Is The Stock Market Predicting A Recession?

By James Picerno | The Milwaukee Company | jpicerno@themilwaukeecompany.com

The recent correction in the stock market has yet to trigger a clear recession warning for the US economy, based on a model that uses S&P 500 drawdowns.

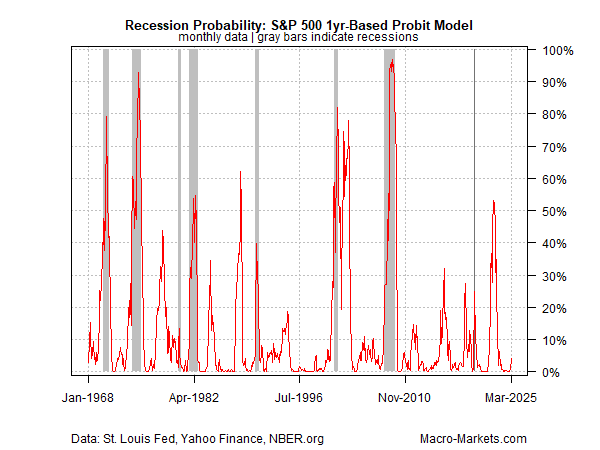

A probit-based model is currently estimating a roughly 5% probability that the US economy is contracting.

The evolution of tariff risk in the days and weeks ahead could change the calculus, perhaps quickly, and so the current recession risk estimate should be revised daily for near term.

Recession risk appears to be rising, according to Wall Street fund managers, analysts and strategists, based on a poll published this week by CNBC. Higher tariffs are cited as the catalyst. For some observers, the sharp drop in the stock market in recent weeks is a smoking gun for expecting that the economy will soon contract.

Equities can be a useful forward-looking indicator for macro conditions, but there are several caveats. One is putting too much faith in one subjective and far from flawless view (in this case via the stock market) for deciding what constitutes a clear recession warning. To minimize bias it’s helpful to model stock market volatility as it relates to historical recession periods with an implied nowcast/forecast of economic contraction. On that basis, using the S&P 500 Index’s drawdown history as a predictor suggests there’s still a low probability that a US recession has started or is imminent.

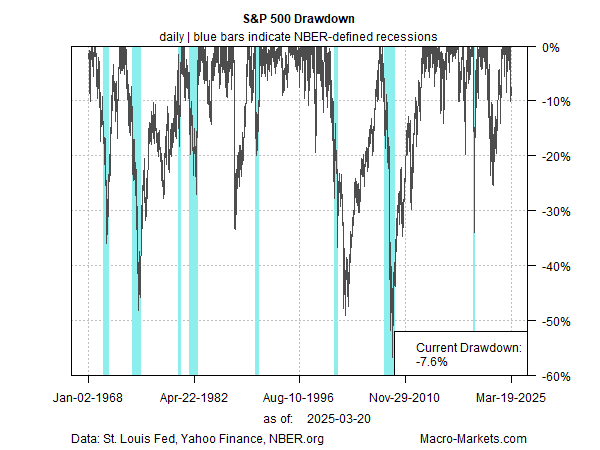

Let’s start with a review of the S&P’s drawdown, which is currently -7.6% as of Mar. 19, shown in the first chart above. That’s a relatively moderate peak-to-trough slide vs. history, and on its face it doesn’t appear that a recession is in progress or is close to starting.

But eyeballing drawdown vis-à-vis recessions can be tricky. To double-check the signaling for recession risk relative to rolling 1-year S&P 500 changes with a more quantitative approach, a probit model is used, based on business-cycle dates selected by the National Bureau of Economic Research. This model estimates a low probability (roughly 4%) that the US economy is currently in recession, shown in the second chart below.

As with any model, there are caveats to consider. The main issue here is the possibility that drawdown and rolling 1-year returns don’t fully capture the recession factor, in which case the estimates are, at best, rough approximations of the true risk.

A more fundamental challenge is that the stock market proper isn’t a reliable predictor of recession risk. That’s a caveat that resonates, given the market’s history of sometimes posting sharp losses without an ensuing recession. The most-extreme example: October 19, 1987, when the S&P 500 plunged more than 20% in a single day, a record decline, albeit one that did not soon lead to an economic recession (the next downturn started nearly three years later).

The stock market alone isn’t a reliable indicator of recession risk, but it’s still useful for monitoring the general consensus on expected macro risk. On that front, the recent upturn in estimated recession risk (albeit from a nil level) suggests that the mood has shifted. But until there’s a sustained increase in the probability guesstimate, the market’s pullback still appears to be a garden-variety drawdown.

That could change, of course, and perhaps quickly. Monitoring future changes with a drawdown-based probit model for estimating recession risk is a reasonable first-approximation of the stock market’s implied nowcast of business-cycle risk.

What might change the calculus? Tariff risk is at the top of the list of near-term risk factors. President Trump has marked April 2 for imposing reciprocal tariffs on countries. Depending on what happens, macro risk could rise sharply for the US economy. Or maybe much of the risk is negotiated away in the days ahead.

Meantime, the stock market’s decline to date can be viewed as a demand for a moderately higher risk premium. To date, the market’s decline doesn’t yet appear to reflect a high probability for recession. Given the rapidly-changing nature of the tariff situation, however, the current recession risk estimate should be revised daily until there’s deeper clarity on US policy plans for trade.

Read a pdf version of this article: