Inflation Expectations Edge Higher on Oil-Driven Tension

By James Picerno | The Milwaukee Company

Treasury-based inflation forecasts are inching up as the Iran conflict continues

Markets aren’t alarmed yet, but firmer expectations could complicate the Fed’s path

Persistent pressure from higher energy costs could reshape the Fed’s rate-cut timeline

The ongoing war in Iran has sparked inflation concerns following a surge in energy prices. Market sentiment has shifted, but only moderately to date, and so the implied outlook for inflation based on Treasury yields still leaves room for debate. The longer the conflict rages on, however, the greater the risk that a temporary increase in inflation could last longer and run higher than currently expected.

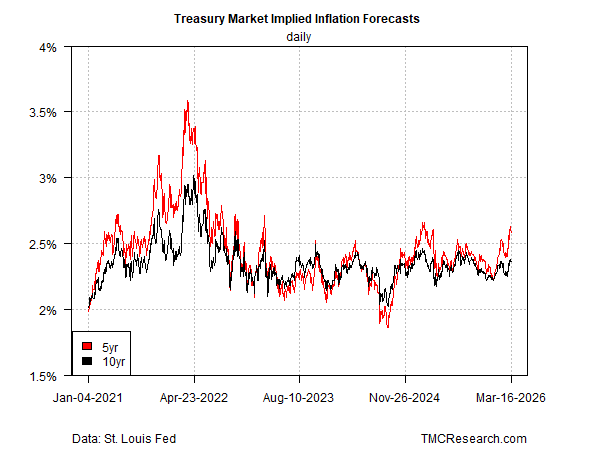

One way to monitor expectations is by tracking the bond market’s reactions, which provide a real-time measure of sentiment. Using the yield spread between nominal and inflation-indexed Treasuries—the so-called breakeven rate—shows that investors have lifted inflation expectations, but only moderately so far. The market’s implied 5-year inflation forecast has increased to 2.58% (as of Mar. 16), near the highest in a year. The jump in the 10-year outlook is less severe, rising to 2.36%, a six-month high.

The differing reactions suggest that while the market perceives inflation risk as modestly higher for the medium term, the rise will be temporary, as suggested by the lower forecast for the 10-year horizon.

More importantly, both estimates are still close to actual inflation measures, based on the Consumer Price Index. In February, CPI rose 2.4% over the year-earlier level, roughly in line with the 10-year Treasury market’s forecast and slightly below the 5-year outlook.

The question is whether market sentiment will lift inflation expectations further in the days and weeks ahead? If so, it could signal growing concern that the energy shock may persist and push prices higher than currently expected.

Historically, oil spikes have tended to lift headline inflation only temporarily, Long-term expectations remained anchored near 2.5%, even during periods of $100-plus crude oil. A key exception was during the 2021–2022 cycle, when the post-pandemic recovery and expansive fiscal policy amplified demand and allowed higher energy prices to intensify both demand-pull and cost-push inflation pressures. The current situation, by contrast, is war-driven, and some of the effects are expected to ebb, perhaps sharply, when the fighting stops.

Fed Policy Path Becomes Less Certain

Could it be different this time? If inflation expectations rise, and remain sticky at a higher level, the Federal Reserve may be forced to delay rate cuts, or perhaps even raise rates. Cuts are off the table for the next several policy meetings, based on expectations derived from Fed funds futures. Traders see a slight chance for a cut at the September Fed meeting, but the odds are close to a coin flip, and so confidence is low about where policy is headed. Part of that uncertainty reflects the risk that the conflict could keep energy prices elevated, complicating the inflation outlook.

The sooner the war ends, the more encouraging the odds that any jump in inflation triggered by surging energy prices will be transitory. But with the conflict now in its third week, and no immediate end in sight, the market may continue to anticipate higher inflation risk.

At present there is no consensus view among analysts on how or when the conflict may end, with timelines shifting as events evolve and energy markets price in a geopolitical risk premium tied to the possibility of persistent disruptions to oil flows through the Strait of Hormuz.

The challenge is that developing relatively high-confidence estimates of future inflation risk will take time—probably a few months at a minimum—in the current environment. Even if the war stopped tomorrow, a return to “normal” and resetting expectations will unfold slowly.

In the meantime, market sentiment will be valuable for guesstimating the future. Using the Treasury yield spreads shown above as a guide suggests that investors aren’t panicking, but they are starting to price in the possibility that inflation could rise to some degree for a period of time.

Until there’s more clarity on the war’s path, and its effects on energy and beyond, the market will struggle with pricing risk for the inflation outlook.