Markets Price In Another Fed Rate Cut Next Week, But Friday's Delayed Inflation Report Could Muddy The Waters

By James Picerno | The Milwaukee Company

Markets are expecting that the Fed will cut its target rate again next Wednesday

Headline inflation may rise to 3.1% per consensus estimate, while core CPI holds steady—fueling both hawkish and dovish narratives.

Labor market signals remain murky amid the shutdown, leaving the Fed to decide policy in a data vacuum.

Market-based forecasts continue to expect the Federal Reserve will cut interest rates again next week at the Oct. 29 policy meeting. But getting from here to there requires going through tomorrow’s release of the delayed consumer inflation report for September.

Economists are looking for a mixed bag of numbers. The headline measure of the consumer price index (CPI) is on track to pick up to a 3.1% annual rate, the highest in nearly a year-and-a-half, according to Econoday.com’s survey. Core CPI, which strips out volatile food and energy prices and tends to be a more reliable measure of the trend, is projected to remain steady, also at 3.1%.

Assuming the estimates are correct, the CPI report will provide support for inflation hawks and doves, if only on the margins. The question is whether the update will strengthen or derail the case for another rate cut next week?

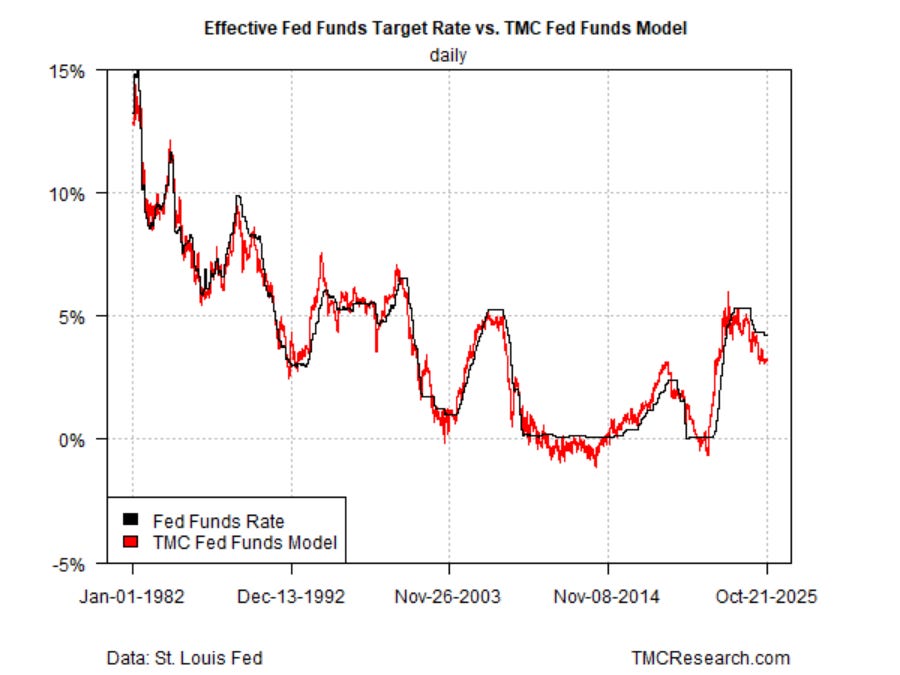

Policy is still moderately tight

TMC Research’s Fed funds model continues to indicate that monetary policy remains moderately tight. The effective Fed funds rate has been holding steady recently at roughly one percentage point above our neutral estimate. The gap leaves room for the Fed to cut while still leaving policy with a hawkish bias.

