Is The Steepening Yield Curve A Sign To Favor Longer Treasury Maturities?

By James Picerno | The Milwaukee Company

Widening Treasury yield spreads could be an opportunity for investors, but uncertainty on the inflation outlook still suggests caution

The bond market is struggling with deciding if inflation or slower economic growth is the bigger risk

Wall Street this week will be looking for guidance from Fed Chair Powell, who’s scheduled on Friday to give what may be his most important speech of the year, if not his career

Under “normal” conditions, the widening spread in Treasury yields in recent months might be viewed as a sign that the market’s pricing in healthy economic growth. In turn, that might be considered an opportunity to hold longer-term bonds and take advantage of the fatter yield premiums vs. shorter-term securities.

But there’s an alternative narrative that’s resonating these days: Yields at the longer end of the curve are rising due to growing concerns that inflation will pick up.

Inflation, of course, is a non-trivial risk factor for bonds, particularly for longer maturities. With fixed payouts, the purchasing power of a given yield can wither if inflation rises. (Inflation-indexed Treasuries are an exception, but that’s a story for another day.)

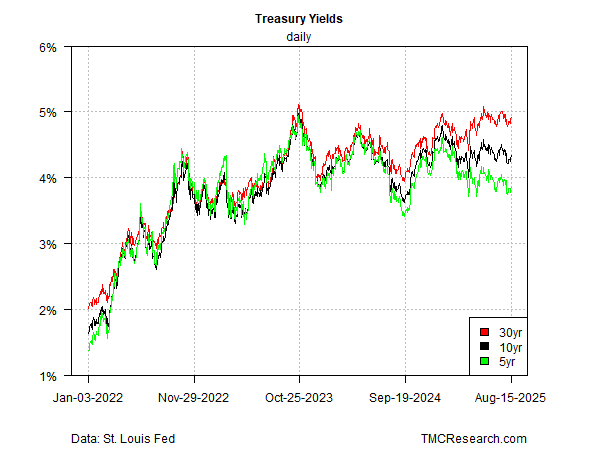

The 30-year yield has been slowly but persistently trending higher, closing at 4.94% on Monday (Aug. 18), near its highest level in two years. Meantime, shorter maturities continue to trade in a range. The benchmark 10-year rate is holding at a middling range vs. recent history: 4.34%, which is well below its previous peak of roughly 4.80% set in January.

The bond market, it seems, has yet to make up its mind about the near-term outlook. Although recent economic data has been mixed, including the latest inflation numbers, the crowd is struggling to decide if the dominant risk for the rest of the year is higher inflation, slower growth, or both – the dreaded stagflation scenario.

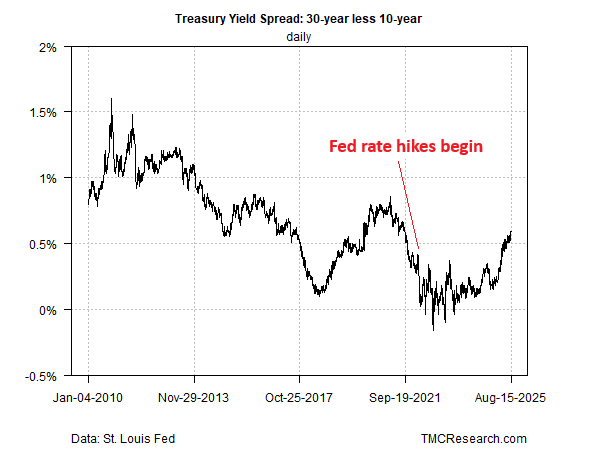

What is clear is that the Treasury curve is steepening (yields are widening between longer and shorter rates). This is at least partly due to a normalizing process following several years of a yield curve that’s been more or less flat to inverted.

When the Federal Reserve started to rapidly raise short-term interest rates in 2022, the market reacted by pricing in higher odds of slower growth if not recession. Although the economy proved to be more resilient than initially expected, the return to an upward-sloping profile has been gradual. In turn, the case for favoring shorter maturities has been persuasive. If you can get the lion’s share of yield in, say, a 5-year bond, why take the extra risk with a longer maturity?

As spreads have widened, the debate about whether it’s timely to go long is again topical. Consider the spread between the 30-year yield vs. the 10-year yield. Most of the time this spread should be positive, in favor of the longer-term bonds. Investors generally demand a higher yield for longer maturities as compensation for extra risk. This typical pricing relationship was thrown off course since the rate hikes began in 2022. But a return toward normalcy started in 2024, and progressed through early 2025.

The rise of tariffs, however, has introduced a new element of macroeconomic uncertainty and the bond market is struggling to assess if higher import duties will raise inflation, slow economic growth, or perhaps a bit of both. Then again, maybe the answer is neither – the US avoids recession and inflation remains relatively tame.

Deciding which scenario is likely dictates how you view the wider spreads of late. After several years of trading in close proximity to each other, the 5-, 10- and 30-year yields are returning to form. The 30-year’s 4.94% marks a relatively wide premium over the 10- and 5-year yields vs. recent history.

If you expect inflation will remain relatively contained, the case for buying longer-term Treasuries looks more appealing these days, courtesy of the higher yield over shorter maturities. All the more so if economic activity slows or falls into recession, a scenario that usually lifts Treasury prices and reduces yields as investors seek safe havens and assume that the Fed will cut rates to support the economy.

The complication is that markets appear to be sensing that higher inflation and softer growth are non-trivial risk scenarios.

At the moment, the growth downshift has the upper hand, based on Fed funds futures, which are pricing in high odds that the Federal Reserve will cuts rates at next month’s policy meeting (Sep. 17). Mixed numbers on inflation for July, however, leave room for debate.

The headline measure of the consumer price index (CPI) was steady in July at a 2.7% year-over-year pace. That’s still above the Fed’s 2% inflation target, but only moderately so. But core CPI (which strips out volatile food and energy prices and tends to be a better measure of the trend) rose again last month, touching 3.1% year over year, the highest since February.

Other warning signs for inflation include a sharp rise in wholesale prices in July: the 0.9% monthly increase in the produce price index (PPI) marks the biggest advance in over three years. By some accounts, PPI’s surge highlights the risk that higher tariff-related costs are now bubbling in the business sector. The debate is whether the hotter prices will soon show up in consumer prices, which would, in theory, pressure the Fed to maintain if not raise rates.

The sharp slowdown in hiring in July, by contrast, suggests that it’s timely to cut rates. Nonfarm payrolls last month posted another weak gain, which implies that the Fed’s priority is to pump more liquidity into the economy and lower rates. On that basis, the higher yields in longer maturities look relatively appealing.

These views will be tested this week in discussions at the Federal Reserve’s annual meeting in Jackson Hole, Wyoming. Wall Street will be keenly focused on Fed Chair Jerome Powell’s policy speech on Friday (Aug. 22). TMC Research is expecting that some version of the “watching and waiting” strategy will prevail when Powell regales markets with his current thinking.

Meantime, investors are pricing in a rate cut, an assumption that still feels premature unless the next employment report (due on Sep. 5) is at least as weak, if not weaker, than July’s increase.

Perhaps the wild card is the August inflation report (Sep. 11). A surprise, one way or the other, could drive the Fed decision the following week.

For now, it’s too early to confidently argue that the widening yield spread is a slam-dunk opportunity to go long on the curve. A modest 60 basis points separates the 30-year yield from its 10-year counterpart, and less than 50 basis points between the 10-year over the 5-year.

With the potential for higher inflation lurking, at least for now, those are still thin margins of comfort. Powell isn’t likely to convince us otherwise on Friday.