Is It Time To Consider Hedging Stock Market Risk?

By James Picerno | The Milwaukee Company

Emotion can derail investing goals

Risk management and diversification help prevent reactive mistakes

Planning beats reacting—prepare for market turmoil before it strikes

Betting against the stock market in the long run has generally been a losing proposition, but the short-to-medium term is often complicated.

Some investors with lengthy time horizons, and the steely discipline to sit tight during bear markets, have the patience to stay calm and focus on the long run. But such individuals tend to be the exception to the rule when it comes to investor behavior.

The worst-case scenario: an investor thinks he has a long-term focus, only to panic when markets hit rough seas, as they inevitably do from time to time. That mismatch can be a significant challenge to building long-term wealth because of what might be called the biggest behavioral risk for investing: Selling at or near a market bottom.

One solution is taking the long view, and perhaps employing Nathan Rothschild’s famous advice to buy when there’s blood in the streets. But while that’s sound advice in theory, in practice many investors discover in the depths of a financial storm that they can’t tolerate watching the value of their portfolio fall sharply.

There are many studies that document how emotion tends to conflict with long-term investing goals. For example, a 2019 study in the Financial Analysts Journal observed: “The field of modern financial economics assumes that people behave with extreme rationality, but they do not. Furthermore, people's deviations from rationality are often systematic.”

Another study, published last year in The Financial Review, focused on investor psychology and found that “during a bear market when stock prices decline, investors may experience depression due to the materialization of paper losses.”

Perhaps the most practical advice for the average investor is to update Rothchild’s advice: Prepare for when there’s blood in the streets.

Balancing Short-Term Pain Against Long-Term Gain

There are several implications that arise from the empirical fact that behavioral risk can derail an otherwise sound investment strategy. One is that the average investor can benefit from professional advice for investing decisions, if only to prevent sudden emotional reactions that can derail a long-term plan.

Sensible risk management is not only useful; it’s often essential for most folks as a tool for curbing the worst instincts that can arise during market downturns. For some individuals, there’s a strong case for monitoring market conditions and dialing down risk exposure when the prospect for market turmoil appears elevated.

Such efforts may or may not lead to higher long-term returns vs. buying and holding, but for investors who are vulnerable to panic selling that may not be the point. Rather, a disciplined process of opportunistically de-risking to a degree at certain points in the market and business cycles can minimize the worst impulses that arise during spikes in market volatility. Compared with panic-driven selling at or near market bottoms, such pre-planned risk management efforts can be beneficial, even if there could be a cost vs. letting it ride with buy and hold.

Risk Monitoring

For some investors, current market conditions appear to be suitable for taking a more defensive portfolio stance. Consider, for example, that the U.S. stock market has recently been trading at or near record highs. Market strength can be seen as a sign that even higher highs are coming, but for certain investor types (short time horizons, low risk tolerance, etc.) reducing exposure to risk assets may be timely.

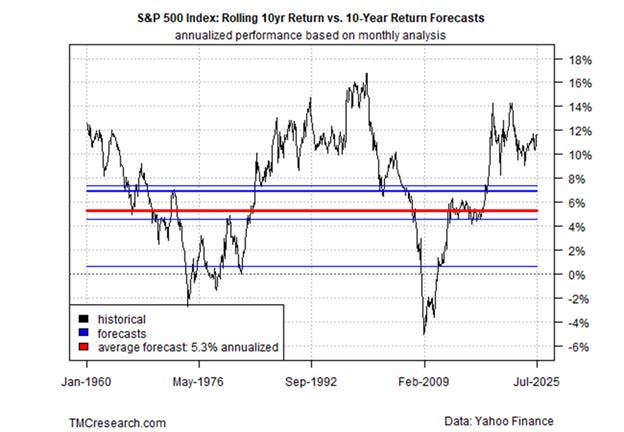

Consider, for instance, that TMC Research’s 10-year median forecast for US stocks (calculated via five models) is less than half the level compared with the trailing 10-year return. No one can see into the future, but there’s a reasonable case for expecting that the years ahead will deliver noticeably softer results vs. the bull run in recent years.

