Inflation’s Next Move Could Define Kevin Warsh’s Fed

A reality check awaits the incoming Fed chair with tomorrow’s consumer inflation report for April

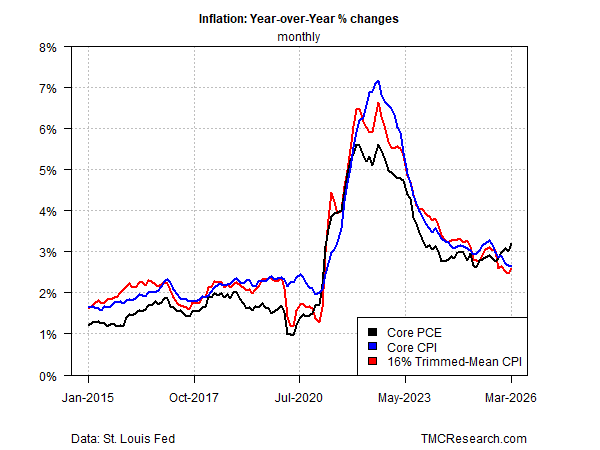

Headline inflation stays hot while core and trimmed measures are relatively stable

Inflation’s split signals complicate Warsh’s debut

By James Picerno | The Milwaukee Company

No one will be watching tomorrow’s update on US consumer inflation for April more closely than Kevin Warsh, who is expected to become chairman of the Federal Reserve this week following the Senate’s vote to confirm him.

The honeymoon may be short. Economists are forecasting that inflation will continue to accelerate at the headline level. The consensus estimate calls for a 3.8% year‑over‑year increase in the Consumer Price Index (CPI), according to Econoday.com — up from 3.3% in March. If correct, it will mark a second straight month of sharply rising pricing pressure, lifting the annual pace to a three‑year high.

Hotter inflation creates a challenge for Warsh, who has recently said that interest rates are too high — comments that have persuaded some observers that his hawkish reputation is softening. But the argument that rate cuts are prudent has become harder to make at a time when the energy shock from the war in the Middle East is driving up headline inflation.

In recent Senate testimony, Warsh recommended that the Fed refocus on the “trimmed averages” of inflation, which exclude outlier data and therefore offer a more robust profile of the trend. Notably, the Cleveland Fed’s Trimmed‑Mean CPI (T‑CPI) is running well below the Fed’s preferred inflation measure, the core Personal Consumption Expenditures index (core PCE), which excludes food and energy prices.

T‑CPI rose 2.6% for the year through March, matching the year‑over‑year gain in core CPI. By contrast, core PCE is running substantially hotter, at 3.2%, which is raising alarms in some circles that the Fed may soon need to hike rates.

The core PCE update will arrive at the end of May, but tomorrow’s CPI data may offer a preview. If economists are right, core CPI will edge up only slightly to a 2.7% increase versus the year‑ago level. The Cleveland Fed’s nowcast for April is a tick lower for the core reading.

Assuming those forecasts are accurate, the results may give Warsh some cover to argue that inflation is less threatening than it appears. Central bankers generally prefer core measures on the view that they offer a more reliable profile of inflation’s trend compared to headline inflation, which suffers from a higher degree of short-term noise.

The real challenge awaits in late May, when the core PCE numbers are released. The trend on this front is already running a full percentage point above the Fed’s 2% target.

It’s doubtful that Warsh will be able to persuade enough members of the Fed’s monetary policy committee to cut rates at the next meeting on June 17. Fed funds futures are pricing in a near‑certainty of no change.

Perhaps an even bigger issue to monitor is whether the new Fed chair’s views on rate cuts will evolve once he is confirmed for a four‑year term. A clue may emerge in tomorrow’s CPI report.