Macro Fog Thickens, But Market Sentiment Still Points to Another Rate Cut

By James Picerno | The Milwaukee Company

Powell signals caution: Fed policy “not on a preset course” as economic data grows murky

Markets lean dovish: Fed funds futures price in near-70% probability of a December rate cut

Mixed labor signals: ADP shows modest hiring rebound; Challenger reports 20-year high in layoffs

The next policy meeting for the Federal Reserve is more than a month away, but market sentiment remains moderately confident that another cut in interest rates is brewing for December. Official commentary from the central bank, however, suggests the Fed prefers to keep the crowd guessing.

At the Oct. 29 meeting, Fed Chairman Powell downplayed the idea that a new round of policy easing is fate. Another rate cut “is not a forgone conclusion,” he said. “Far from it. Policy is not on a preset course.”

Powell reasoned that setting monetary policy is becoming more complicated as the government shutdown delays key economic reports and creates a data void. “What do you do if you’re driving in the fog?” Powell asked. “You slow down.”

Adding to the uncertainty is a pending decision by the Supreme Court on whether President Trump’s tariffs are legal. If the court overturns his authority to impose import duties without Congressional approval, billions of dollars collected by the US government since the tariffs took effect in the spring could trigger a wave of refunds, which could become a chaotic bureaucratic affair.

The fog metaphor, in short, remains apt in the first week of November as updates on the economy from private sources paint a mixed profile. For example, the ADP Employment Report for October indicates hiring rebounded at US companies. “Private employers added jobs in October for the first time since July, but hiring was modest relative to what we reported earlier this year,” said Dr. Nela Richardson, chief economist at ADP.

A day after the relatively upbeat hiring data was released, the workplace consultancy Challenger, Gray & Christmas reported that its monthly read on layoffs surged in October to the highest level in 20 years. “October’s pace of job cutting was much higher than average for the month,” said the firm’s senior vice president. “Some industries are correcting after the hiring boom of the pandemic, but this comes as AI adoption, softening consumer and corporate spending, and rising costs drive belt-tightening and hiring freezes.” In total, firms have announced 1.1 million cuts this year, a 65% increase from a year ago and the highest level since the Covid pandemic year of 2020.

Using the policy-sensitive 2-year Treasury yield as a guide, market sentiment is still leaning in favor of softer monetary policy for the near term. This proxy for rate expectations continues to trend lower, trading below 3.6% on Thursday, close to the lowest level in 3-1/2 years.

Fed funds futures are pricing in a near 70% probability that the central bank will ease again next month and cut its target rate for a third time this year.

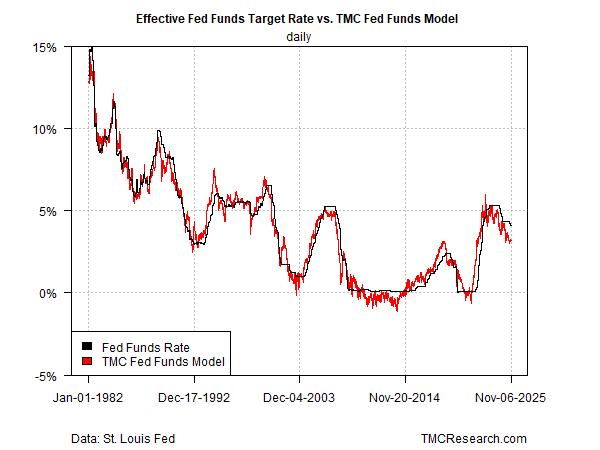

TMC Research’s Fed funds model indicates that the central bank still has room to cut rates while maintaining a modestly hawkish bias, thereby providing an opportunity to provide a relevant policy response at a time of muddled and missing economic data. The current Fed funds rate is roughly 90 basis points above our estimate of a neutral rate, i.e., a rate that would be optimal given current economic and financial conditions.

Notably, the degree of the current hawkish bias, per our estimate, remains in line with the bias that prevailed just before the Oct. 29 Fed meeting. The implication: the stance of monetary policy, relative to macro conditions, hasn’t changed much since last month’s rate cut.

Perhaps that’s the goal, to the extent the Fed is trying to maintain a balancing act of setting policy amid dense macro fog and more or less maintain the status quo while appearing to act on the margins. On that basis, another ¼-point cut in the target wouldn’t be surprising for Dec. 10. FOMC meeting since it would allow the Fed to publicly show that it’s addressing signs of a cooling economy without making a material change in its policy stance.