Is The Tide Turning Again In Favor Of Clean Energy Stocks?

By James Picerno | The Milwaukee Company

Alternative energy demand and usage continues to increase globally despite US policy shifts

Big oil shares are weakening relative to clean energy stocks

Renewables dominate new energy capacity

Companies in the alternative-energy business are facing a challenging future, at least from the vantage of Washington policy preferences.

The Trump administration is prioritizing development of fossil fuels and downplaying renewable energy. In the legislation President Trump signed into law on July 4, for example, tax breaks for wind and solar energy were cut, while federal subsidies and favorable tax treatment for the oil and gas industry were broadly expanded.

The investment prospects for alternative energy firms, in other words, appears to have undergone a significant transformation in the current political environment. But maybe investors didn’t get the memo. Following the sharp selloff in stocks in April, the rebound has favored renewable energy shares over conventional oil and gas firms by a wide margin. The outperformance raises the question: Is this potentially the start of new bull run for the clean energy industry?

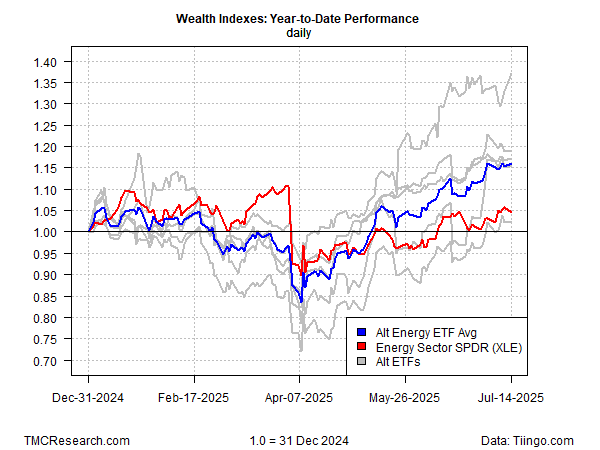

A few months is hardly compelling evidence, but it’s nonetheless striking that alt-energy stocks have rebounded sharply since the US stock market (S&P 500 Index) bottomed on April 8. Since then, the iShares Global Clean Energy ETF (ICLN) has rallied nearly 26%, or nearly twice the bounce for Big Oil stocks via Energy Select Sector SPDR ETF (XLE), as of July 14.

It’s tempting to write off the alt-energy rally as short-term noise. White House energy policy, after all, is not particularly favorable toward clear energy and is expected to remain so for the foreseeable future. That’s no trivial headwind. Market sentiment, however, has recently shifted in favor of solar companies, wind power and other companies engaged in non-fossil-fuel energy.

Consider how the five biggest alt-energy ETFs have performed year to date. Four of the five are currently ahead of the Big Oil proxy (XLE). The average of the five is up roughly 16% so far in 2025 vs. less than a 5% rise for XLE. Note that the alt-energy strength this year has arrived after the April sell-off.

What’s driving the sentiment shift? Perhaps it’s a revived recognition that renewable energy, despite Washington’s change in policy priorities, is still a growth industry. It may or may not receive government support, but as the technology for alt-energy continues to improve, and the related costs for generating energy in this industry continue to slide, demand growth is expected to persist.

A recent New Yorker story reported that renewables comprised 96% of demand for new energy globally in 2024 and 93% of new energy capacity in the US. It’s unclear how the Trump administration’s reversal of government incentives for renewables will affect business activity in the industry. But a recent report from BloombergNEF advises that the factors that have been ramping up demand for energy sources beyond fossil fuels remain intact. Meanwhile, global oil demand is expected to peak in 2032, preceded a few years earlier by peak demand for road-fuel consumption, the analysis predicts.

It's premature to assume that the market is again recognizing the long-term growth opportunities in alt-energy, but recent history raises the possibility. For perspective, the next chart shows the relative performance for a Big Oil proxy (XLE) vs. its global counterpart for clean energy (ICLN) vis-à-vis a pair of ETFs. When the line is rising, XLE is outperforming and vice versa.

The latest period of leadership for Big Oil relative to alt energy stocks started in 2021. One clue for thinking that XLE’s relative strength may be fading: the ratio’s 100-day moving average has fallen below its 200-day counterpart to the deepest degree in four years. That alone doesn’t ensure that ICLN will outperform. But clean energy shares have been out of favor several years and on that basis it appears that the selling may have gone too far.

Meantime, the economics of alt energy still look compelling for the years ahead, or so recent data implies. Morningstar, for example, reports this month that “Renewables (solar, wind, and battery storage) accounted for 99% of new generation capacity in first-quarter 2025… We expect renewables to continue to comprise the bulk of near-term capacity additions, along with natural gas additions and select nuclear restarts to help meet rising electricity demand.”

The transition from fossil fuels to clean energy will probably unfold over decades, perhaps gradually at times. But the shift is widely expected to endure, amid falling cost barriers in renewables that are slowly bringing them into parity with conventional energy sources, particularly on a global basis. It’s debatable if the recent pop in alt energy stocks reflects a renewed recognition of this long-term outlook, but for the moment it’s too early to dismiss the possibility.

Disclosure: The author owns shares of ICLN