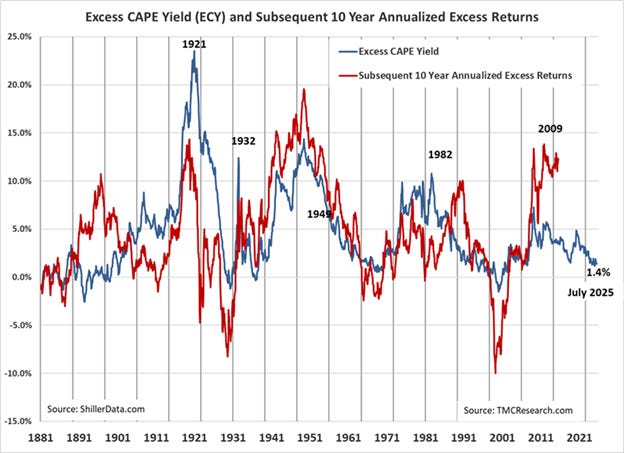

Several valuation measures of the US stock market also imply that the performance will be relatively modest in the years ahead vs. recent history. The S&P Shiller Cyclically Adjusted Price Earnings Ratio (CAPE) is close to its second-highest reading in history, which dates to 1871. Although short-term market timing based on market valuation is difficult if not impossible, this indicator suggests stocks are fully if not overvalued. In turn, that could be an early warning that a reversion to the mean (i.e., a market correction or worse) is a relatively high probability for some point in the near term.

A variation of CAPE (excess CAPE yield, or ECY, which crunches the data using inflation-adjusted numbers) also forecasts a weaker performance for stocks in the decade ahead: 1.4% annualized, based on ECY data as of mid-July.

The macro outlook also highlights reasons to be cautious with risk exposure. Start with the approaching August 1 deadline that could trigger higher tariffs on US imports. Meanwhile, heightened geopolitical risk continues in the Middle East as the war in Ukraine rolls on, each of which still pose threats to the global economy. There are also growing concerns about China’s plans to regain control of Taiwan, the home base to one of the world’s key semiconductor manufacturers at the leading edge of this crucial technology.

Risk Management

For investors who think it’s timely to take a more defensive position in their portfolio after a strong bull run, there are several choices. Each comes with its own unique set of pros and cons, and so different approaches will appeal to different investors. It’s also important to bear in mind the time horizon of the portfolio to customize decisions for each investor.

Holding more cash (or cash equivalents) is one possibility. It doesn’t hurt that a 3-month Treasury bill, for instance, is currently yielding 4.41% at the moment (July 22) — representing around 80% of the 10-year expected return for the stock market, based on our median estimate (see TMC Research chart above).

A drawback with raising cash is that it requires selling securities and perhaps incurring taxes in taxable accounts. One way to minimize outsized capital gains taxes is to use options, which provide a means for hedging without selling equities. Buying certain put options on the S&P 500 Index, for instance, opens the door to selling the index at a higher price (the strike price) after the market has fallen.

For investors with portfolios that are overweighted in stocks (a not uncommon scenario at the moment, thanks to the rally in equities), rebalancing the asset allocation back to the target weight (and thereby lowering equity holdings) is another possibility for managing risk.

Yet another way to hedge is to diversify existing equity holdings into lower-risk ETF equivalents. For instance, if you own an S&P 500 Index Fund, a portion of the allocation could be sold and redeployed to a low-volatility or value fund – strategies that have historically exhibited lower risk vs. a market-cap-weighted portfolio, such as the S&P 500 Index.

It’s also timely to revisit your asset allocation plan. For portfolios that aren’t diversified, or only partly so, it may be good time to consider a more expansive view of investing by adding bonds, foreign equities, foreign bonds, gold, commodities writ large, and real estate investment trusts. Each of those asset categories bring a degree of lower return correlation vis-à-vis US stocks, which could be beneficial if American equities run into trouble.