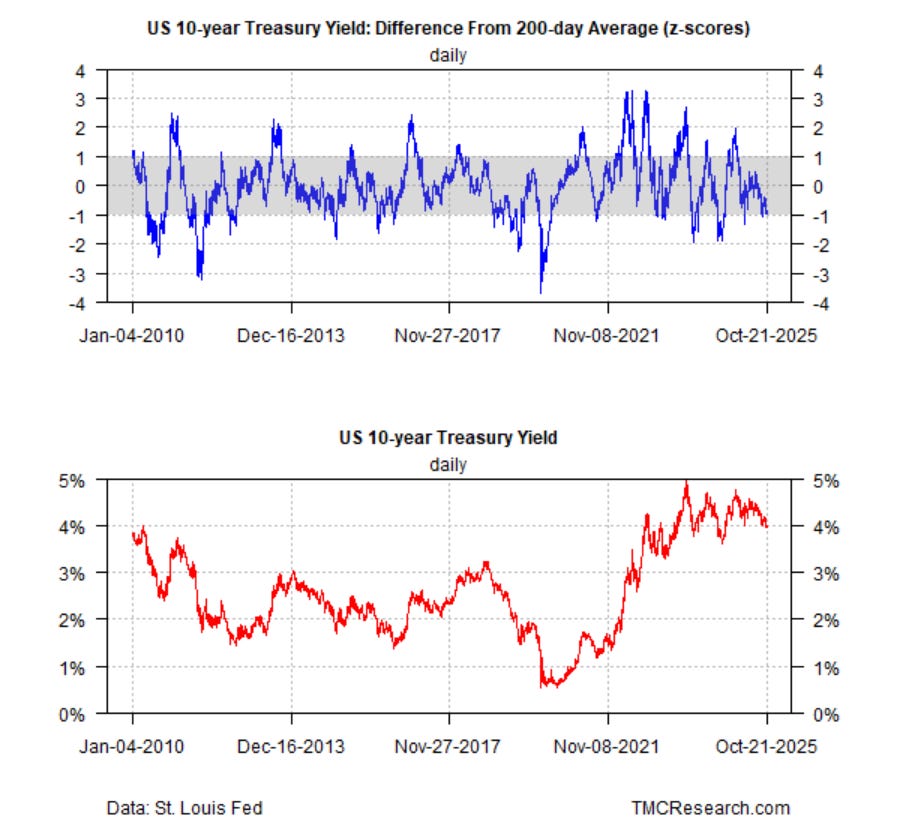

If there are concerns about upside inflation risk, it’s not showing up in the US 10-year Treasury yield, which continues to trade near its lowest level of the year.

Instead, the market and the Fed appear to remain more concerned about downside risks for the labor market. Last week Federal Reserve Chairman Powell said: “Inflation is above target and gently rising” while “the labor market is subject to pretty clear downside risks” in terms of hiring.

Labor market issues

Deciding if labor market risk remains a pressing concern, or not, has become challenging due to the government shutdown, which has delayed the September payrolls report.

Private-sector data can help fill in the gap, but alternative sources aren’t providing a clear picture of the labor market at the moment. The ADP Employment Report shows that private employers cut jobs for a second month in a row in September. Revelio Labs, a data analytics firm, paints a modestly brighter view and reports that hiring picked up last month, albeit from a low level.

Tomorrow’s CPI report could bring clarity, at least in terms of whether the Fed has a stronger or weaker case for more rate cuts. But if the consensus forecast is accurate, the inflation data will still leave room for debate.

This much is clear: the market will be forced to wait for the government to open for a clearer read on the numbers. Even if the shutdown ended today, tabulating and publishing new data will take time. The Fed, meanwhile, will be forced to make a new policy decision next Wednesday, well before the government starts updating economic figures.

An added complication for analyzing economic conditions: on top of the loss of data updates from various government agencies due to the shutdown, the payroll services firm ADP Research stopped providing its private-sector jobs data to the central bank following an Aug. 28 speech by Fed Governor Christopher Waller that referenced the numbers, according to The Wall Street Journal. The Fed’s already challenging job of assessing the economy seems to be getting tougher.

Thank you.

For anyone interested, here are my Sep CPI estimates:

https://arkominaresearch.substack.com/p/sep-2025-cpi-estimate?r=1r1n6n