Markets Expect Another Fed Rate Cut This Week

By James Picerno | The Milwaukee Company

Fed funds futures are pricing in a high probability of a rate cut on Wednesday (Dec. 10)

Slowing payrolls contrast with still‑low jobless claims, leaving the labor outlook foggy

Muted inflation: Core PCE eased to 2.8%, giving the Fed cover to ease policy again

Delayed economic data and a mixed bag of indicators continue to complicate the macro outlook for the Federal Reserve, but markets remain confident that the central bank will cut interest rates again at this week’s policy meeting on Wednesday, Dec. 10.

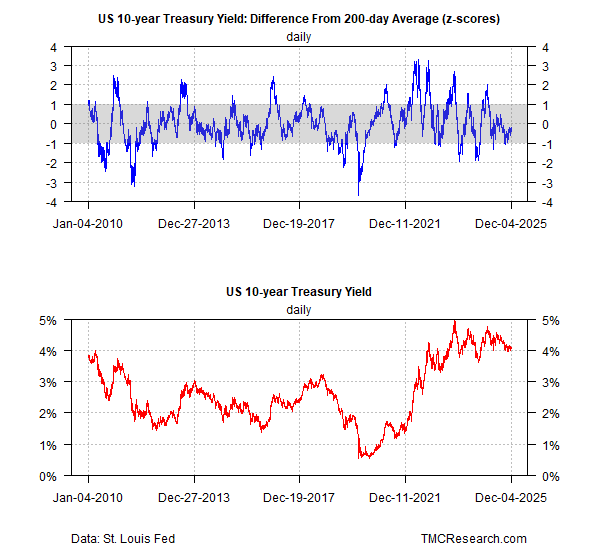

Fed funds futures are currently pricing in a high probability (90%) for a new round of easing. The bond market is on board with that view as US Treasury yields continue to trade near the lowest levels of the year, suggesting that the concerns about inflation remain muted. The 10-year rate, for instance, closed on Friday at 4.15%, close to the low point for 2025.

Recent economic numbers have been mixed, but signs that the labor market is slowing give the Fed room to cut rates again. ADP’s estimate of private-sector payrolls indicates a decline of 32,000 in November. Another estimate by Revelio Labs, a data firm, also report a loss for last month.

Some analysts question the reliability of these and other alternative sources for tracking the employment trend, but the slide highlights a consensus view: hiring has downshifted, a slowdown that’s also visible, if less starkly, in the Labor Department’s data through September.

Macro bulls counter that US weekly jobless claims – a leading indicator for payrolls — remain low, which suggests the labor market is still robust. The latest update for the week through Nov. 29 shows new filings for unemployment benefits diving to the lowest level in more than three years. The drop is probably distorted by the Thanksgiving holiday, but numbers in recent months also show that layoffs remain muted.

One pushback is that the rise of the gig economy — workers in short-term, temporary and freelance jobs — has diluted the value of jobless claims, which mostly reflect layoffs from formal work relationships. Goldman Sachs reports that 5% to 15% of the US population is involved in gig work.

Higher inflation data could, in theory, stay the Fed’s hand, but the latest release of PCE inflation results for September from the Bureau of Economic Analysis suggests that pricing pressure is holding at a middling pace relative to results for the year so far. Notably, core PCE inflation – one of the Fed’s closely-watched indicators – ticked lower in September for the first time since April in year-over-year terms, easing to 2.8%, which matches the average print so far in 2025.

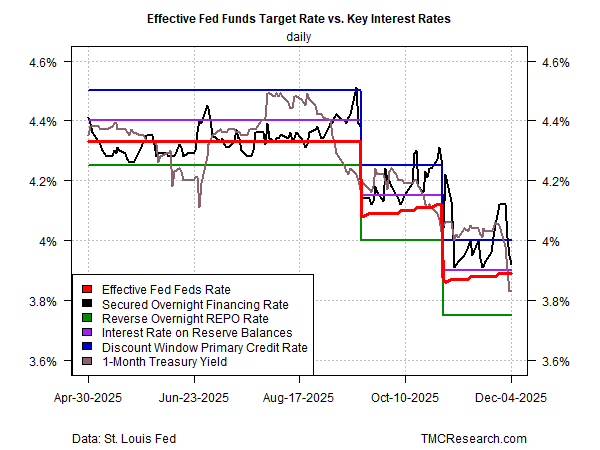

Adding to the dovish outlook: Recent warning signs for near-term interest rates has softened lately, based on several key yields that are closely watched for estimating the Fed’s policy decisions. As shown in the chart below, the bias has turned dovish again, following a brief but fleeting hawkish run in late-November.

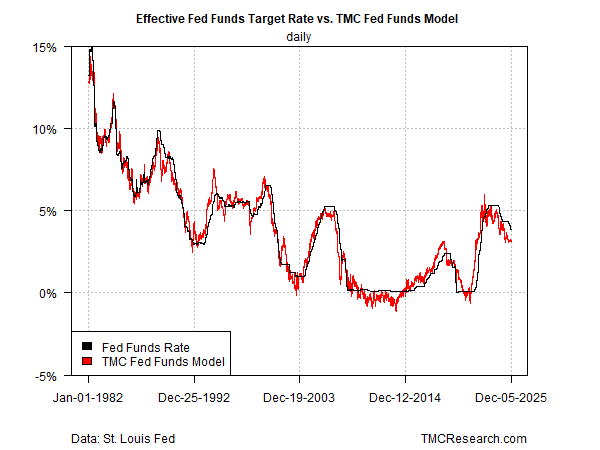

TMC Research’s Fed funds model continues to indicate a moderately hawkish bias for monetary policy. That may be useful in that it gives the central bank cover to cut and still argue that policy is somewhat tight—a non-trivial talking point at a time when some polls show that Americans are concerned about the cost of living.

No matter what the Fed does on Wednesday it will be controversial in some degree as analysts debate the best path forward for policy. With several key economic reports still delayed, the economic profile for the fourth quarter remains foggy. But to the extent that the central bank will err, it looks set to err on the side of caution by cutting rates and assuming that economic conditions are softening.