction. That contrasts with traditional finance models, which treat risk as a two-way street and assume, for instance, that when market uncertainty rises by 10%, safe-haven prices go up by a matching 10%, and when uncertainty falls, they drop by the same degree. This paper shows that investor behavior is, in fact, highly asymmetric (unequal).

The research finds evidence of what might be called a panic premium, the extra cost added to certain assets during times of widespread fear or uncertainty. Markets can react violently to bad news, causing safe-haven prices to jump quickly. But when the dust settles, those prices don’t come down nearly as fast, because human fear lingers. If you buy during the panic, you may end up locked into an inflated price.

Investors react far more aggressively and persistently to increases in uncertainty — driven by loss aversion and panic — than they do to decreases in uncertainty. When a crisis hits, investors overreact and pile into safe assets, driving prices up rapidly.

The flip side of this behavioral pattern is that the recovery is slow. When the crisis ends and uncertainty falls, investors do not sell off their safe havens at the same speed. Fear lingers, causing safe-haven prices to remain elevated long after the actual danger has passed.

If you buy defensive assets during a crash, you probably aren’t solving a calculated math problem to optimize your expected payoff. Rather, you’re paying a premium for a “psychological anchor” that soothes your anxiety and stops the emotional pain of watching your portfolio drop. Contrast that with the standard financial-textbook assumption that investors are rational and will make logical, cold-blooded decisions, even when a portfolio has quickly lost 20%. In reality, biology takes over.

One lesson is to build a structured portfolio before the storm hits — often a more reliable way to protect yourself from your own inevitable, fear-driven decisions. Putting clear rules in place on how a portfolio will be managed through time — before a crisis strikes — is also prudent.

As the study notes, “The investment decision of an individual can be affected by psychological variables like uncertainty, anxiety, and fear... The helpfulness of the concept of rationality is limited in times of turmoil.”

This research highlights a subtle but consequential risk for investors: the loss-averse instinct that sends capital rushing into safe havens during spikes in market volatility, policy uncertainty, or geopolitical tension does not reverse with equal speed once conditions calm down. In short, investors tend to de-risk fast but re-risk slowly, if at all.

For an investment portfolio, this behavioral lag can translate into a tangible opportunity cost: capital that stays parked defensively out of lingering anxiety, rather than being redeployed once risk genuinely subsides, misses out on the recovery and growth phases of the market cycle. Over time, this pattern of overstaying in “safety” can quietly erode long-run returns relative to a more risk-tolerant, timely reallocation strategy — turning a rational, protective impulse in the moment into a source of underperformance in the long run.

None of this means that periodic adjustments to risk exposure is inherently a mistake. Tilting toward a more defensive asset allocation during periods of genuine stress is often a sound and necessary part of managing a portfolio through time. The problem isn’t the instinct to seek safety; it’s the tendency to stay there long after the original rationale has faded.

The real takeaway is that risk management works best as a deliberate, pre-planned process with well-designed rules rather than a reactive one driven by lingering fear. Investors who build a sound framework in advance — with defined triggers for both scaling into and out of safe havens — are better positioned to manage risk through time without falling into the trap of chronic overcaution.

Done well, risk management remains one of the most valuable tools an investor has; done reactively, it can quietly become one of the costliest.