Investment Implications If The US Dollar’s Currency Reserve Status Continues To Wane

By James Picerno | The Milwaukee Company

The US dollar's global dominance appears to be waning, but without a clear successor.

A weaker dollar could boost non-dollar assets and impact US debt management.

Gradual diversification of currency reserves enhances the prospects for international investment strategies.

The US dollar is the world’s reserve currency with no obvious successors, but the recent market volatility has revived questions about the role of the greenback for the global economy going forward.

Dramatic changes in the short term are unlikely, but the foundation that’s anchored international finance over the past 80 years may be evolving. Rather than a sharp, sudden break with the past, the shift is more of a continuum. The dominance that the US dollar has commanded in the decades following World War II has been in gradually easing for years. The transition appears set to roll on in the wake of recent changes in Washington’s policy agenda for global trade.

To the extent that the US dollar’s supremacy as the world’s reserve currency continues to ebb, the evolution provides greater support for maintaining an internationally diversified portfolio.

A key factor for the near-term outlook is the Trump administration’s recent advocacy for a weaker dollar as a tool to revive the US manufacturing base. Vice President Vance, on the campaign trail last year as a sitting US senator, said: “‘Devaluing [the dollar]’, of course, is a scary word, but what it really means is American exports become cheaper, and that’s important. If you want to employ a lot of people in manufacturing, you need to make it easier for us to export and not just import what we need.”

More recently, Stephen Miran – one of President Trump’s leading economic advisors – outlined a plan (published by the White House) for reshaping the global economic order:

The U.S. provides the dollar and Treasury securities, reserve assets which make possible the global trading and financial system which has supported the greatest era of prosperity mankind has ever known.

Both of these are costly to us to provide… the reserve function of the dollar has caused persistent currency distortions and contributed, along with other countries’ unfair barriers to trade, to unsustainable trade deficits.

Citing his ideas for “restructuring the global trading system” a few months earlier, Miran wrote: “We may be on the cusp of generational change in the international trade and financial systems.”

The proposal is popularly known as the Mar-a-Lago Accord and could become the latest incarnation of previous currency agreements, such as the Plaza Accord in 1985 or the post-war financial restructuring of Bretton Woods in the 1940s. It’s unclear if the Trump administration will formerly pursue the Mar-a-Lago Accord, but in some respects movement toward implementation is already in progress.

The US Dollar Index has dropped 11% since its recent peak in January, although it’s debatable if this is part of the normal ebb and flow in currency markets or the start of extended decline. In any case, to the extent that the dollar’s role in global trade will ease, there’s still no obvious replacement.

The world’s three main currencies beyond the greenback – the euro, yen and yuan – each come with issues that raise roadblocks to anointing a clear winner in the way that the US dollar overtook the British pound in the early 20th century to become the world’s leading reserve currency.

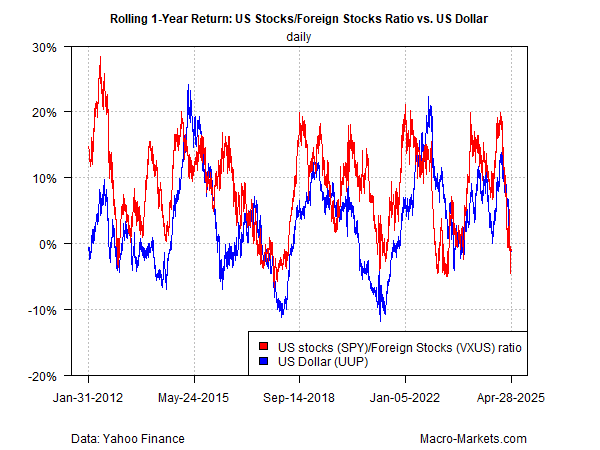

What is clear is that foreign exchange risk influences the relationships between foreign and US stock markets and that’s set to persist if not strengthen. The chart below compares the rolling 1-year return for the US dollar vs. the ratio of US shares to global stocks ex-US, based on a set of ETF proxies. The moderately positive correlation suggests that the dollar’s trend has been, and will remain, a key factor for relative performance for US vs. foreign equities.

If the dollar’s on track to play a lesser role in global finance, one implication is that owning non-dollar assets will become more attractive on the assumption that demand for foreign currencies will increase while holdings of dollars will decline, if only on the margins. Although a sharp and relatively quick realignment of dollar-based reserves at central banks and investment accounts around the world is unlikely in the short term, the ongoing diversification of currency holdings that’s been underway for years appears set to continue.

The euro is expected to be the leading beneficiary of ongoing efforts to diversify currency reserves. Although Europe’s currency is an imperfect replacement for the dollar for several reasons, it’s said to be the least-worst alternative compared with the yuan and yen.

Despite China’s economic heft – second only to the US in terms of GDP – the country’s currency is a poor substitute for the dollar. One reason: the country’s capital controls are a disincentive to holding the yuan beyond a role as a marginal reserve asset. The yuan represents roughly 0.2% of global central bank reserves, according to IMF data as of 2024’s third quarter. That compares with 57% for the dollar, 20% for the euro, and nearly 6% for the yen.

Gold is also a component of foreign exchange reserves, and one that’s reportedly in higher demand among central banks lately. A 2024 survey by the World Gold Council reported that nearly 70% of central banks are planning lift gold reserves over the next five years. The plan dovetails with ongoing efforts to reduce US dollar holdings.

China has been a large buyer of gold recently. Poland, Turkey and India have also been major buyers. Data from the World Gold Council shows that central bank purchases have ramped up starting in late-2022.

By one estimate, gold currently accounts for around 18% of total global reserves, although ignoring the main central banks in the West (including the US) cuts the total to 11%. Could the precious metal’s share of reserves go higher still? History suggests an emphatic “yes.” Consider that in the 1950s, gold topped 70% of reserves, which suggests there plenty of room for an upside reallocation. In turn, that implies the potential for gold to continue rising, even after setting a record high earlier this month at $3,500 an ounce.

Second-order effects of de-dollarization, even at the margins and through time, will apply to the US. Perhaps the leading factor relates to America’s large and growing pile of debt. The government runs a budget deficit that’s 7% of the economy and interest payments on the debt have ballooned to over $1 trillion a year.

The yawning amount of red ink, in theory, could reduce demand for US assets, Treasuries, in particular. But that effect has been muted in no small part due to the US dollar’s role as the world’s reserve currency, which provides an “exorbitant privilege,” as a French minister of finance famously observed of the greenback in the 1960s.

But the privilege is fading, if only slightly. With no clear alternative to a dollar-based system of global trade available at present, the status quo will likely continue for the near term. But efforts at diversifying currency reserves, along with looking for alternatives to facilitate international capital flows, will also persist. These trends, in concert with a change in US policy objectives, suggests that international diversification from an investing perspective looks attractive for the near term and perhaps longer.

While it may be the case that dedollarization is a trend with legs, in the short term the implication from the chart above is two fold. First, on a year over year basis the dollar has declined to a level where it typically bounces. Second, if that is accurate then the recent outperformance of international equities is likely over - at least in the short term.